Exploring Undiscovered Gems on Exchange None in December 2024

Reviewed by Simply Wall St

As global markets continue to display mixed performances, with major U.S. indices like the S&P 500 and Nasdaq reaching record highs while the Russell 2000 experiences a decline, investors are keenly observing small-cap stocks amid fluctuating economic indicators and geopolitical developments. In this dynamic environment, identifying promising opportunities requires a focus on companies that demonstrate resilience and potential for growth despite broader market volatility.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Marítima de Inversiones | NA | 82.67% | 21.14% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Forest Packaging GroupLtd | 17.72% | 2.87% | -6.03% | ★★★★★★ |

| Shandong Boyuan Pharmaceutical & Chemical | NA | 28.20% | 32.92% | ★★★★★★ |

| Tibet Development | 51.47% | -1.07% | 56.62% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Watt's | 73.27% | 7.85% | -1.33% | ★★★★★☆ |

| MAPFRE Middlesea | NA | 14.56% | 1.77% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Practic | NA | 3.63% | 6.85% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

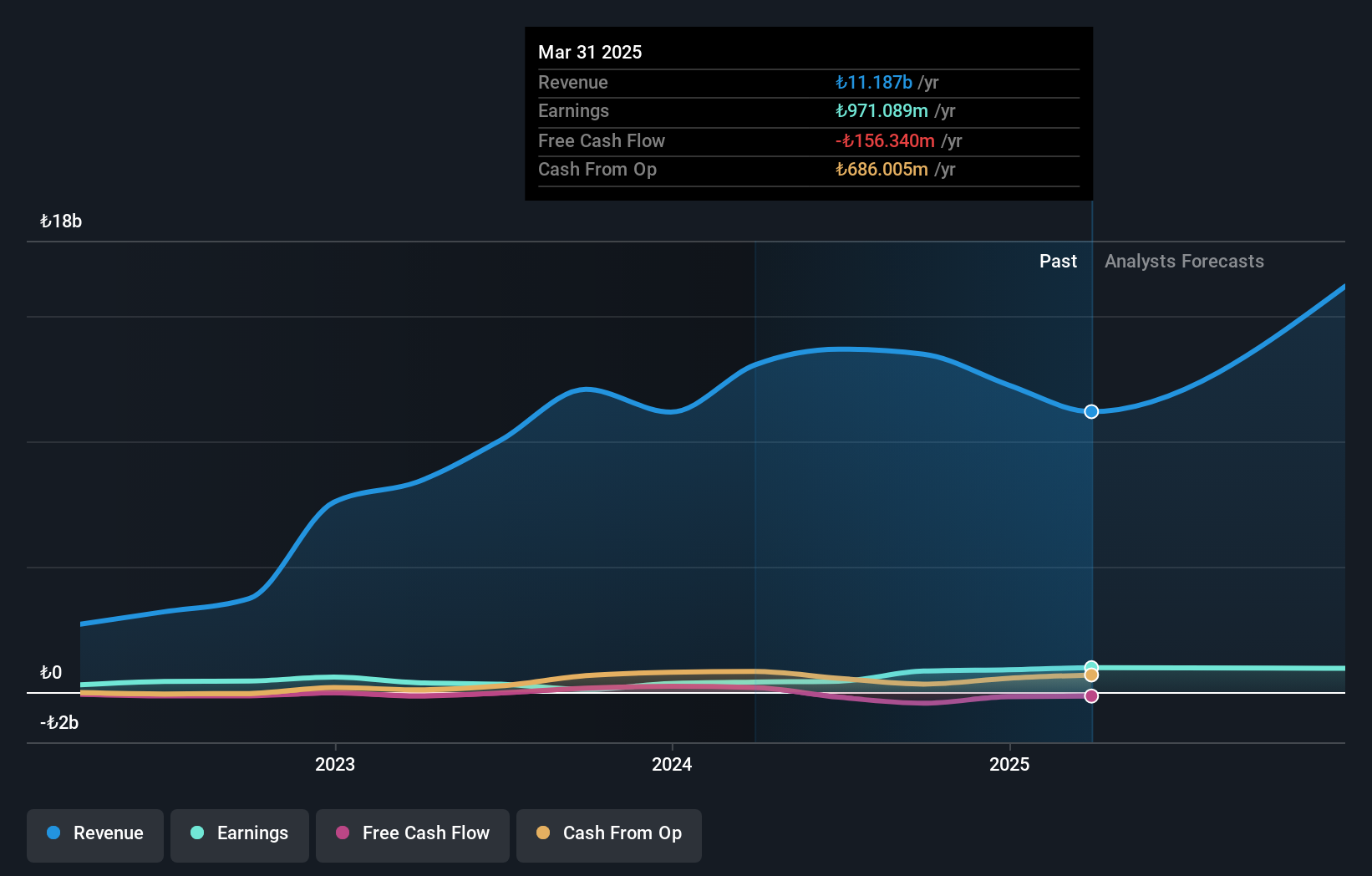

Sun Tekstil Sanayi ve Ticaret (IBSE:SUNTK)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Sun Tekstil Sanayi ve Ticaret A.S. is a company that designs, produces, and sells knit fabrics and ready-made womenswear garments in Turkey and internationally, with a market capitalization of TRY15.71 billion.

Operations: Sun Tekstil derives its revenue primarily from ready-made garments, contributing TRY7.26 billion, and fabric production, adding TRY2.09 billion. The company's gross profit margin is a key financial metric to consider when evaluating its performance over time.

Sun Tekstil, a notable player in the luxury industry, boasts a price-to-earnings ratio of 21x, which is below the industry average of 23.3x. Over the past year, earnings surged by 601%, significantly outpacing the industry's -21% trend. Despite this growth, free cash flow remains negative as of recent reports. The company has a satisfactory net debt to equity ratio at 0.1%, suggesting prudent financial management. Recent earnings highlight robust performance with third-quarter sales at TRY 2.94 billion and net income reaching TRY 310 million compared to a previous loss, reflecting improved profitability and operational efficiency.

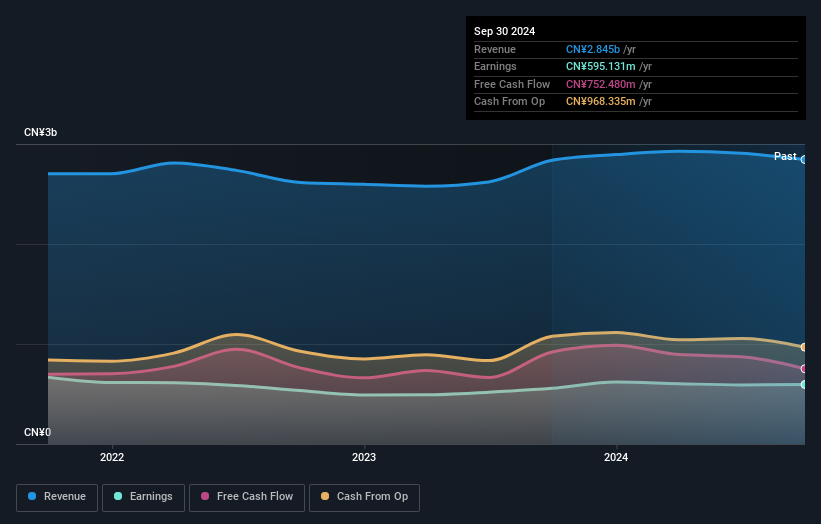

Chengdu Expressway (SEHK:1785)

Simply Wall St Value Rating: ★★★★★★

Overview: Chengdu Expressway Co., Ltd. is involved in the development, operation, and management of expressways in Chengdu, Sichuan province, China and has a market capitalization of HK$3.91 billion.

Operations: The company generates revenue primarily through toll fees collected from expressway operations in Chengdu. It incurs costs related to the maintenance and operation of these expressways. A notable financial aspect is its net profit margin, which shows variability across periods.

Chengdu Expressway, a smaller player in the infrastructure sector, has shown resilience with its earnings growing 7% over the past year, surpassing the industry average of 6.7%. The company seems to be trading at an attractive valuation, estimated to be 48.2% below fair value. Despite a slight dip in sales from CNY 2.21 billion to CNY 2.16 billion for the nine months ending September 2024, it maintains high-quality earnings and positive free cash flow. Its debt situation appears manageable with a net debt to equity ratio of just 6%, indicating financial stability amidst market challenges.

- Take a closer look at Chengdu Expressway's potential here in our health report.

Understand Chengdu Expressway's track record by examining our Past report.

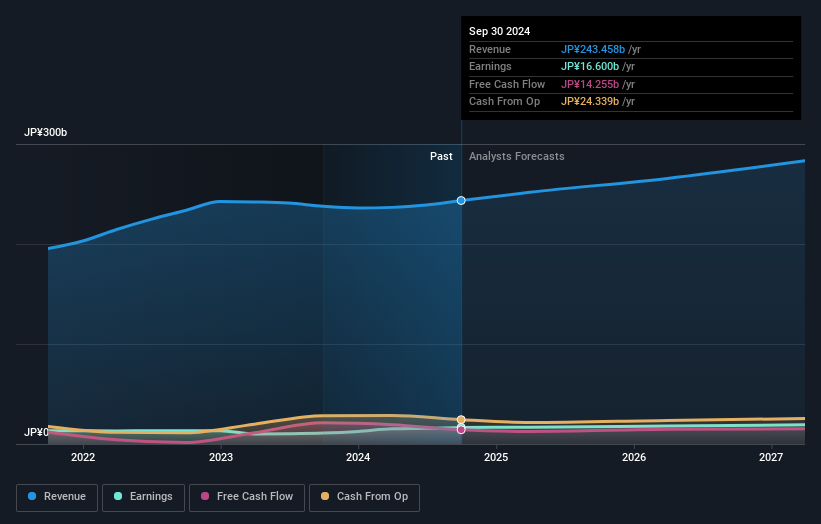

Aica Kogyo Company (TSE:4206)

Simply Wall St Value Rating: ★★★★★☆

Overview: Aica Kogyo Company, Limited is engaged in the development, production, and sale of chemical products, laminates, and building materials both in Japan and internationally with a market capitalization of approximately ¥207.83 billion.

Operations: Aica's primary revenue streams include chemical products and construction building materials, generating ¥138.04 billion and ¥109.29 billion respectively. The company does not allocate certain adjustments amounting to -¥3.87 billion across its segments.

Earnings for Aica Kogyo have surged by 50.7% over the past year, outpacing the Chemicals industry average of 14%, which speaks to its strong performance in a competitive sector. Trading at 35.1% below estimated fair value, it offers potential upside for investors seeking undervalued opportunities. The company has more cash than total debt, indicating a solid financial footing and reducing concerns about interest coverage. Recent buybacks saw ¥3,999.71 million spent to repurchase 1,207,400 shares or 1.89% of its capital—showing confidence in future prospects while also enhancing shareholder value with increased dividends from JPY 52 to JPY 56 per share this quarter.

- Unlock comprehensive insights into our analysis of Aica Kogyo Company stock in this health report.

Explore historical data to track Aica Kogyo Company's performance over time in our Past section.

Taking Advantage

- Embark on your investment journey to our 4626 Undiscovered Gems With Strong Fundamentals selection here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4206

Aica Kogyo Company

Develops, produces, and sells chemical products, and laminates and building materials in Japan and internationally.

Solid track record with excellent balance sheet and pays a dividend.

Market Insights

Community Narratives