Advertisement

- Singapore

- /

- Specialized REITs

- /

- SGX:DCRU

July 2024 Insights Into Three SGX Stocks Estimated as Undervalued

Simply Wall St

Reviewed by Simply Wall St

As the Singapore market continues to adapt to global financial innovations, such as the recent partnership between Visa and Tangem in the cryptocurrency sector, investors are keenly watching for opportunities that align with these evolving trends. In this context, identifying undervalued stocks becomes crucial, especially those that might benefit from or contribute to such technological advancements and economic shifts.

Top 5 Undervalued Stocks Based On Cash Flows In Singapore

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| LHN (SGX:41O) | SGD0.335 | SGD0.38 | 10.9% |

| Singapore Technologies Engineering (SGX:S63) | SGD4.26 | SGD8.20 | 48.1% |

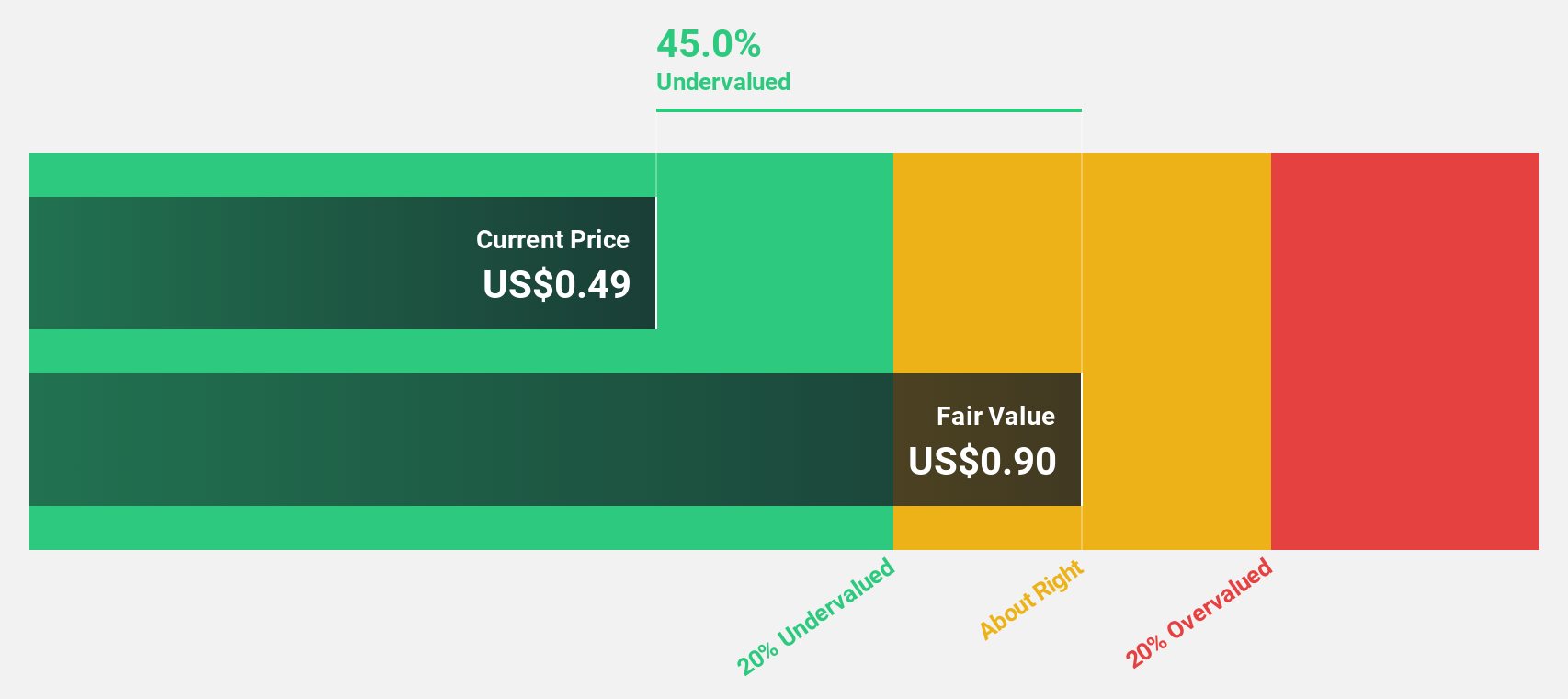

| Hongkong Land Holdings (SGX:H78) | US$3.20 | US$5.81 | 44.9% |

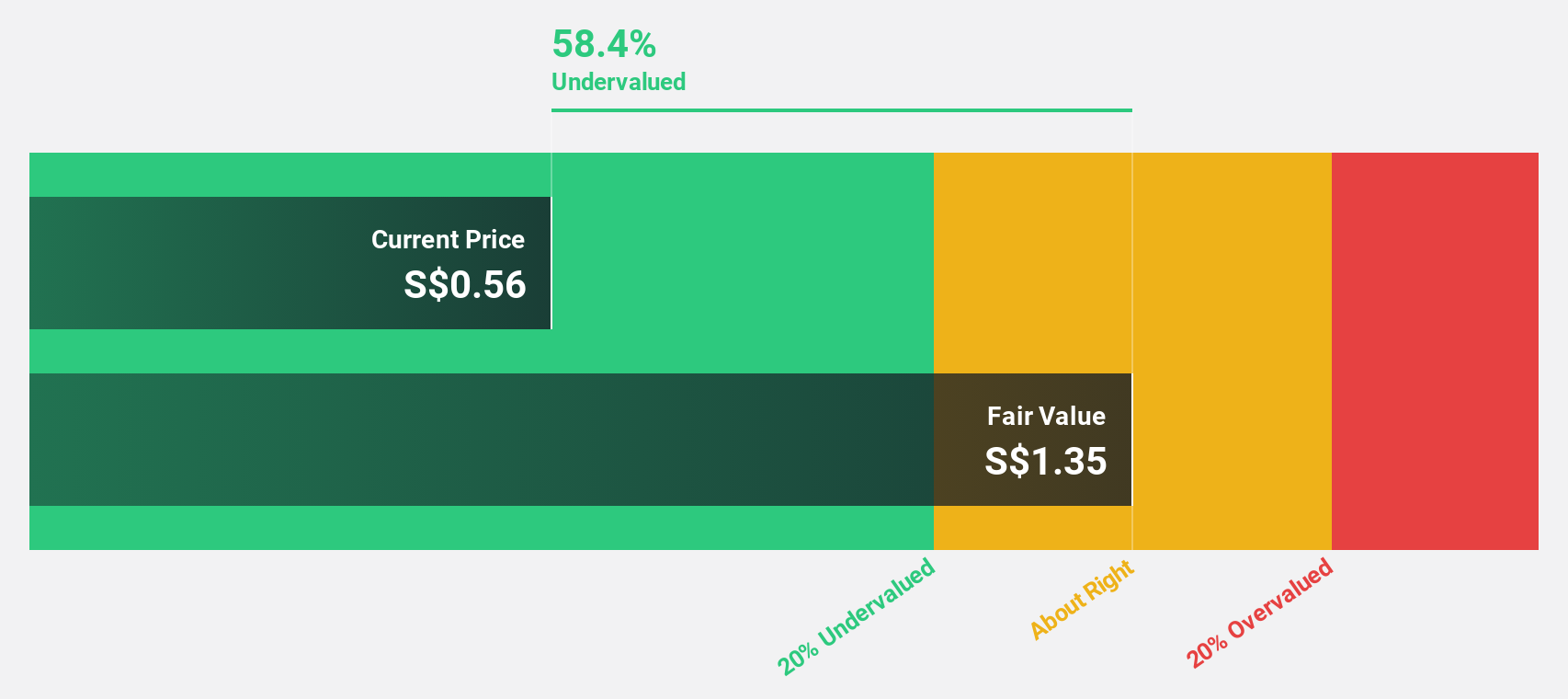

| Frasers Logistics & Commercial Trust (SGX:BUOU) | SGD0.93 | SGD1.65 | 43.8% |

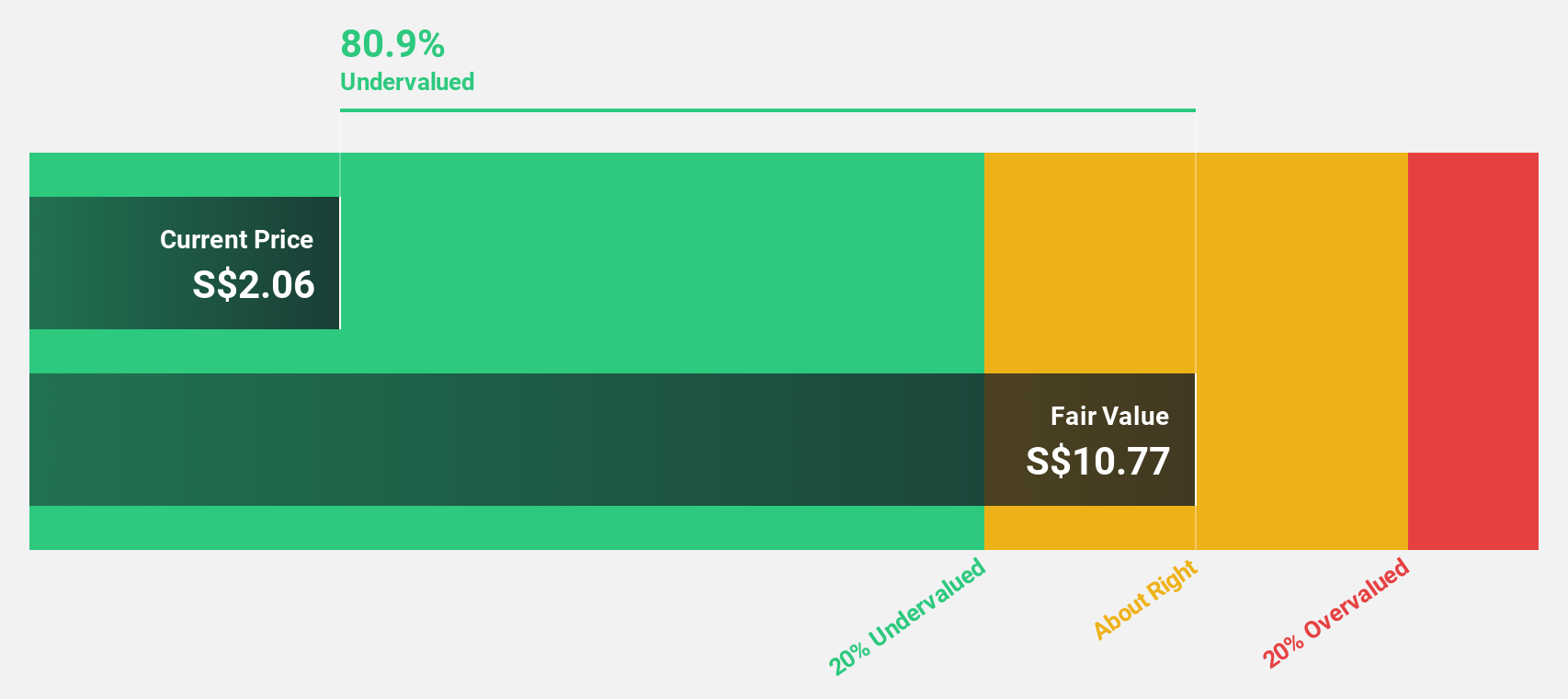

| Digital Core REIT (SGX:DCRU) | US$0.585 | US$1.10 | 47% |

| Seatrium (SGX:5E2) | SGD1.44 | SGD2.63 | 45.2% |

| Nanofilm Technologies International (SGX:MZH) | SGD0.84 | SGD1.47 | 42.8% |

Below we spotlight a couple of our favorites from our exclusive screener

Seatrium (SGX:5E2)

Overview: Seatrium Limited specializes in engineering solutions for the offshore, marine, and energy sectors, with a market capitalization of approximately SGD 4.91 billion.

Operations: The company generates revenue primarily through its segments in Rigs & Floaters, Repairs & Upgrades, Offshore Platforms, and Specialised Shipbuilding, totaling approximately SGD 7.26 billion.

Estimated Discount To Fair Value: 45.2%

Seatrium Limited, trading at SGD1.44, is significantly undervalued based on discounted cash flow analysis, with an estimated fair value of SGD2.63. Despite a highly volatile share price recently, it's positioned well below analyst targets with expectations of an 88.4% increase. The company's earnings are projected to grow by 72.23% annually and it is anticipated to become profitable within three years, outpacing average market growth predictions significantly. Recent large-scale contracts and strategic partnerships underscore its potential for revenue expansion and operational scale-up.

- The growth report we've compiled suggests that Seatrium's future prospects could be on the up.

- Click to explore a detailed breakdown of our findings in Seatrium's balance sheet health report.

Digital Core REIT (SGX:DCRU)

Overview: Digital Core REIT (SGX: DCRU) operates as a pure-play data centre real estate investment trust in Singapore, sponsored by Digital Realty, and has a market capitalization of approximately $762.92 million.

Operations: The company generates its revenue primarily from commercial real estate investments in data centres, totaling approximately $71.10 million.

Estimated Discount To Fair Value: 47%

Digital Core REIT, priced at $0.59, is considered undervalued by more than 20% according to discounted cash flow analysis, with a fair value estimated at $1.1. Despite its unstable dividend record and shareholder dilution over the past year, it's expected to become profitable within three years, with earnings growth projected at 104.28% annually. Recent corporate changes include the appointment of Ms Shim Gek Nii as Joint Company Secretary and a share buyback program initiation on April 19, 2024.

- Insights from our recent growth report point to a promising forecast for Digital Core REIT's business outlook.

- Unlock comprehensive insights into our analysis of Digital Core REIT stock in this financial health report.

Nanofilm Technologies International (SGX:MZH)

Overview: Nanofilm Technologies International Limited operates in Singapore, China, Japan, and Vietnam, offering nanotechnology solutions with a market capitalization of SGD 546.85 million.

Operations: The company generates revenue through four primary segments: Sydrogen (SGD 1.05 million), Nanofabrication (SGD 16.05 million), Advanced Materials (SGD 141.54 million), and Industrial Equipment (SGD 37.17 million).

Estimated Discount To Fair Value: 42.8%

Nanofilm Technologies International, with a current trading price of SGD0.84, is significantly undervalued based on discounted cash flow analysis, suggesting a fair value of SGD1.47. Despite modest profit margins at 1.8%, down from the previous year’s 18.5%, the company forecasts robust earnings growth at an annual rate of 50.66% and revenue growth at 15.1% annually, both outpacing broader Singapore market projections. Recent affirmations include a final dividend declaration and optimistic guidance for FY2024's financial performance.

- Our comprehensive growth report raises the possibility that Nanofilm Technologies International is poised for substantial financial growth.

- Navigate through the intricacies of Nanofilm Technologies International with our comprehensive financial health report here.

Make It Happen

- Click this link to deep-dive into the 7 companies within our Undervalued SGX Stocks Based On Cash Flows screener.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:DCRU

Digital Core REIT

A pure-play data centre Singapore Real Estate Investment Trust (S-REIT) sponsored by Digital Realty, a global best-in-class pure-play listed data centre owner and operator.

Very undervalued average dividend payer.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.6% undervalued

MA

Community Contributor