Advertisement

The board of NSL Ltd (SGX:N02) has announced that it will pay a dividend of SGD0.05 per share on the 24th of May. This means the annual payment is 5.7% of the current stock price, which is above the average for the industry.

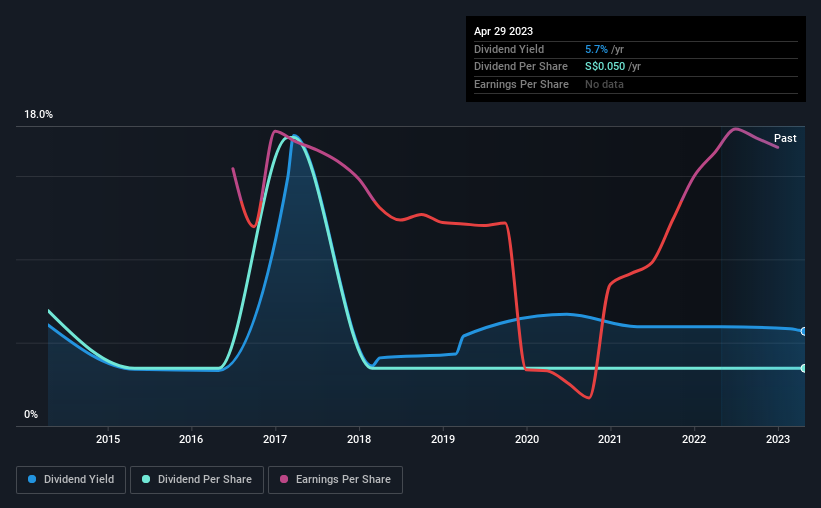

See our latest analysis for NSL

NSL Is Paying Out More Than It Is Earning

If the payments aren't sustainable, a high yield for a few years won't matter that much. Before making this announcement, the company's dividend was higher than its profits, and made up 82% of cash flows. This indicates that the company could be more focused on returning cash to shareholders than reinvesting to grow the business.

Earnings per share could rise by 19.6% over the next year if things go the same way as they have for the last few years. If the dividend continues on its recent course, the payout ratio in 12 months could be 146%, which is a bit high and could start applying pressure to the balance sheet.

NSL's Dividend Has Lacked Consistency

Looking back, NSL's dividend hasn't been particularly consistent. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. Since 2014, the dividend has gone from SGD0.10 total annually to SGD0.05. Doing the maths, this is a decline of about 7.4% per year. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

Dividend Growth Could Be Constrained

Dividends have been going in the wrong direction, so we definitely want to see a different trend in the earnings per share. NSL has impressed us by growing EPS at 20% per year over the past five years. While EPS is growing at a decent rate, but future growth could be limited by the amount of earnings being paid out to shareholders.

The Dividend Could Prove To Be Unreliable

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. While we generally think the level of distributions are a bit high, we wouldn't rule it out as becoming a good dividend payer in the future as its earnings are growing healthily. This company is not in the top tier of income providing stocks.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Taking the debate a bit further, we've identified 2 warning signs for NSL that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if NSL might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:N02

NSL

An investment holding company, engages in the manufacture and sale of building materials, oil and petroleum related products in Singapore, Malaysia, the United Arab Emirates, Finland, Norway, Germany, and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor