Advertisement

- Singapore

- /

- Real Estate

- /

- SGX:OU8

Centurion Corporation Limited Beat Analyst Estimates: See What The Consensus Is Forecasting For This Year

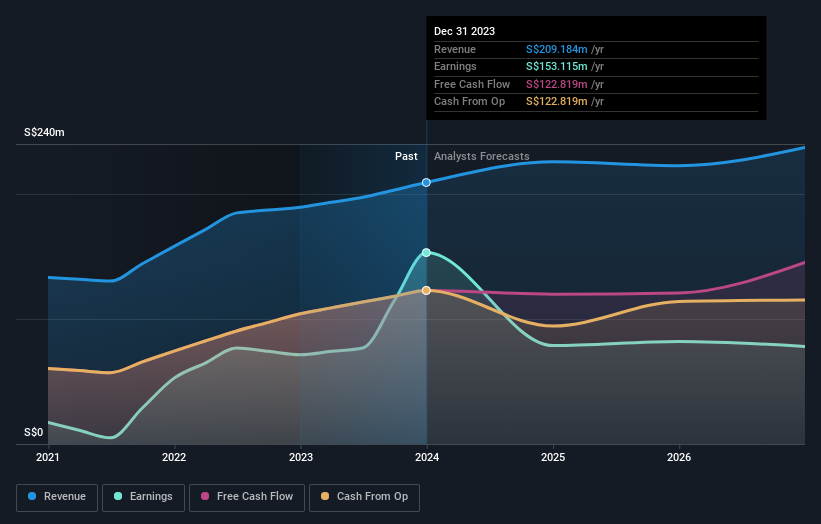

Centurion Corporation Limited (SGX:OU8) just released its latest yearly results and things are looking bullish. It was overall a positive result, with revenues beating expectations by 4.8% to hit S$209m. Centurion also reported a statutory profit of S$0.18, which was an impressive 119% above what the analysts had forecast. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for Centurion

Following the latest results, Centurion's four analysts are now forecasting revenues of S$225.8m in 2024. This would be a credible 7.9% improvement in revenue compared to the last 12 months. Statutory earnings per share are expected to plunge 52% to S$0.088 in the same period. In the lead-up to this report, the analysts had been modelling revenues of S$210.5m and earnings per share (EPS) of S$0.082 in 2024. It looks like there's been a modest increase in sentiment following the latest results, withthe analysts becoming a bit more optimistic in their predictions for both revenues and earnings.

Despite these upgrades,the analysts have not made any major changes to their price target of S$0.58, suggesting that the higher estimates are not likely to have a long term impact on what the stock is worth. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Centurion, with the most bullish analyst valuing it at S$0.63 and the most bearish at S$0.50 per share. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Centurion is an easy business to forecast or the the analysts are all using similar assumptions.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's pretty clear that there is an expectation that Centurion's revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 7.9% growth on an annualised basis. This is compared to a historical growth rate of 11% over the past five years. Compare this with other companies in the same industry, which are forecast to see a revenue decline of 0.09% annually. So it's clear that despite the slowdown in growth, Centurion is still expected to grow meaningfully faster than the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Centurion following these results. On the plus side, they also lifted their revenue estimates, and the company is expected to perform better than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Centurion going out to 2026, and you can see them free on our platform here..

You should always think about risks though. Case in point, we've spotted 4 warning signs for Centurion you should be aware of, and 2 of them are significant.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:OU8

Centurion

Owns, develops, and manages workers and student accommodation assets in Singapore, Malaysia, Australia, the United Kingdom, and internationally.

Very undervalued with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor