Singapore Airlines Limited's (SGX:C6L) Dismal Stock Performance Reflects Weak Fundamentals

Singapore Airlines (SGX:C6L) has had a rough three months with its share price down 11%. To decide if this trend could continue, we decided to look at its weak fundamentals as they shape the long-term market trends. Specifically, we decided to study Singapore Airlines' ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Put another way, it reveals the company's success at turning shareholder investments into profits.

Check out our latest analysis for Singapore Airlines

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Singapore Airlines is:

11% = S$2.2b ÷ S$20b (Based on the trailing twelve months to March 2023).

The 'return' is the amount earned after tax over the last twelve months. Another way to think of that is that for every SGD1 worth of equity, the company was able to earn SGD0.11 in profit.

What Is The Relationship Between ROE And Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

A Side By Side comparison of Singapore Airlines' Earnings Growth And 11% ROE

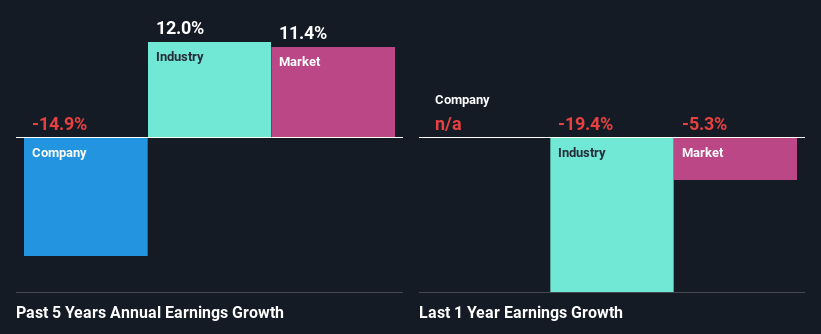

To begin with, Singapore Airlines seems to have a respectable ROE. Yet, the fact that the company's ROE is lower than the industry average of 14% does temper our expectations. Needless to say, the 15% net income shrink rate seen by Singapore Airlinesover the past five years is a huge dampener. Not to forget, the company does have a high ROE to begin with, just that it is lower than the industry average. So there might be other reasons for the earnings to shrink. These include low earnings retention or poor allocation of capital.

However, when we compared Singapore Airlines' growth with the industry we found that while the company's earnings have been shrinking, the industry has seen an earnings growth of 12% in the same period. This is quite worrisome.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is Singapore Airlines fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Singapore Airlines Making Efficient Use Of Its Profits?

With a LTM (or last twelve month) payout ratio as high as 107%,Singapore Airlines' shrinking earnings don't come as a surprise as the company is paying a dividend which is beyond its means. Its usually very hard to sustain dividend payments that are higher than reported profits. You can see the 2 risks we have identified for Singapore Airlines by visiting our risks dashboard for free on our platform here.

Moreover, Singapore Airlines has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 57% over the next three years. However, Singapore Airlines' future ROE is expected to decline to 6.9% despite the expected decline in its payout ratio. We infer that there could be other factors that could be steering the foreseen decline in the company's ROE.

Conclusion

On the whole, Singapore Airlines' performance is quite a big let-down. The company has shown a disappointing growth in its earnings as a result of it retaining little to almost none of its profits. So, the decent ROE it does have, is not much useful to investors given that the company is reinvesting very little into its business. Additionally, the latest industry analyst forecasts show that analysts expect the company's earnings to continue to shrink in the future. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:C6L

Singapore Airlines

Together with subsidiaries, provides passenger and cargo air transportation services under the Singapore Airlines and Scoot brands in East Asia, the Americas, Europe, Southwest Pacific, West Asia, and Africa.

Undervalued established dividend payer.