Advertisement

- Sweden

- /

- Paper and Forestry Products

- /

- OM:NPAPER

Nordic Paper Holding AB (publ) Just Recorded A 28% EPS Beat: Here's What Analysts Are Forecasting Next

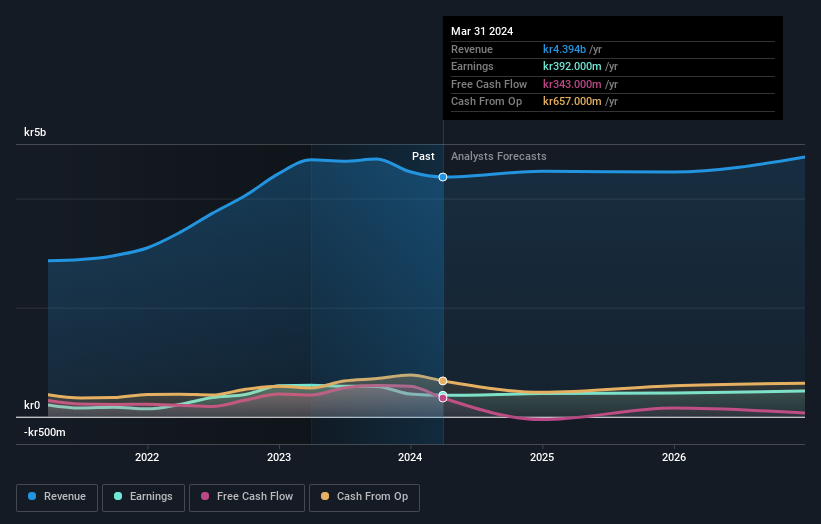

Investors in Nordic Paper Holding AB (publ) (STO:NPAPER) had a good week, as its shares rose 2.5% to close at kr55.50 following the release of its quarterly results. It looks like a credible result overall - although revenues of kr1.2b were what the analysts expected, Nordic Paper Holding surprised by delivering a (statutory) profit of kr2.23 per share, an impressive 28% above what was forecast. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

See our latest analysis for Nordic Paper Holding

Taking into account the latest results, the consensus forecast from Nordic Paper Holding's twin analysts is for revenues of kr4.50b in 2024. This reflects a modest 2.4% improvement in revenue compared to the last 12 months. Per-share earnings are expected to increase 8.2% to kr6.34. Yet prior to the latest earnings, the analysts had been anticipated revenues of kr4.58b and earnings per share (EPS) of kr6.16 in 2024. So the consensus seems to have become somewhat more optimistic on Nordic Paper Holding's earnings potential following these results.

The consensus price target rose 8.3% to kr65.00, suggesting that higher earnings estimates flow through to the stock's valuation as well.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that Nordic Paper Holding's revenue growth is expected to slow, with the forecast 3.2% annualised growth rate until the end of 2024 being well below the historical 18% p.a. growth over the last three years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 4.3% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Nordic Paper Holding.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Nordic Paper Holding's earnings potential next year. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting that it's tracking in line with expectations. Although our data does suggest that Nordic Paper Holding's revenue is expected to perform worse than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Nordic Paper Holding going out as far as 2026, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 2 warning signs for Nordic Paper Holding that you should be aware of.

Valuation is complex, but we're here to simplify it.

Discover if Nordic Paper Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:NPAPER

Nordic Paper Holding

Engages in the production and sale of natural greaseproof and kraft paper in Sweden, Italy, Germany, the United Kingdom, rest of Europe, the United States, and internationally.

Mediocre balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor