3 Swedish Growth Companies With High Insider Ownership And Up To 98% Earnings Growth

Reviewed by Simply Wall St

As global markets face heightened tensions and economic uncertainties, the European market has also experienced a downturn with major indices like the STOXX Europe 600 Index declining due to escalating conflicts in the Middle East. Amidst this backdrop, investors are increasingly looking towards growth companies with high insider ownership as these entities often signal strong confidence from those closest to the business. In Sweden, such companies are particularly noteworthy for their potential resilience and capacity for earnings growth even in challenging times.

Top 10 Growth Companies With High Insider Ownership In Sweden

| Name | Insider Ownership | Earnings Growth |

| CTT Systems (OM:CTT) | 16.9% | 24.8% |

| Truecaller (OM:TRUE B) | 29.6% | 21.6% |

| Magle Chemoswed Holding (OM:MAGLE) | 14.9% | 72.2% |

| Biovica International (OM:BIOVIC B) | 18.3% | 78.5% |

| BioArctic (OM:BIOA B) | 34% | 98.4% |

| KebNi (OM:KEBNI B) | 36.3% | 86.1% |

| Yubico (OM:YUBICO) | 37.5% | 42.3% |

| InCoax Networks (OM:INCOAX) | 19.5% | 115.5% |

| C-Rad (OM:CRAD B) | 16.1% | 33.9% |

| OrganoClick (OM:ORGC) | 23.1% | 109.0% |

Let's dive into some prime choices out of the screener.

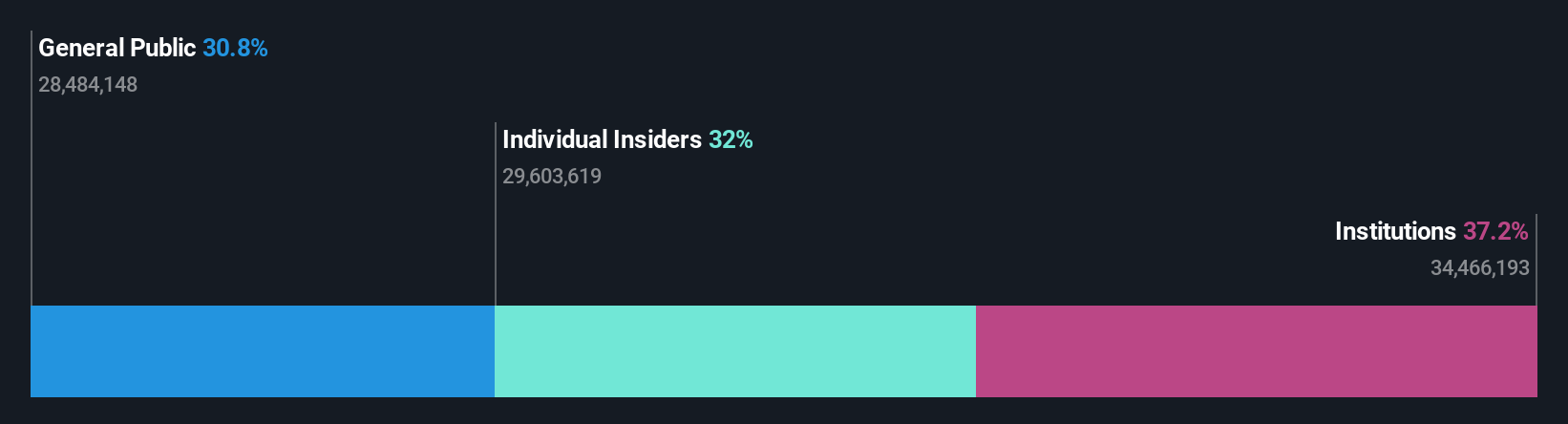

Bilia (OM:BILI A)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Bilia AB (publ) is a full-service supplier for car ownership operating in Sweden, Norway, Luxembourg, and Belgium with a market cap of SEK10.48 billion.

Operations: The company's revenue segments include Fuel (SEK1.03 billion), Car - Norway (SEK7.14 billion), Car - Sweden (SEK19.89 billion), Service - Norway (SEK2.26 billion), Service - Sweden (SEK6.33 billion), Car - Western Europe (SEK3.59 billion), and Service - Western Europe (SEK670 million).

Insider Ownership: 31.4%

Earnings Growth Forecast: 19.5% p.a.

Bilia's earnings are forecast to grow at 19.47% annually, outpacing the Swedish market's 15.2%, though its revenue growth of 5.1% lags behind significant benchmarks. Despite trading at a substantial discount to its estimated fair value, Bilia faces challenges with high debt levels and declining profit margins—down from 3.1% to 2%. Recent earnings reports show increased sales but decreased net income and EPS compared to last year, indicating mixed financial health.

- Get an in-depth perspective on Bilia's performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that Bilia's share price might be on the cheaper side.

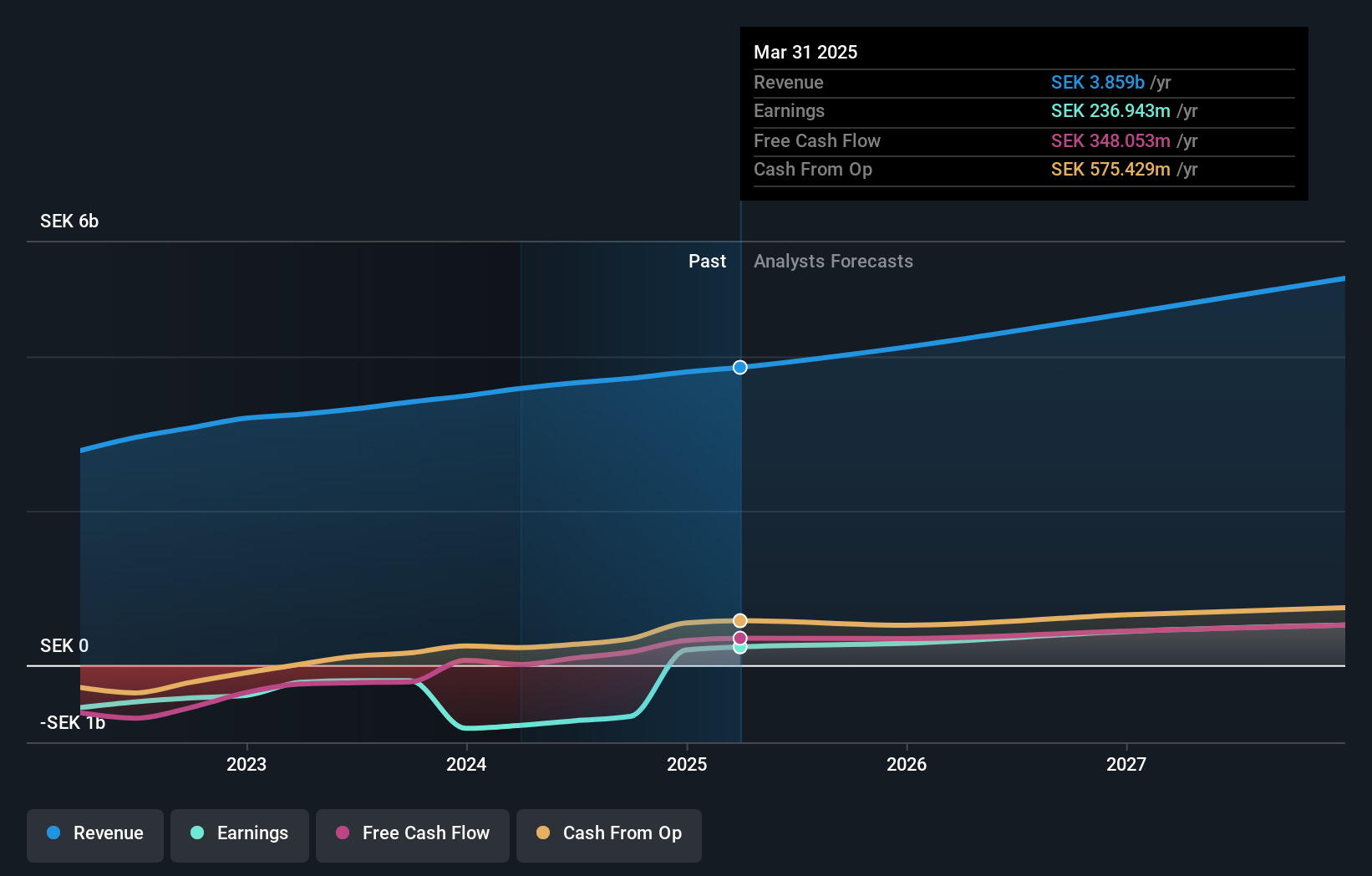

Storytel (OM:STORY B)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Storytel AB (publ) offers streaming services for audiobooks and e-books, with a market cap of SEK4.54 billion.

Operations: The company's revenue is primarily derived from its books segment, which generated SEK825.91 million.

Insider Ownership: 19.5%

Earnings Growth Forecast: 98.7% p.a.

Storytel's growth trajectory is bolstered by high insider ownership and recent strategic moves, including a partnership with Wellhub to expand audiobook access across Latin America and Europe. The company has seen substantial insider buying in the past three months, indicating confidence in its prospects. Forecasts suggest Storytel will achieve profitability within three years, with revenue growth expected to outpace the Swedish market. Currently trading significantly below estimated fair value, it presents an intriguing investment case despite slower-than-desired revenue expansion rates.

- Unlock comprehensive insights into our analysis of Storytel stock in this growth report.

- Our valuation report unveils the possibility Storytel's shares may be trading at a discount.

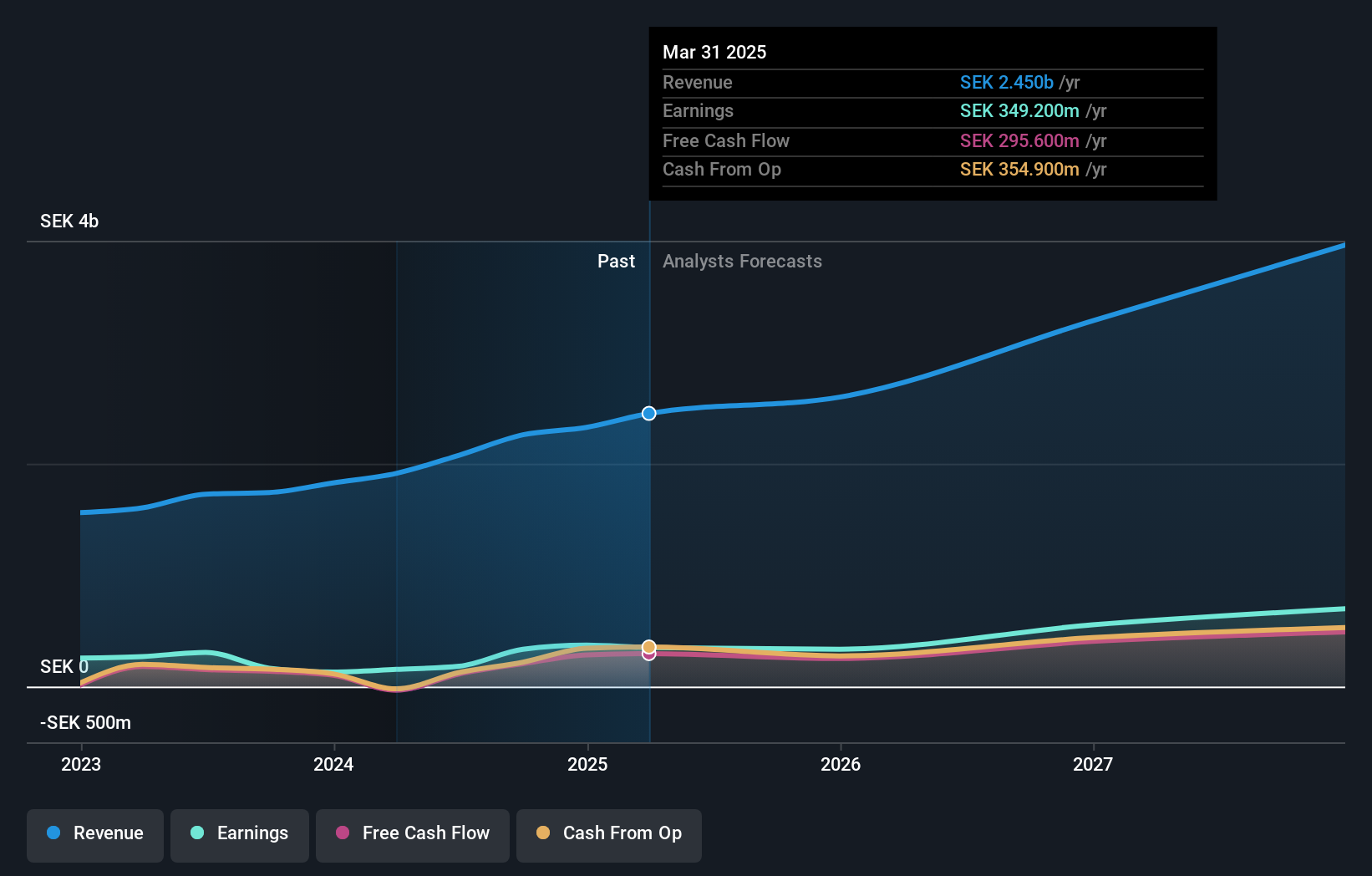

Yubico (OM:YUBICO)

Simply Wall St Growth Rating: ★★★★★★

Overview: Yubico AB offers authentication solutions for computers, networks, and online services with a market cap of SEK23.16 billion.

Operations: The company's revenue is derived from its Security Software & Services segment, totaling SEK2.09 billion.

Insider Ownership: 37.5%

Earnings Growth Forecast: 42.3% p.a.

Yubico demonstrates strong growth potential with high insider ownership, highlighted by its recent partnership with PKO Bank Polski to enhance security using YubiKeys. The company's revenue and earnings are forecasted to grow significantly faster than the Swedish market, at 20.5% and 42.3% annually, respectively. Despite volatility in share price and declining profit margins from last year, Yubico's strategic initiatives in cybersecurity bolster its position as a leader in phishing-resistant authentication solutions.

- Delve into the full analysis future growth report here for a deeper understanding of Yubico.

- According our valuation report, there's an indication that Yubico's share price might be on the expensive side.

Summing It All Up

- Reveal the 79 hidden gems among our Fast Growing Swedish Companies With High Insider Ownership screener with a single click here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:YUBICO

Yubico

Provides authentication solutions for use in computers, networks, and online services.

Exceptional growth potential with excellent balance sheet.