Advertisement

- Sweden

- /

- Construction

- /

- OM:NYAB

3 Swedish Stocks That Could Be Trading Below Their Estimated Value

Simply Wall St

Reviewed by Simply Wall St

As the pan-European STOXX Europe 600 Index experiences a modest rise amid hopes for quicker interest rate cuts by the European Central Bank, investors are closely watching Sweden's market for potential opportunities. In this environment, identifying stocks that might be trading below their estimated value can be a strategic approach, especially when considering factors such as company fundamentals and broader economic conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Sweden

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Truecaller (OM:TRUE B) | SEK45.54 | SEK89.05 | 48.9% |

| Concentric (OM:COIC) | SEK213.50 | SEK404.69 | 47.2% |

| Lindab International (OM:LIAB) | SEK272.20 | SEK526.86 | 48.3% |

| Telefonaktiebolaget LM Ericsson (OM:ERIC B) | SEK88.36 | SEK174.84 | 49.5% |

| Wall to Wall Group (OM:WTW A) | SEK55.00 | SEK104.53 | 47.4% |

| Securitas (OM:SECU B) | SEK130.80 | SEK259.32 | 49.6% |

| TF Bank (OM:TFBANK) | SEK315.00 | SEK617.94 | 49% |

| OptiCept Technologies (OM:OPTI) | SEK7.13 | SEK13.68 | 47.9% |

| BHG Group (OM:BHG) | SEK13.91 | SEK26.37 | 47.2% |

| Bactiguard Holding (OM:BACTI B) | SEK46.50 | SEK86.31 | 46.1% |

Let's explore several standout options from the results in the screener.

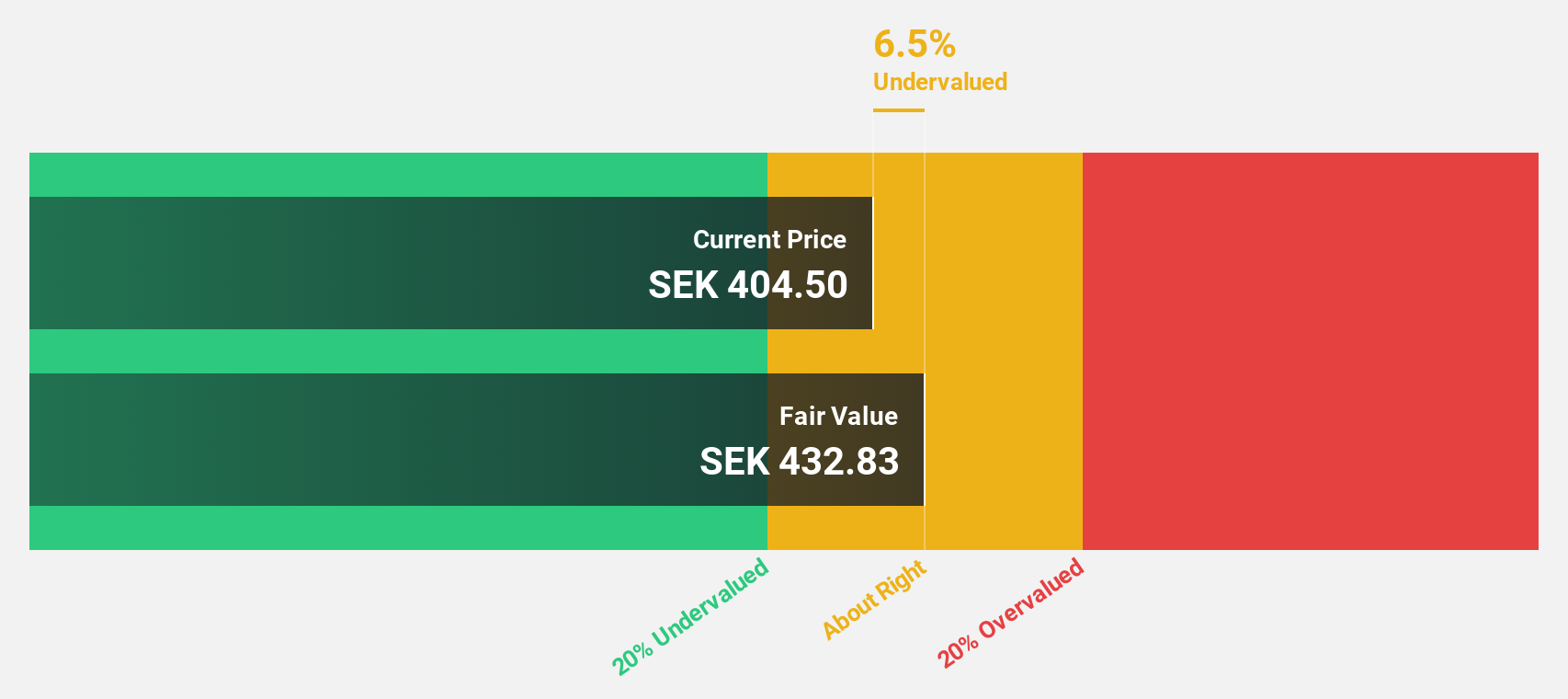

Lime Technologies (OM:LIME)

Overview: Lime Technologies AB (publ) offers SaaS-based CRM solutions in the Nordic region and has a market cap of SEK4.44 billion.

Operations: The company's revenue primarily comes from selling and implementing CRM systems, totaling SEK631.84 million.

Estimated Discount To Fair Value: 28.5%

Lime Technologies, trading at SEK334.5, is undervalued with a discounted cash flow estimate of SEK467.51. Despite high debt levels, the stock trades 28.5% below its fair value estimate and offers strong potential for growth in earnings—forecasted to increase significantly by over 20% annually over the next three years. While revenue growth is slower at 14.2%, it still outpaces the Swedish market average of 1.2%.

- Our earnings growth report unveils the potential for significant increases in Lime Technologies' future results.

- Click here to discover the nuances of Lime Technologies with our detailed financial health report.

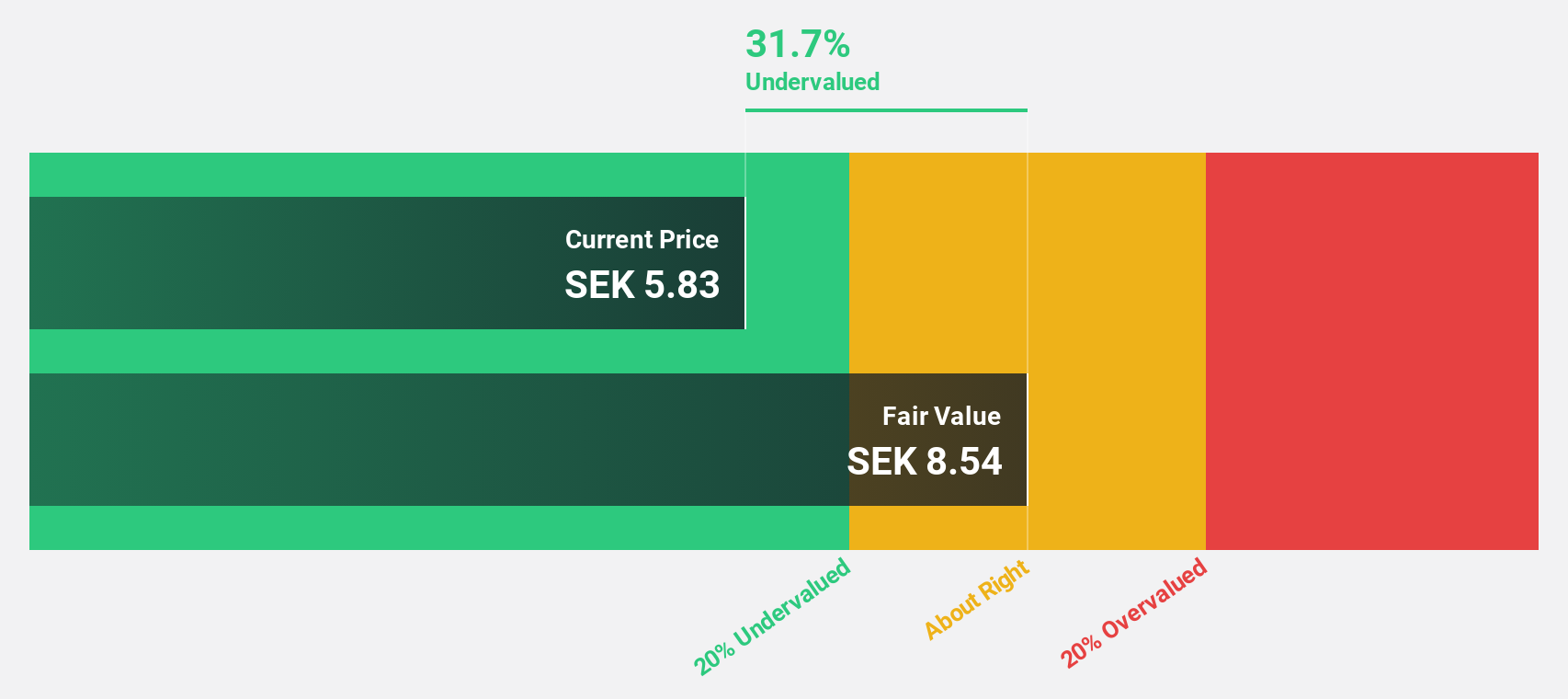

Nyab (OM:NYAB)

Overview: Nyab AB (publ) operates in Finland and Sweden, offering engineering, construction, and maintenance services for energy, infrastructure, and industrial projects across public and private sectors with a market cap of SEK4.07 billion.

Operations: The company's revenue segment for Heavy Construction is €308.95 million.

Estimated Discount To Fair Value: 44%

Nyab is trading at SEK5.73, significantly below its estimated fair value of SEK10.22, offering potential upside based on cash flow analysis. Despite a forecasted revenue growth rate of 11.2% per year, which surpasses the Swedish market average, profit margins have declined to 2.9% from 7.4% last year. However, earnings are expected to grow substantially by 28.1% annually over the next three years, outpacing the broader market's growth expectations of 15.3%.

- The growth report we've compiled suggests that Nyab's future prospects could be on the up.

- Dive into the specifics of Nyab here with our thorough financial health report.

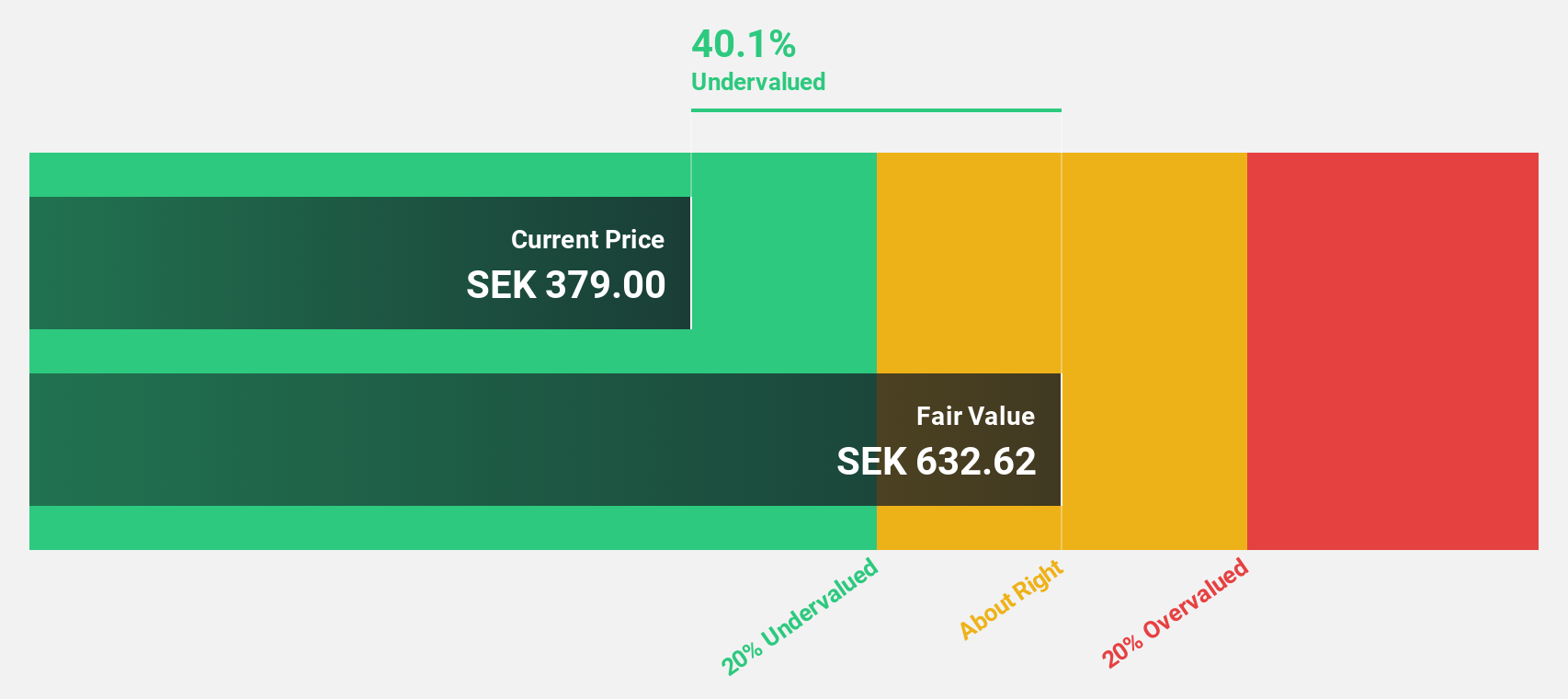

TF Bank (OM:TFBANK)

Overview: TF Bank AB (publ) is a digital bank that offers consumer banking services and e-commerce solutions via its proprietary IT platform, with a market cap of SEK6.77 billion.

Operations: TF Bank generates revenue from three primary segments: Credit Cards (SEK511.24 million), Consumer Lending (SEK607.24 million), and Ecommerce Solutions excluding Credit Cards (SEK363.28 million).

Estimated Discount To Fair Value: 49%

TF Bank is trading at SEK315, substantially below its estimated fair value of SEK617.94, highlighting potential undervaluation based on cash flow analysis. With projected annual earnings growth of 31.6%, it surpasses the Swedish market's forecasted growth of 15.3%. Revenue is expected to rise by 34.1% annually, significantly outpacing the market average. However, concerns include a high level of non-performing loans at 10.6% and a low allowance for bad loans at 62%.

- The analysis detailed in our TF Bank growth report hints at robust future financial performance.

- Click to explore a detailed breakdown of our findings in TF Bank's balance sheet health report.

Make It Happen

- Click here to access our complete index of 46 Undervalued Swedish Stocks Based On Cash Flows.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nyab might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:NYAB

Nyab

Provides engineering, construction, and maintenance services to energy, infrastructure, and industrial construction projects for public and private sectors in Finland and Sweden.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|18.3% undervalued

BL

Community Contributor