Advertisement

- Sweden

- /

- Communications

- /

- OM:ERIC B

VodafoneThree’s Core Network Deal Could Be a Game Changer for Ericsson (OM:ERIC B)

Simply Wall St

Reviewed by Sasha Jovanovic

- On September 22, 2025, VodafoneThree announced it selected Ericsson to power the majority of its next-generation UK mobile network, including the entire core network, through a SEK12.5 billion (almost £1 billion) eight-year partnership, covering extensive deployment of Ericsson's 5G Standalone solutions in major UK cities.

- This exclusive deal positions Ericsson as the sole nationwide core network vendor for one of Europe's largest network consolidation undertakings, highlighting the company's expanding influence in key telecom infrastructure upgrades.

- We'll explore how securing sole core network vendor status in the UK could shape Ericsson's investment narrative and growth outlook.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Telefonaktiebolaget LM Ericsson Investment Narrative Recap

Investors in Ericsson are often drawn by the company’s global role in 5G and advanced telecom infrastructure, banking on rising demand for next-generation network equipment and monetization through enterprise connectivity. The recent SEK12.5 billion VodafoneThree deal reaffirms Ericsson’s technology leadership and strengthens its growth catalysts in core markets, though in the short term, the primary risk remains exposure to geopolitical shifts and intensified competition rather than immediate financial impact from this single contract.

Alongside this major win, Ericsson’s private 5G deployment at Hitachi Rail in Maryland stands out, showcasing the firm’s ability to capture industrial digital transformation opportunities. Such industry partnerships support Ericsson’s long-term catalyst, the global shift towards AI-powered, high-performance networks, even as the company faces margin pressures and evolving market risks.

By contrast, investors should be aware that ongoing uncertainty from trade restrictions and heightened geopolitical friction continues to ...

Read the full narrative on Telefonaktiebolaget LM Ericsson (it's free!)

Telefonaktiebolaget LM Ericsson's narrative projects SEK242.3 billion in revenue and SEK18.2 billion in earnings by 2028. This is based on a -0.5% annual revenue decline and a SEK0.9 billion earnings increase from the current SEK17.3 billion.

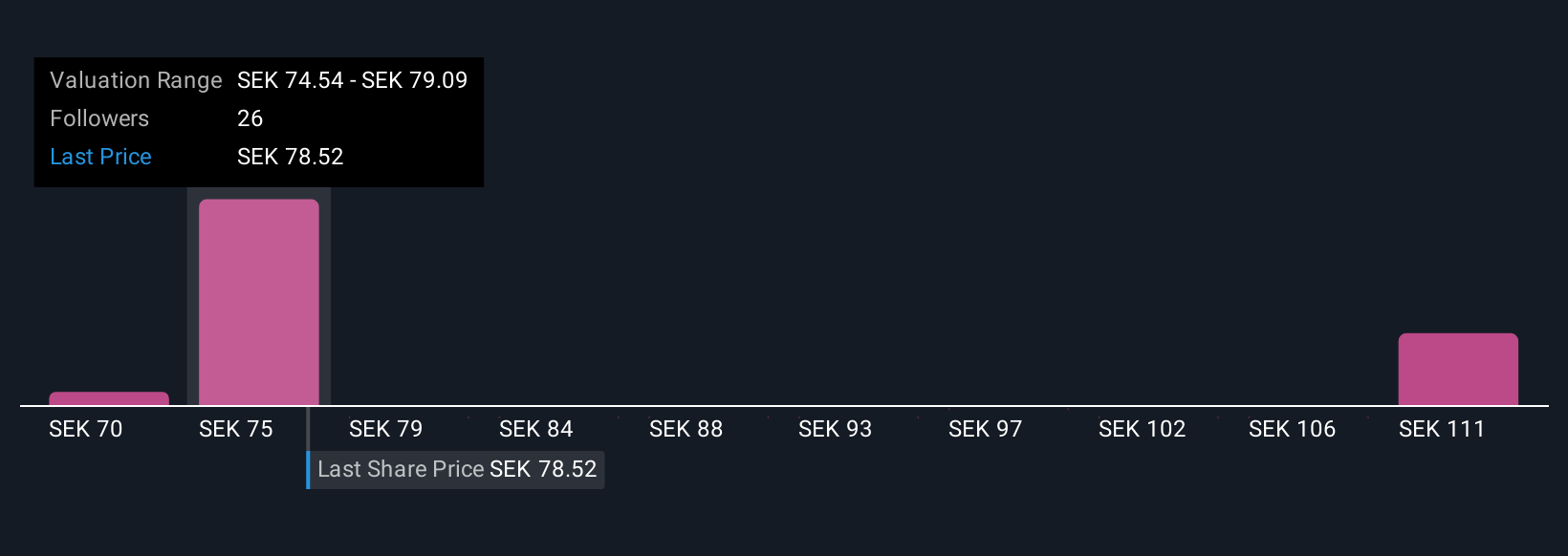

Uncover how Telefonaktiebolaget LM Ericsson's forecasts yield a SEK77.62 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members offered six distinct fair value estimates for Ericsson, ranging from SEK69.99 to SEK115.35. With many seeing opportunity in 5G growth, but risks from geopolitical and regulatory headwinds, it’s clear opinions vary, explore several different viewpoints for a fuller picture.

Explore 6 other fair value estimates on Telefonaktiebolaget LM Ericsson - why the stock might be worth as much as 47% more than the current price!

Build Your Own Telefonaktiebolaget LM Ericsson Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Telefonaktiebolaget LM Ericsson research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Telefonaktiebolaget LM Ericsson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Telefonaktiebolaget LM Ericsson's overall financial health at a glance.

No Opportunity In Telefonaktiebolaget LM Ericsson?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Rare earth metals are the new gold rush. Find out which 32 stocks are leading the charge.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Telefonaktiebolaget LM Ericsson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:ERIC B

Telefonaktiebolaget LM Ericsson

Provides mobile connectivity solutions to communications service providers, enterprises, and the public sector.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor