- Singapore

- /

- Construction

- /

- SGX:E3B

3 Promising Penny Stocks With Market Caps Under US$400M

Reviewed by Simply Wall St

Global markets have recently experienced volatility, with U.S. stocks giving back some gains due to uncertainties around the incoming administration's policies and potential impacts on corporate earnings. For investors willing to explore beyond established giants, penny stocks—often smaller or newer companies—remain a relevant investment area despite being an older market term. These stocks can offer unique opportunities when backed by strong financials, providing both value and growth potential that larger firms might overlook.

Top 10 Penny Stocks

| Name | Share Price | Market Cap | Financial Health Rating |

| BP Plastics Holding Bhd (KLSE:BPPLAS) | MYR1.21 | MYR340.59M | ★★★★★★ |

| DXN Holdings Bhd (KLSE:DXN) | MYR0.48 | MYR2.39B | ★★★★★★ |

| Rexit Berhad (KLSE:REXIT) | MYR0.775 | MYR134.24M | ★★★★★★ |

| Seafco (SET:SEAFCO) | THB1.97 | THB1.6B | ★★★★★★ |

| LaserBond (ASX:LBL) | A$0.585 | A$68.57M | ★★★★★★ |

| Hil Industries Berhad (KLSE:HIL) | MYR0.87 | MYR288.79M | ★★★★★★ |

| ME Group International (LSE:MEGP) | £2.225 | £838.3M | ★★★★★★ |

| Lever Style (SEHK:1346) | HK$0.87 | HK$539.57M | ★★★★★★ |

| Embark Early Education (ASX:EVO) | A$0.80 | A$146.79M | ★★★★☆☆ |

| Next 15 Group (AIM:NFG) | £3.67 | £365M | ★★★★☆☆ |

Click here to see the full list of 5,818 stocks from our Penny Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

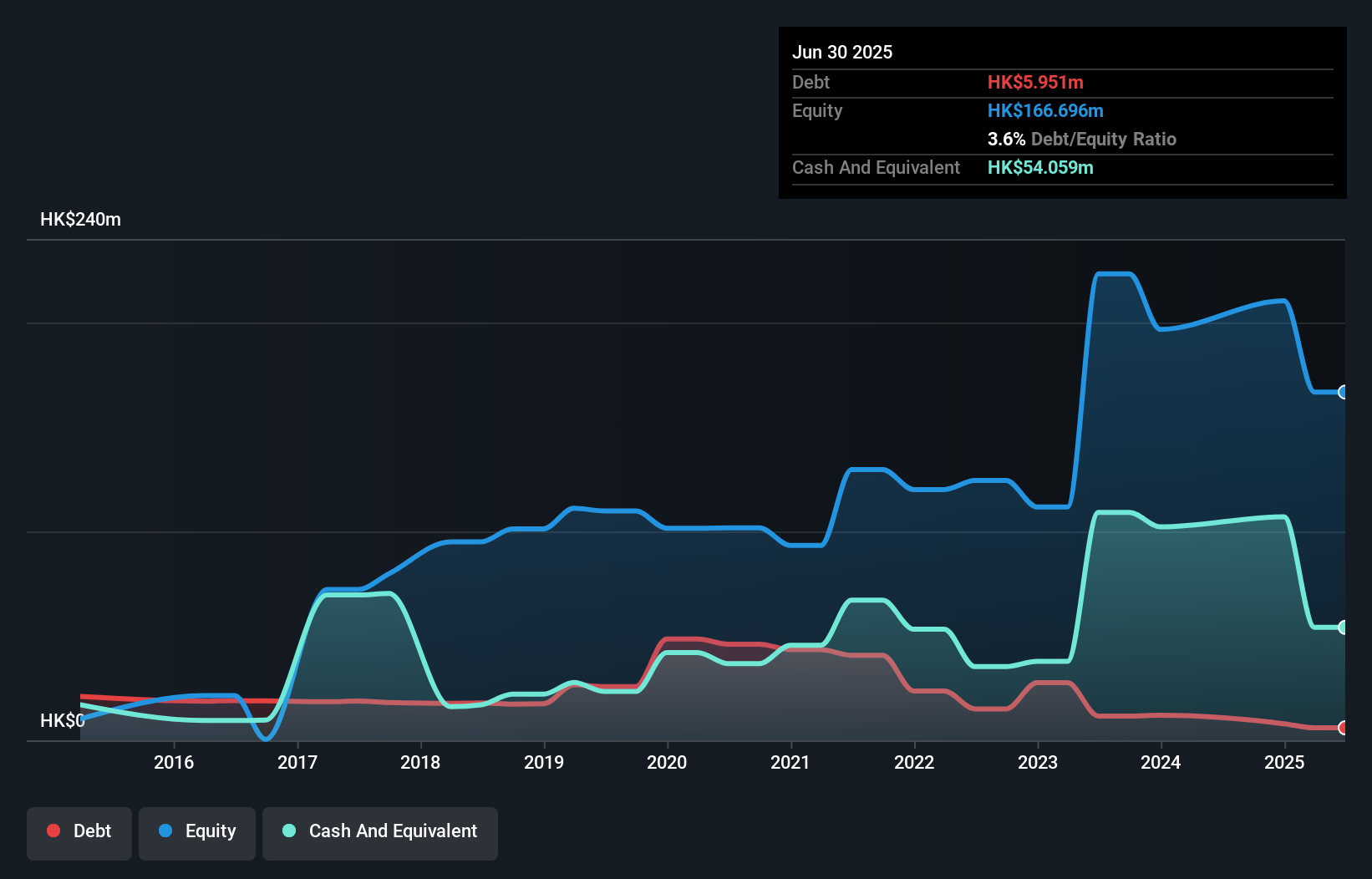

China Wantian Holdings (SEHK:1854)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: China Wantian Holdings Limited operates in the green food supply and catering chain, as well as environmental protection and technology sectors in Hong Kong and the People's Republic of China, with a market cap of HK$2.71 billion.

Operations: The company's revenue is primarily derived from food supply, contributing HK$360.98 million, followed by catering services at HK$20.02 million and environmental protection and technology services at HK$0.85 million.

Market Cap: HK$2.71B

China Wantian Holdings Limited, with a market cap of HK$2.71 billion, primarily generates revenue from its food supply sector. Despite being added to the S&P Global BMI Index recently, the company remains unprofitable with increasing losses over five years and a negative return on equity of -31.41%. While it has more cash than debt and its short-term assets exceed both short- and long-term liabilities, significant insider selling in recent months raises concerns. The management team is experienced, but insufficient data exists to assess the company's cash runway stability or growth potential accurately.

- Jump into the full analysis health report here for a deeper understanding of China Wantian Holdings.

- Assess China Wantian Holdings' previous results with our detailed historical performance reports.

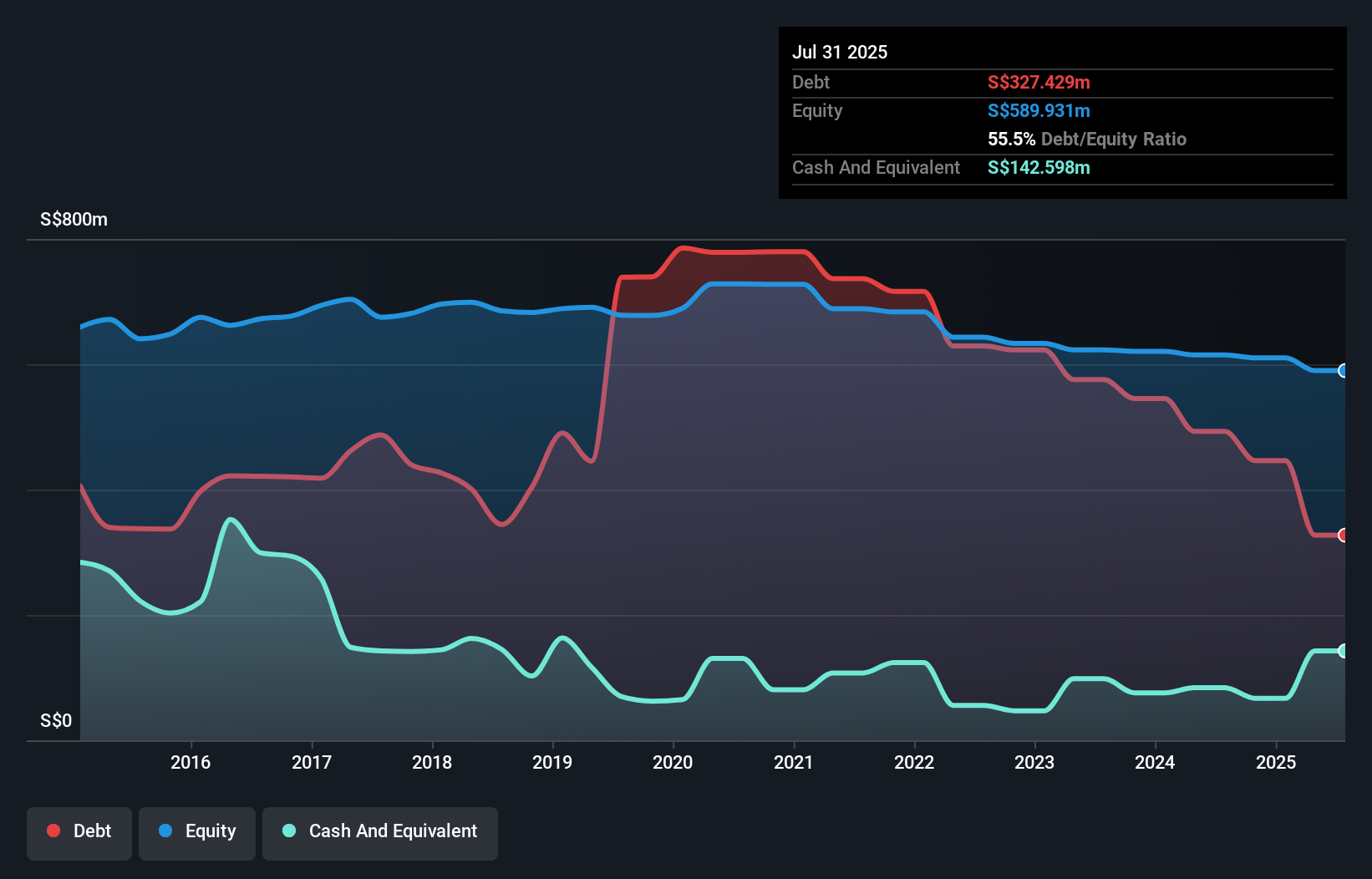

Wee Hur Holdings (SGX:E3B)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Wee Hur Holdings Ltd. is an investment holding company involved in general building and civil engineering construction in Singapore and Australia, with a market cap of SGD409.06 million.

Operations: The company's revenue segments include Building Construction (SGD121.19 million), Workers Dormitory (SGD76.45 million), Property Development in Singapore (SGD50.76 million), Fund Management (SGD5.81 million), PBSA Operations (SGD1.84 million), Corporate Segment (SGD2.20 million), and Property Development in Australia (SGD0.81 million).

Market Cap: SGD409.06M

Wee Hur Holdings Ltd., with a market cap of SGD409.06 million, has experienced significant investor interest due to speculation about the potential sale of its Australian purpose-built student accommodation (PBSA) business. Despite no confirmed transactions, the company's stock surged following reports of discussions involving major industry players. Financially, Wee Hur displays robust fundamentals: its debt is well-covered by cash flow and operating income, and it holds more cash than total debt. The company recently achieved profitability with high-quality earnings and a strong return on equity of 32.2%, although share price volatility remains high.

- Get an in-depth perspective on Wee Hur Holdings' performance by reading our balance sheet health report here.

- Explore historical data to track Wee Hur Holdings' performance over time in our past results report.

Low Keng Huat (Singapore) (SGX:F1E)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Low Keng Huat (Singapore) Limited is an investment holding company involved in property development and investment activities across Singapore, Australia, and Malaysia, with a market cap of SGD236.42 million.

Operations: The company's revenue is primarily derived from property development at SGD366.11 million, followed by investment activities including construction at SGD68.80 million, and hotel operations contributing SGD49.29 million.

Market Cap: SGD236.42M

Low Keng Huat (Singapore) Limited, with a market cap of SGD236.42 million, recently reported a return to profitability for the half year ended July 31, 2024, with net income of SGD5.79 million compared to a loss previously. Despite this positive shift, the company faces challenges such as high net debt to equity at 66.5% and interest payments not being well covered by EBIT. While its short-term assets exceed both short and long-term liabilities indicating liquidity strength, earnings have declined significantly over five years and share price volatility remains elevated compared to other Singaporean stocks.

- Click here to discover the nuances of Low Keng Huat (Singapore) with our detailed analytical financial health report.

- Understand Low Keng Huat (Singapore)'s track record by examining our performance history report.

Key Takeaways

- Unlock more gems! Our Penny Stocks screener has unearthed 5,815 more companies for you to explore.Click here to unveil our expertly curated list of 5,818 Penny Stocks.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wee Hur Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:E3B

Wee Hur Holdings

An investment holding company, engages in general building and civil engineering construction business in Singapore and Australia.

Flawless balance sheet and good value.