Advertisement

- Singapore

- /

- Specialty Stores

- /

- SGX:528

It's Unlikely That Second Chance Properties Ltd's (SGX:528) CEO Will See A Huge Pay Rise This Year

CEO Mohamed Salleh Marican has done a decent job of delivering relatively good performance at Second Chance Properties Ltd (SGX:528) recently. As shareholders go into the upcoming AGM on 21 December 2021, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still want to keep CEO compensation within reason.

Check out our latest analysis for Second Chance Properties

How Does Total Compensation For Mohamed Salleh Marican Compare With Other Companies In The Industry?

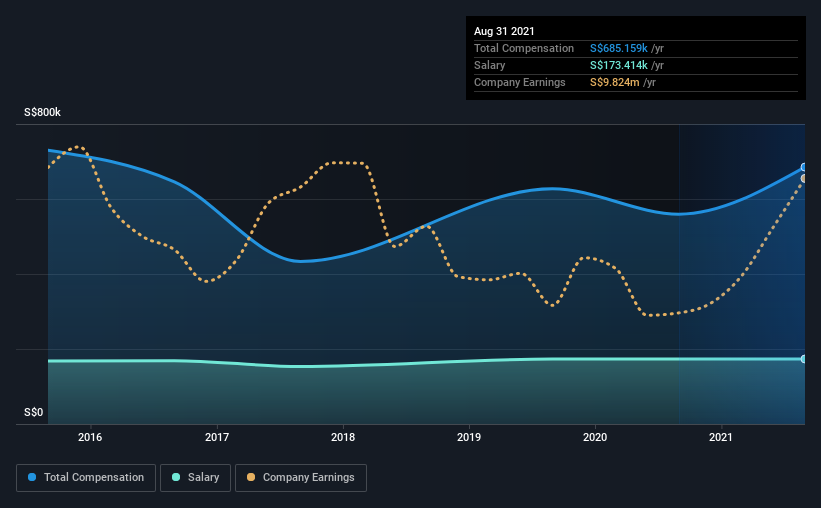

At the time of writing, our data shows that Second Chance Properties Ltd has a market capitalization of S$233m, and reported total annual CEO compensation of S$685k for the year to August 2021. Notably, that's an increase of 22% over the year before. While we always look at total compensation first, our analysis shows that the salary component is less, at S$173k.

For comparison, other companies in the same industry with market capitalizations ranging between S$137m and S$547m had a median total CEO compensation of S$380k. This suggests that Mohamed Salleh Marican is paid more than the median for the industry. Furthermore, Mohamed Salleh Marican directly owns S$162m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | S$173k | S$173k | 25% |

| Other | S$512k | S$386k | 75% |

| Total Compensation | S$685k | S$560k | 100% |

On an industry level, roughly 85% of total compensation represents salary and 15% is other remuneration. It's interesting to note that Second Chance Properties allocates a smaller portion of compensation to salary in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Second Chance Properties Ltd's Growth

Second Chance Properties Ltd has seen its earnings per share (EPS) increase by 7.6% a year over the past three years. It achieved revenue growth of 53% over the last year.

It's hard to interpret the strong revenue growth as anything other than a positive. And in that context, the modest EPS improvement certainly isn't shabby. So while we'd stop short of saying growth is absolutely outstanding, there are definitely some clear positives! We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Second Chance Properties Ltd Been A Good Investment?

Most shareholders would probably be pleased with Second Chance Properties Ltd for providing a total return of 52% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. However, if the board proposes to increase the compensation, some shareholders might have questions given that the CEO is already being paid higher than the industry.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We've identified 2 warning signs for Second Chance Properties that investors should be aware of in a dynamic business environment.

Important note: Second Chance Properties is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:528

Second Chance Properties

An investment holding company, operates in the retail of gold and jewelries, and ready-made garments in Singapore and Malaysia.

Mediocre balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets