- Singapore

- /

- Capital Markets

- /

- SGX:AIY

iFAST And 2 Other Growth Stocks With Strong Insider Commitment

Reviewed by Simply Wall St

As global markets continue to reach record highs, driven by positive sentiment around domestic policy and geopolitical developments, investors are increasingly focused on identifying growth opportunities that align with these trends. In this context, companies with high insider ownership often signal strong commitment and confidence from those who know the business best, making them appealing candidates for those seeking robust growth potential in today's market environment.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| SKS Technologies Group (ASX:SKS) | 32.4% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.9% | 37.6% |

| On Holding (NYSE:ONON) | 19.1% | 29.6% |

| Pharma Mar (BME:PHM) | 11.8% | 56.2% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 111.4% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.7% | 63.6% |

| Alkami Technology (NasdaqGS:ALKT) | 10.9% | 98.6% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.6% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Let's explore several standout options from the results in the screener.

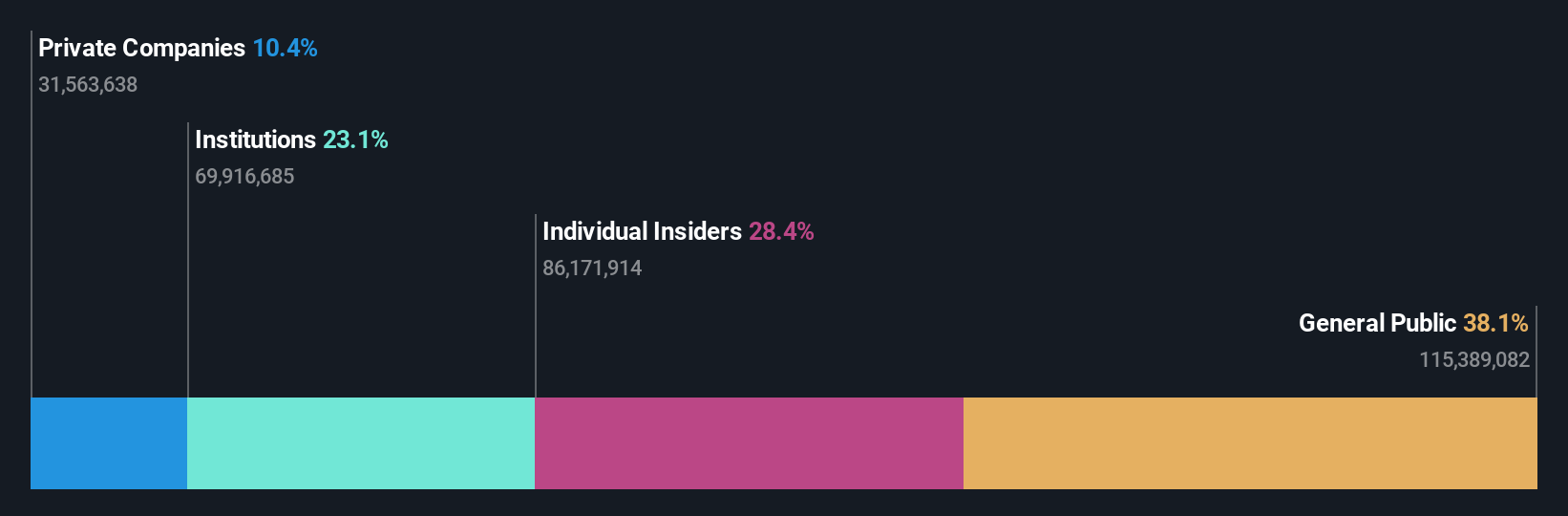

iFAST (SGX:AIY)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: iFAST Corporation Ltd. is a company that offers investment products and services across Singapore, Hong Kong, Malaysia, China, and the United Kingdom with a market cap of SGD2.29 billion.

Operations: Revenue Segments (in millions of SGD): The company generates revenue through its investment products and services offered across multiple regions, including Singapore, Hong Kong, Malaysia, China, and the United Kingdom.

Insider Ownership: 28.7%

Earnings Growth Forecast: 17.6% p.a.

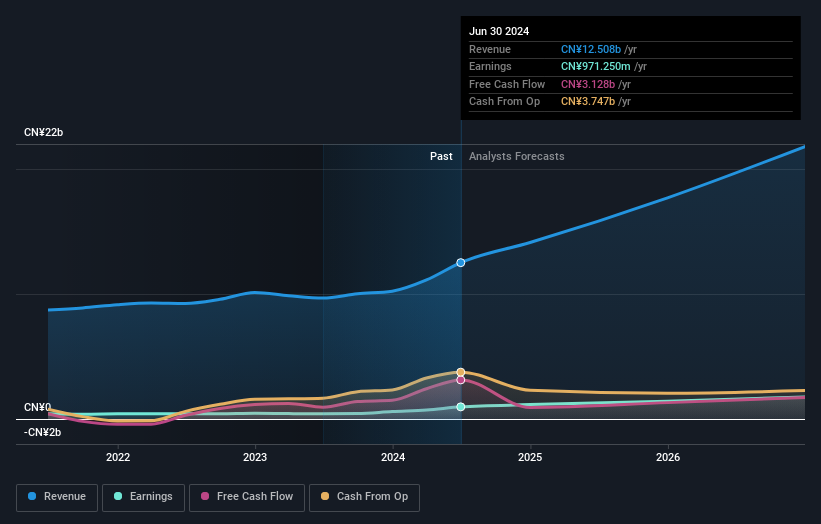

iFAST Corporation Ltd. demonstrates solid growth potential with its revenue and earnings expected to outpace the Singapore market, growing at 9.5% and 17.6% annually, respectively. The company reported significant financial improvements in Q3 2024, with net income reaching SGD 16.81 million, nearly doubling from the previous year. While insider ownership is high, recent executive changes may influence strategic direction; however, there is no substantial insider trading activity noted recently.

- Delve into the full analysis future growth report here for a deeper understanding of iFAST.

- Insights from our recent valuation report point to the potential overvaluation of iFAST shares in the market.

Ninebot (SHSE:689009)

Simply Wall St Growth Rating: ★★★★★★

Overview: Ninebot Limited is involved in the design, research and development, production, sale, and servicing of transportation and robot products globally, with a market cap of CN¥31.67 billion.

Operations: Revenue Segments (in millions of CN¥):

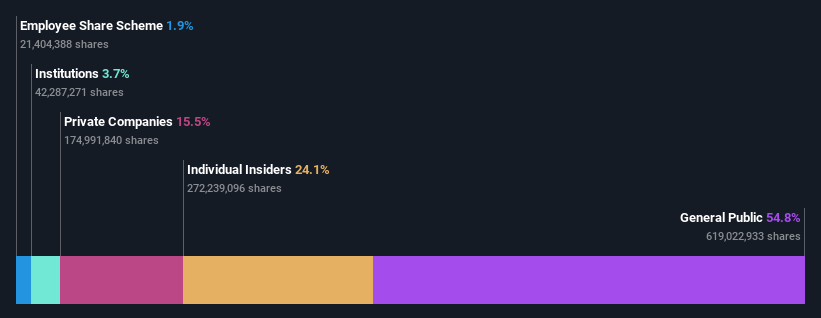

Insider Ownership: 16%

Earnings Growth Forecast: 27.6% p.a.

Ninebot Limited showcases strong growth potential, with its revenue and earnings forecasted to grow at 24.3% and 27.6% annually, surpassing the Chinese market averages. Recent earnings results highlight significant improvements, with net income reaching CNY 969.67 million for the first nine months of 2024, more than doubling from the previous year. Despite a favorable price-to-earnings ratio of 26.9x compared to the market's 36.7x, no substantial insider trading activity is reported recently.

- Click here to discover the nuances of Ninebot with our detailed analytical future growth report.

- In light of our recent valuation report, it seems possible that Ninebot is trading beyond its estimated value.

Tianrun Industry Technology (SZSE:002283)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Tianrun Industry Technology Co., Ltd. manufactures and sells internal combustion engine crankshafts both in China and internationally, with a market cap of CN¥5.86 billion.

Operations: Revenue Segments (in millions of CN¥): The company generates its revenue primarily from the production and sale of internal combustion engine crankshafts, serving both domestic and international markets.

Insider Ownership: 24.1%

Earnings Growth Forecast: 26.2% p.a.

Tianrun Industry Technology's growth prospects are underscored by an expected annual earnings increase of 26.2%, outpacing the Chinese market average. Revenue is also anticipated to grow at 16.8% annually, exceeding market expectations. Despite a recent decline in net income to CNY 268.96 million for the first nine months of 2024, the company trades at a favorable price-to-earnings ratio of 18.5x against the market's 36.7x, with no significant insider trading activity reported recently.

- Dive into the specifics of Tianrun Industry Technology here with our thorough growth forecast report.

- Upon reviewing our latest valuation report, Tianrun Industry Technology's share price might be too pessimistic.

Key Takeaways

- Click here to access our complete index of 1514 Fast Growing Companies With High Insider Ownership.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if iFAST might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:AIY

iFAST

Provides investment products and services in Singapore, Hong Kong, Malaysia, China, the United Kingdom.

Outstanding track record with excellent balance sheet.