Advertisement

Upgrade: The Latest Revenue Forecasts For Pagero Group Ab (Publ) (STO:PAGERO)

Pagero Group Ab (Publ) (STO:PAGERO) shareholders will have a reason to smile today, with the covering analyst making substantial upgrades to next year's statutory forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

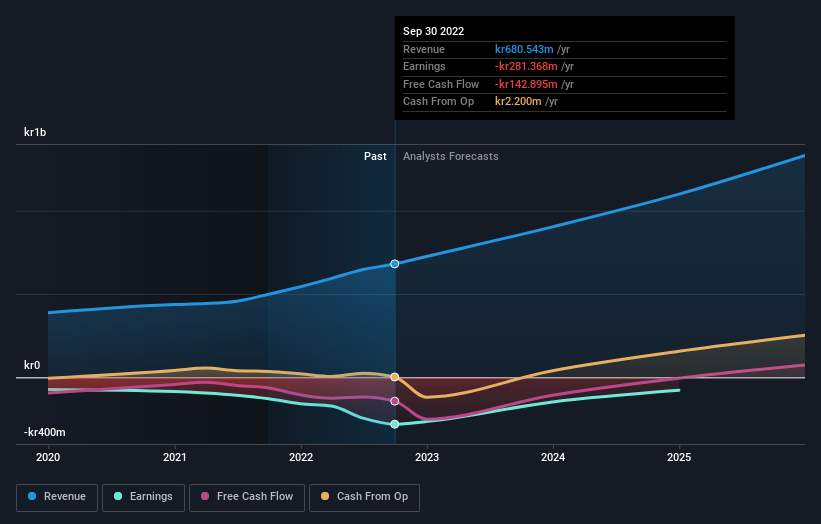

Following the upgrade, the most recent consensus for Pagero Group from its solo analyst is for revenues of kr903m in 2023 which, if met, would be a major 33% increase on its sales over the past 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 50% to kr0.90. However, before this estimates update, the consensus had been expecting revenues of kr748m and kr0.92 per share in losses. We can see there's definitely been a change in sentiment in this update, with the analyst administering a sizeable upgrade to next year's revenue estimates, while at the same time reducing their loss estimates.

See our latest analysis for Pagero Group

The consensus price target rose 5.9% to kr18.00, with the analyst encouraged by the higher revenue and lower forecast losses for next year.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. The period to the end of 2023 brings more of the same, according to the analyst, with revenue forecast to display 25% growth on an annualised basis. That is in line with its 22% annual growth over the past three years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 17% annually. So although Pagero Group is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses next year, perhaps suggesting Pagero Group is moving incrementally towards profitability. Fortunately, the analyst also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. There was also a nice increase in the price target, with the analyst apparently feeling that the intrinsic value of the business is improving. Seeing the dramatic upgrade to next year's forecasts, it might be time to take another look at Pagero Group.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have analyst estimates for Pagero Group going out as far as 2025, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:PAGERO

Pagero Group

Pagero Group AB (publ) provides cloud-based networks that connect buyers, suppliers, partners, banks, and authorities to digitize and automates purchase-to-pay (P2P) and order-to-cash (O2C) processes in Sweden and internationally.

Concerning outlook with worrying balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor