Advertisement

- Sweden

- /

- Electronic Equipment and Components

- /

- NGM:BPCINS

Declining Stock and Solid Fundamentals: Is The Market Wrong About BPC Instruments AB (NGM:BPCINS)?

With its stock down 15% over the past month, it is easy to disregard BPC Instruments (NGM:BPCINS). But if you pay close attention, you might gather that its strong financials could mean that the stock could potentially see an increase in value in the long-term, given how markets usually reward companies with good financial health. Particularly, we will be paying attention to BPC Instruments' ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for BPC Instruments

How Is ROE Calculated?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for BPC Instruments is:

23% = kr11m ÷ kr46m (Based on the trailing twelve months to September 2023).

The 'return' is the profit over the last twelve months. So, this means that for every SEK1 of its shareholder's investments, the company generates a profit of SEK0.23.

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of BPC Instruments' Earnings Growth And 23% ROE

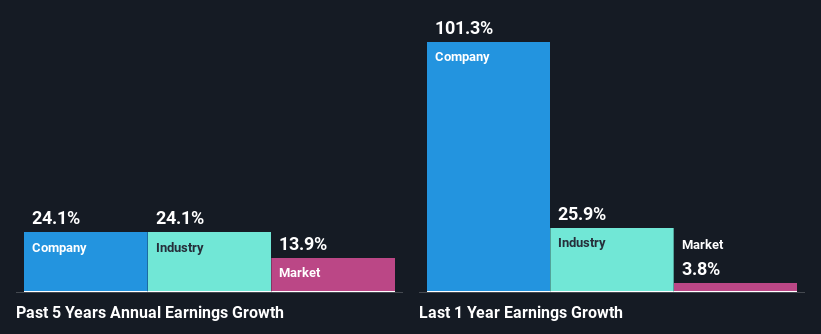

First thing first, we like that BPC Instruments has an impressive ROE. Additionally, the company's ROE is higher compared to the industry average of 18% which is quite remarkable. Under the circumstances, BPC Instruments' considerable five year net income growth of 24% was to be expected.

As a next step, we compared BPC Instruments' net income growth with the industry and found that the company has a similar growth figure when compared with the industry average growth rate of 24% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if BPC Instruments is trading on a high P/E or a low P/E, relative to its industry.

Is BPC Instruments Making Efficient Use Of Its Profits?

Given that BPC Instruments doesn't pay any dividend to its shareholders, we infer that the company has been reinvesting all of its profits to grow its business.

Summary

On the whole, we feel that BPC Instruments' performance has been quite good. In particular, it's great to see that the company is investing heavily into its business and along with a high rate of return, that has resulted in a sizeable growth in its earnings. If the company continues to grow its earnings the way it has, that could have a positive impact on its share price given how earnings per share influence long-term share prices. Remember, the price of a stock is also dependent on the perceived risk. Therefore investors must keep themselves informed about the risks involved before investing in any company. To know the 3 risks we have identified for BPC Instruments visit our risks dashboard for free.

Valuation is complex, but we're here to simplify it.

Discover if BPC Instruments might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NGM:BPCINS

BPC Instruments

A technology company, develops, manufactures, and sells analytical instruments in Sweden and internationally.

Flawless balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor