Advertisement

- Sweden

- /

- Tech Hardware

- /

- OM:TOBII

Tobii AB (publ) (STO:TOBII) Is Expected To Breakeven In The Near Future

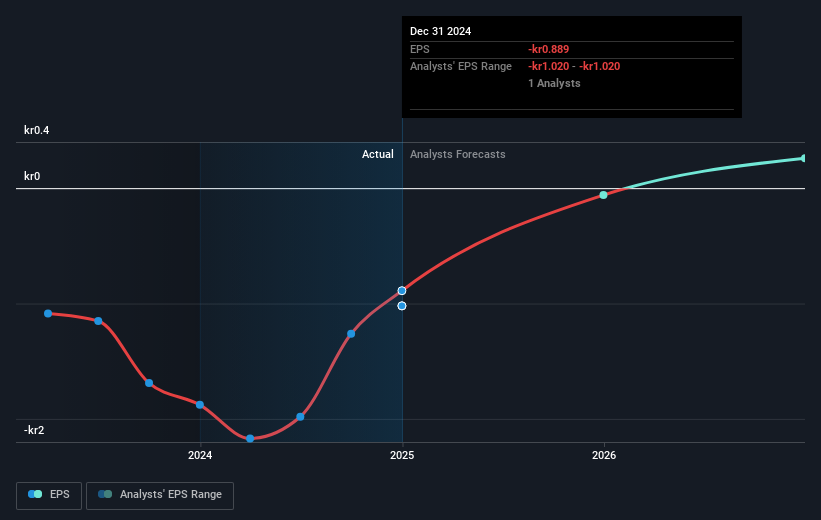

We feel now is a pretty good time to analyse Tobii AB (publ)'s (STO:TOBII) business as it appears the company may be on the cusp of a considerable accomplishment. Tobii AB (publ) develops and sells eye-tracking technology and solutions in Sweden, Asia, Europe, North America, and internationally. On 31 December 2024, the kr515m market-cap company posted a loss of kr177m for its most recent financial year. The most pressing concern for investors is Tobii's path to profitability – when will it breakeven? In this article, we will touch on the expectations for the company's growth and when analysts expect it to become profitable.

Expectations from some of the Swedish Tech analysts is that Tobii is on the verge of breakeven. They anticipate the company to incur a final loss in 2025, before generating positive profits of kr37m in 2026. So, the company is predicted to breakeven just over a year from now. In order to meet this breakeven date, we calculated the rate at which the company must grow year-on-year. It turns out an average annual growth rate of 144% is expected, which is rather optimistic! If this rate turns out to be too aggressive, the company may become profitable much later than analysts predict.

Given this is a high-level overview, we won’t go into details of Tobii's upcoming projects, but, keep in mind that by and large a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

Check out our latest analysis for Tobii

Before we wrap up, there’s one issue worth mentioning. Tobii currently has a relatively high level of debt. Typically, debt shouldn’t exceed 40% of your equity, which in Tobii's case is 49%. Note that a higher debt obligation increases the risk in investing in the loss-making company.

Next Steps:

There are too many aspects of Tobii to cover in one brief article, but the key fundamentals for the company can all be found in one place – Tobii's company page on Simply Wall St. We've also put together a list of pertinent factors you should look at:

- Historical Track Record: What has Tobii's performance been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Tobii's board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

Valuation is complex, but we're here to simplify it.

Discover if Tobii might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:TOBII

Tobii

Develops and sells eye-tracking technology and solutions in Sweden, Europe, Middle East, Africa, the United States, and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor