- South Korea

- /

- Entertainment

- /

- KOSDAQ:A293490

3 Stocks That May Be Trading Below Their Estimated Value

Reviewed by Simply Wall St

As global markets navigate the early days of President Donald Trump's administration, optimism is buoyed by hopes for softer tariffs and enthusiasm surrounding artificial intelligence investments. Major indices like the S&P 500 have reached new heights, reflecting a positive sentiment despite political uncertainties and economic adjustments. In this environment, identifying stocks that may be trading below their estimated value can offer investors potential opportunities to capitalize on market inefficiencies and position themselves advantageously in a fluctuating landscape.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Aidma Holdings (TSE:7373) | ¥1822.00 | ¥3615.82 | 49.6% |

| Sichuan Injet Electric (SZSE:300820) | CN¥50.58 | CN¥100.77 | 49.8% |

| GlobalData (AIM:DATA) | £1.78 | £3.56 | 49.9% |

| Zhaojin Mining Industry (SEHK:1818) | HK$12.14 | HK$24.09 | 49.6% |

| Bufab (OM:BUFAB) | SEK464.20 | SEK926.28 | 49.9% |

| Nidaros Sparebank (OB:NISB) | NOK100.02 | NOK198.62 | 49.6% |

| GemPharmatech (SHSE:688046) | CN¥13.06 | CN¥25.94 | 49.7% |

| Greenworks (Jiangsu) (SZSE:301260) | CN¥13.83 | CN¥27.64 | 50% |

| South32 (ASX:S32) | A$3.36 | A$6.68 | 49.7% |

| Condor Energies (TSX:CDR) | CA$1.83 | CA$3.64 | 49.7% |

Underneath we present a selection of stocks filtered out by our screen.

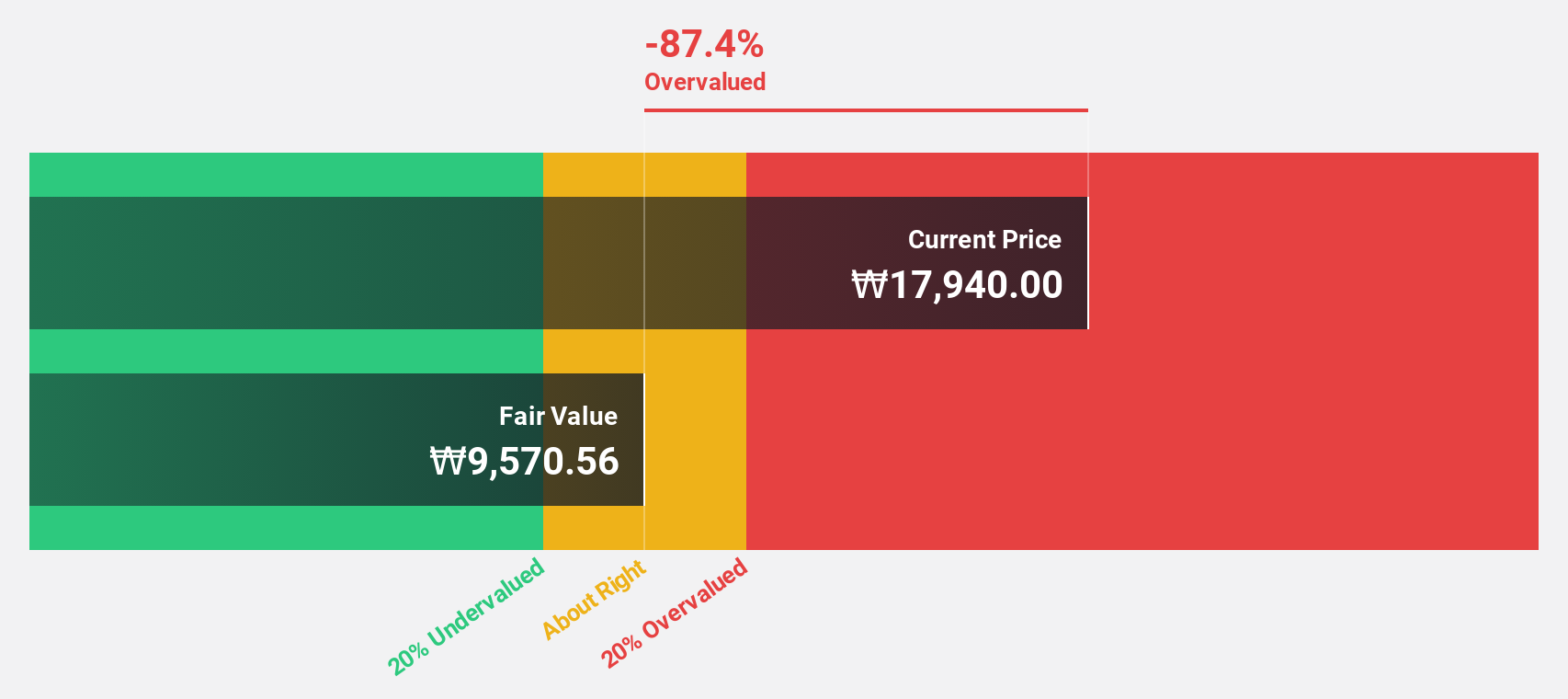

Kakao Games (KOSDAQ:A293490)

Overview: Kakao Games Corporation operates a mobile and PC online game service platform for gamers worldwide, with a market cap of ₩1.31 trillion.

Operations: The company generates revenue from its Computer Graphics segment, amounting to ₩951.76 million.

Estimated Discount To Fair Value: 17%

Kakao Games is trading 17% below its estimated fair value of ₩19,557.79, suggesting it may be undervalued based on cash flows. While revenue growth is projected at 9.4% annually, slightly above the Korean market average, profitability is expected within three years with earnings growth forecasted at a substantial rate annually. However, the anticipated return on equity remains low at 5.9%, which could limit potential returns despite the undervaluation signal from cash flow analysis.

- According our earnings growth report, there's an indication that Kakao Games might be ready to expand.

- Click here to discover the nuances of Kakao Games with our detailed financial health report.

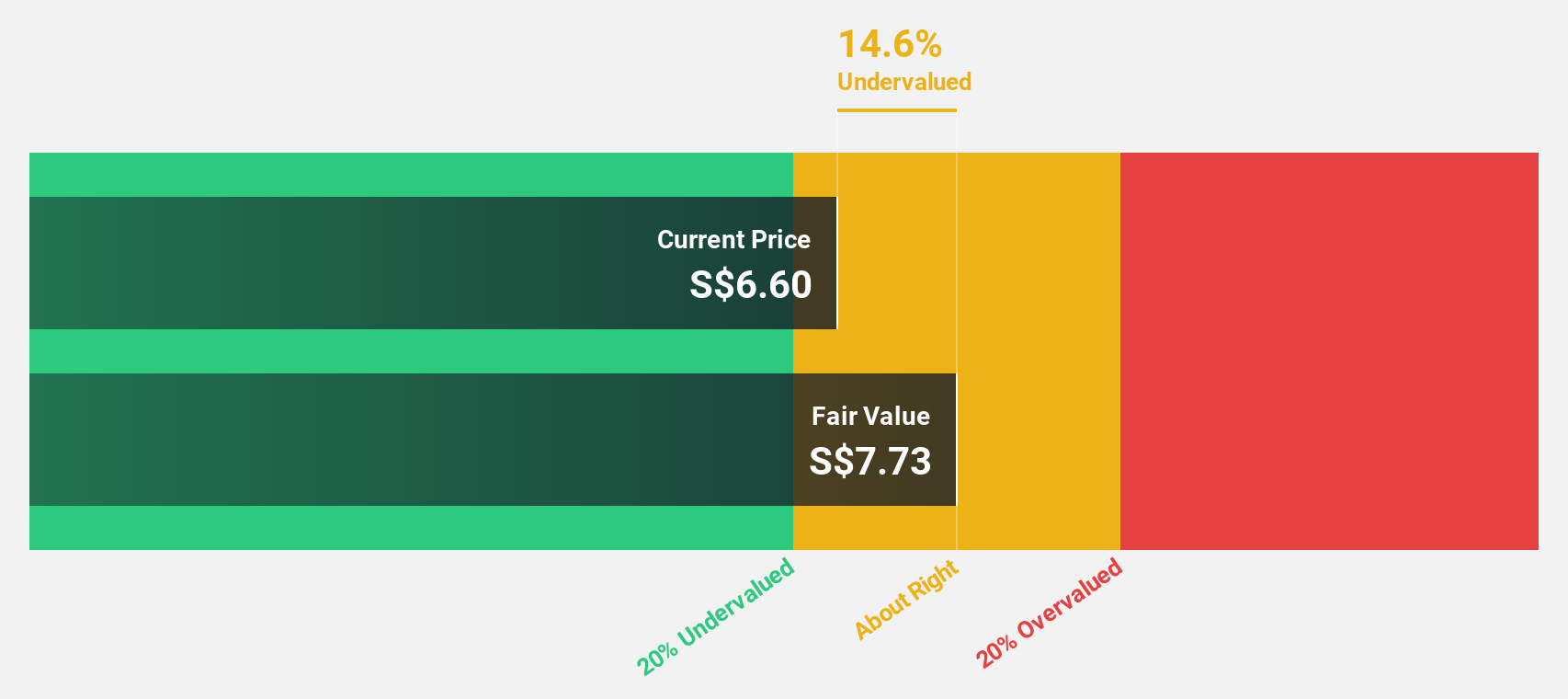

iFAST (SGX:AIY)

Overview: iFAST Corporation Ltd. offers investment products and services across Singapore, Hong Kong, Malaysia, China, and the United Kingdom with a market cap of SGD2.19 billion.

Operations: The company's revenue is derived from its operations in investment products and services across various regions, including Singapore, Hong Kong, Malaysia, China, and the United Kingdom.

Estimated Discount To Fair Value: 12.1%

iFAST is trading at S$7.47, below its estimated fair value of S$8.50, indicating potential undervaluation based on cash flows. The company's revenue is expected to grow at 9.1% annually, outpacing the Singapore market's 3.9% growth rate, while earnings are anticipated to increase by 14.75% per year, above the market average of 11.6%. Despite these positive indicators, the stock's undervaluation margin isn't significant enough to warrant high expectations solely from cash flow analysis.

- Our comprehensive growth report raises the possibility that iFAST is poised for substantial financial growth.

- Click here and access our complete balance sheet health report to understand the dynamics of iFAST.

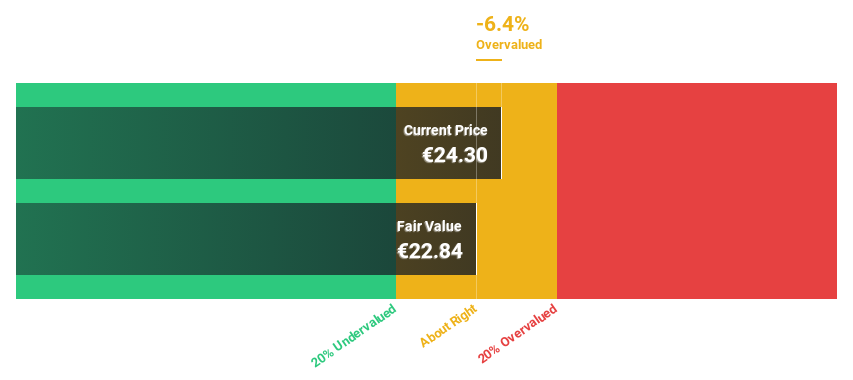

AMAG Austria Metall (WBAG:AMAG)

Overview: AMAG Austria Metall AG, along with its subsidiaries, is involved in the production, processing, and distribution of aluminum and aluminum products both in Austria and internationally, with a market cap of €846.34 million.

Operations: The company's revenue segments include Metal (€1.04 billion), Casting (€156.95 million), Rolling (€1.12 billion), and Service (€119.68 million).

Estimated Discount To Fair Value: 20.6%

AMAG Austria Metall, trading at €24.4, is priced over 20% below its estimated fair value of €30.71, highlighting potential undervaluation based on cash flows. Despite high debt levels and a dividend not fully covered by earnings or free cash flow, AMAG's earnings are forecast to grow significantly at 27.6% annually, surpassing the Austrian market average of 9.3%. However, recent impairment charges may impact short-term profitability with EBIT expected to be reduced by €15 million in 2024.

- The growth report we've compiled suggests that AMAG Austria Metall's future prospects could be on the up.

- Dive into the specifics of AMAG Austria Metall here with our thorough financial health report.

Summing It All Up

- Explore the 908 names from our Undervalued Stocks Based On Cash Flows screener here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kakao Games might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A293490

Kakao Games

Operates a mobile and PC online game service platform for gamers worldwide.

High growth potential with imperfect balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)