Advertisement

Exploring 3 Undervalued Small Caps In The Asian Market With Insider Action

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate the complexities of trade policies and fluctuating inflation rates, Asian small-cap stocks have become a focal point for investors seeking opportunities amidst broader market uncertainties. With smaller-cap indexes posting positive returns despite lagging behind larger peers, identifying promising small-cap stocks in Asia involves examining factors such as insider activity and potential undervaluation in light of current economic indicators and market sentiment.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.4x | 1.0x | 36.76% | ★★★★★★ |

| East West Banking | 3.1x | 0.7x | 33.64% | ★★★★★☆ |

| Lion Rock Group | 5.0x | 0.4x | 49.88% | ★★★★☆☆ |

| China XLX Fertiliser | 4.3x | 0.3x | 10.85% | ★★★★☆☆ |

| Atturra | 28.0x | 1.2x | 33.88% | ★★★★☆☆ |

| Sing Investments & Finance | 7.3x | 3.7x | 39.24% | ★★★★☆☆ |

| Dicker Data | 18.6x | 0.6x | -14.29% | ★★★☆☆☆ |

| Integral Diagnostics | 153.9x | 1.8x | 35.41% | ★★★☆☆☆ |

| AInnovation Technology Group | NA | 2.3x | 48.63% | ★★★☆☆☆ |

| Tabcorp Holdings | NA | 0.7x | -27.48% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

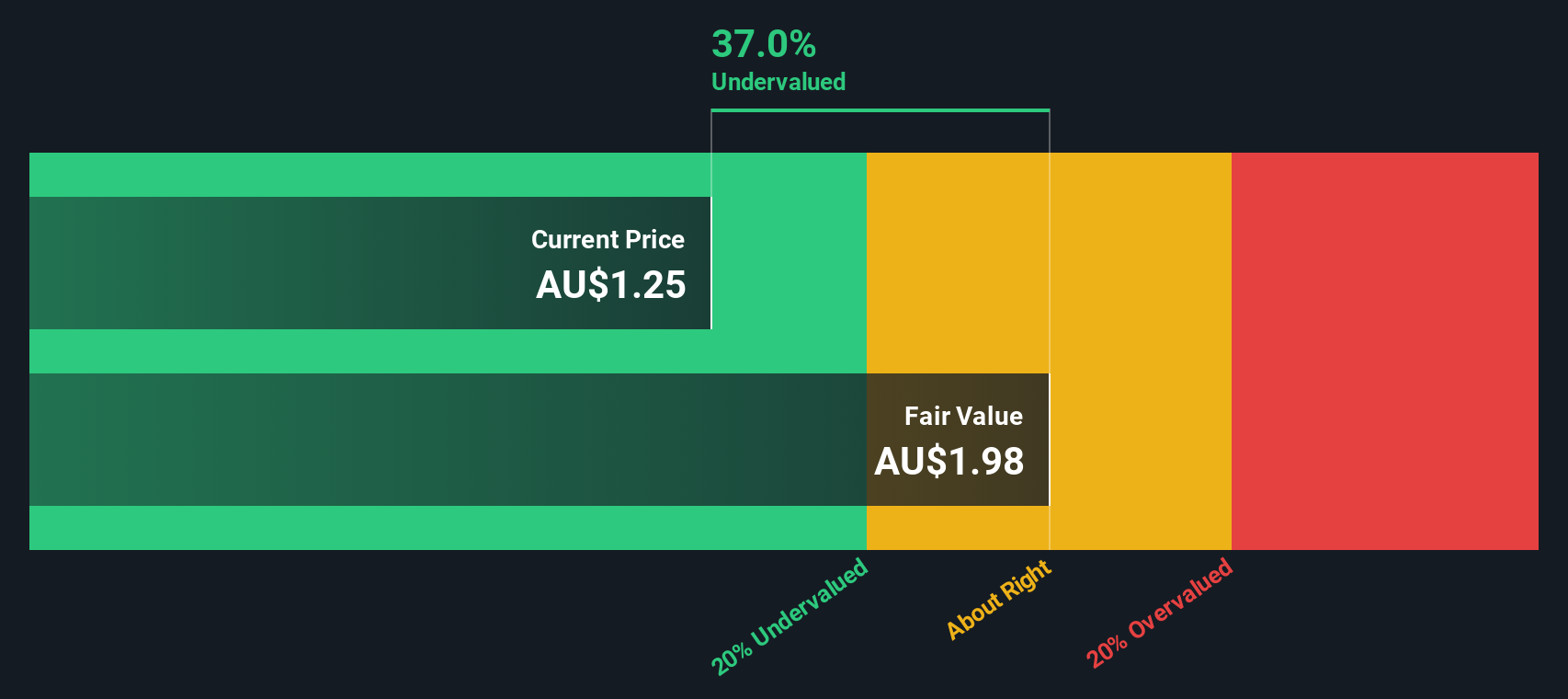

Infomedia (ASX:IFM)

Simply Wall St Value Rating: ★★★★★☆

Overview: Infomedia is a company that specializes in providing software solutions and services for the automotive industry, with a market capitalization of A$500 million.

Operations: Infomedia's revenue has grown from A$57.14 million to A$142.41 million over the observed period, primarily driven by its publishing segment. The company's gross profit margin consistently remains around 95%, indicating a strong ability to generate profit relative to its cost of goods sold. Operating expenses, including sales and marketing, R&D, and general & administrative costs, have increased alongside revenue but at a slower pace than gross profit growth. Net income margins show variability but generally trend upwards from approximately 21% to over 11%, reflecting changes in operational efficiency and expense management strategies over time.

PE: 29.2x

Infomedia, a tech-focused company in Asia, is gaining attention due to its current valuation. Recent insider confidence is evident as executives have been purchasing shares over the past six months. Despite recent leadership changes following Mr. Jon Brett's resignation in March 2025 due to health reasons, the company remains on track with earnings projected to grow by nearly 20% annually. However, reliance on external borrowing poses a risk factor for investors considering this stock's potential future growth trajectory.

- Click here to discover the nuances of Infomedia with our detailed analytical valuation report.

Evaluate Infomedia's historical performance by accessing our past performance report.

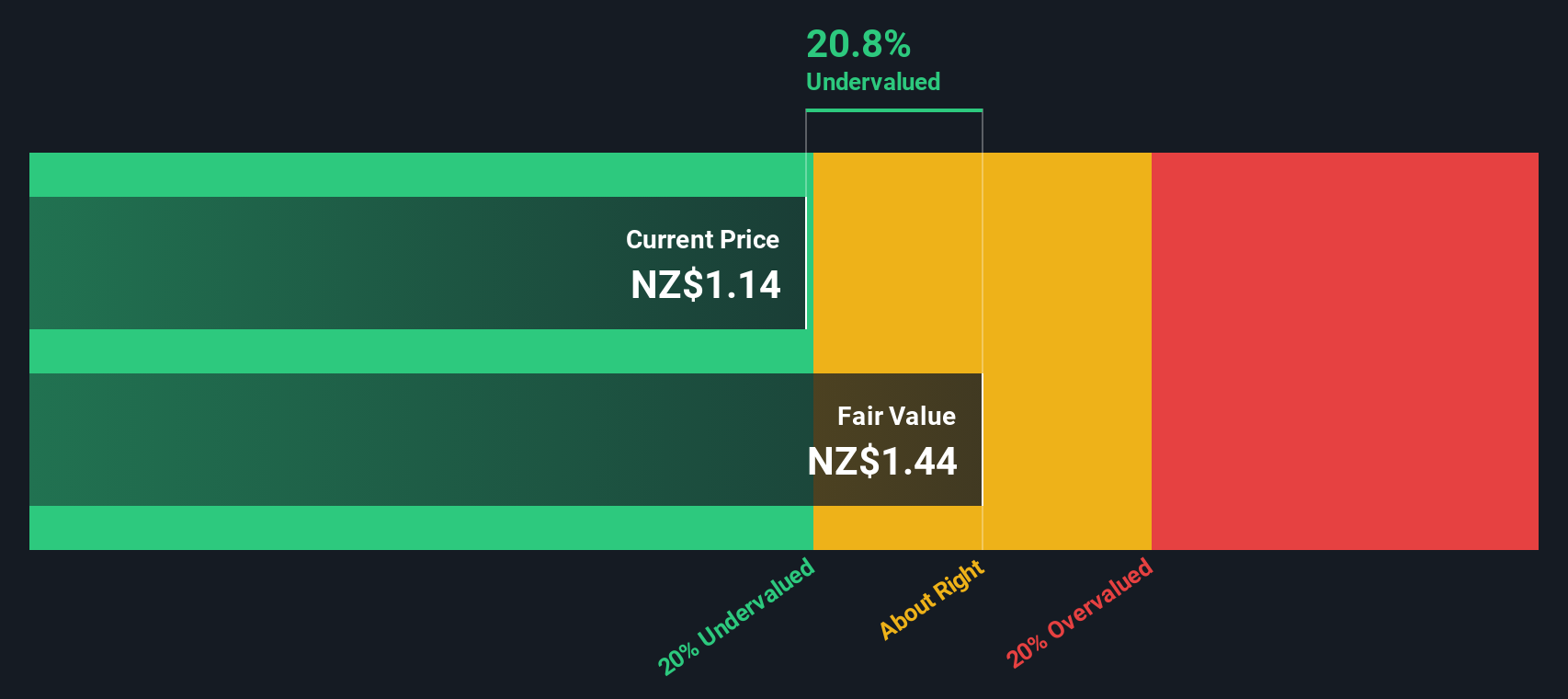

Stride Property Group (NZSE:SPG)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Stride Property Group operates as a property investment and management company in New Zealand, with a market capitalization of NZ$1.05 billion.

Operations: Stride Property Group generates revenue primarily from its SPL and SIML segments, with SPL contributing NZ$86.39 million and SIML adding NZ$31.28 million. The company has experienced fluctuations in its gross profit margin, which was 79.32% as of the latest period ending in June 2025. Operating expenses have remained a significant part of the cost structure, impacting overall profitability alongside non-operating expenses that have varied over time.

PE: 28.9x

Stride Property Group, a smaller player in the market, showcases potential for growth with earnings forecasted to increase by 15.06% annually. Despite relying on external borrowing, their recent financials reveal a turnaround: net income improved to NZ$21.65 million from a prior loss of NZ$56.12 million. Insider confidence is evident with recent share purchases, suggesting optimism about future prospects. However, large one-off items have impacted results and should be considered when evaluating its value proposition.

- Unlock comprehensive insights into our analysis of Stride Property Group stock in this valuation report.

Gain insights into Stride Property Group's past trends and performance with our Past report.

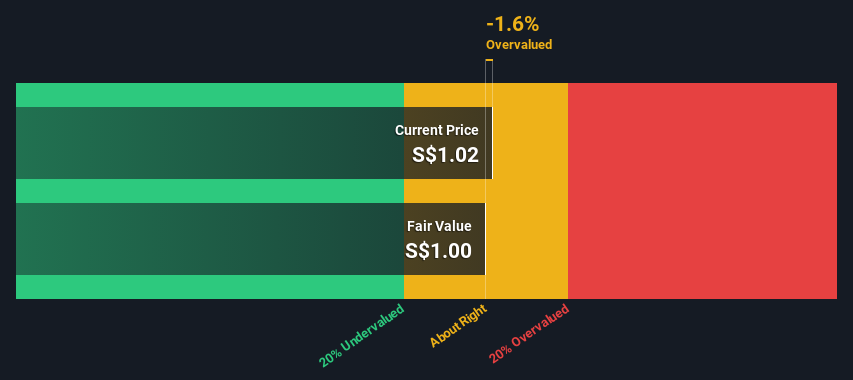

Far East Orchard (SGX:O10)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Far East Orchard is a diversified company engaged in property investment, hospitality operations, hospitality management services, and student accommodation, with a market capitalization of approximately SGD 0.51 billion.

Operations: The company generates revenue primarily from Hospitality Operations, Hospitality Management Services, Hospitality Property Ownership, and Property segments. The gross profit margin showed an upward trend, reaching 49.60% by the end of 2024. Operating expenses include significant allocations to General & Administrative and Sales & Marketing expenses.

PE: 8.3x

Far East Orchard, a smaller Asian company, is navigating through strategic shifts and financial challenges. Recently, they terminated a joint venture aimed at expanding in China's hospitality sector due to unmet objectives post-COVID-19 recovery. Despite this, the company remains on the lookout for other growth opportunities. Their acquisition of a Manchester site for student accommodation development reflects this ambition. The recent appointment of Deloitte & Touche as auditors signals potential changes in financial oversight.

Key Takeaways

- Navigate through the entire inventory of 63 Undervalued Asian Small Caps With Insider Buying here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:IFM

Infomedia

A technology company, develops and supplies electronic parts catalogues, service quoting software, and e-commerce solutions for the automotive industry worldwide.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor