Swedish Exchange Stocks Estimated To Be 33.2% To 45.7% Below Intrinsic Value

Reviewed by Simply Wall St

As global markets react to China's robust stimulus measures and mixed economic signals from major economies, the Swedish market has seen its own share of fluctuations. Amid these developments, certain stocks on the Swedish exchange are estimated to be significantly undervalued, presenting potential opportunities for investors. In this environment, identifying stocks that are trading below their intrinsic value can be particularly advantageous. These undervalued stocks may offer a margin of safety and potential for growth as market conditions stabilize or improve.

Top 10 Undervalued Stocks Based On Cash Flows In Sweden

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Concentric (OM:COIC) | SEK221.00 | SEK406.67 | 45.7% |

| Biotage (OM:BIOT) | SEK185.50 | SEK364.34 | 49.1% |

| Lindab International (OM:LIAB) | SEK288.00 | SEK530.76 | 45.7% |

| Cavotec (OM:CCC) | SEK21.00 | SEK41.43 | 49.3% |

| Mentice (OM:MNTC) | SEK27.70 | SEK50.89 | 45.6% |

| Tourn International (OM:TOURN) | SEK9.06 | SEK16.49 | 45% |

| Svedbergs Group (OM:SVED BTA B) | SEK36.30 | SEK65.51 | 44.6% |

| Nexam Chemical Holding (OM:NEXAM) | SEK4.25 | SEK7.92 | 46.4% |

| MilDef Group (OM:MILDEF) | SEK84.70 | SEK160.55 | 47.2% |

| Lyko Group (OM:LYKO A) | SEK113.40 | SEK214.28 | 47.1% |

We're going to check out a few of the best picks from our screener tool.

Billerud (OM:BILL)

Overview: Billerud AB (publ) is a global provider of paper and packaging materials with a market cap of SEK28.92 billion.

Operations: The company's revenue segments are comprised of SEK27.08 billion from Region Europe, SEK11.35 billion from Region North America, and SEK2.77 billion from Solution & Other (excluding Currency Hedging).

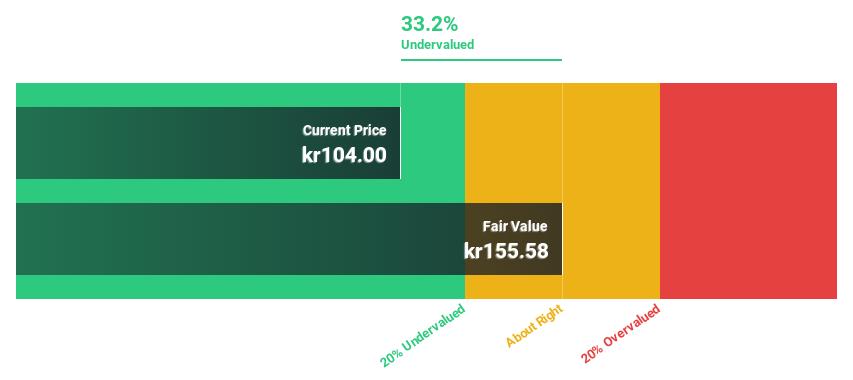

Estimated Discount To Fair Value: 33.2%

Billerud, currently trading at SEK116.3, is significantly undervalued based on discounted cash flow analysis with an estimated fair value of SEK174.11. Despite a forecasted low return on equity (8.6%) in three years and unstable dividend history, its earnings are expected to grow 31.44% annually, outpacing the Swedish market's 15.1%. Recent leadership changes and improved net income from SEK481 million loss to SEK63 million profit in Q2 2024 further bolster its investment appeal based on cash flows.

- Upon reviewing our latest growth report, Billerud's projected financial performance appears quite optimistic.

- Navigate through the intricacies of Billerud with our comprehensive financial health report here.

Concentric (OM:COIC)

Overview: Concentric AB (publ) and its subsidiaries design, develop, manufacture, and distribute hydraulic and engine solutions in Sweden and internationally, with a market cap of SEK8.20 billion.

Operations: The company's revenue segments are Engines (SEK2.71 billion) and Hydraulics (SEK1.25 billion).

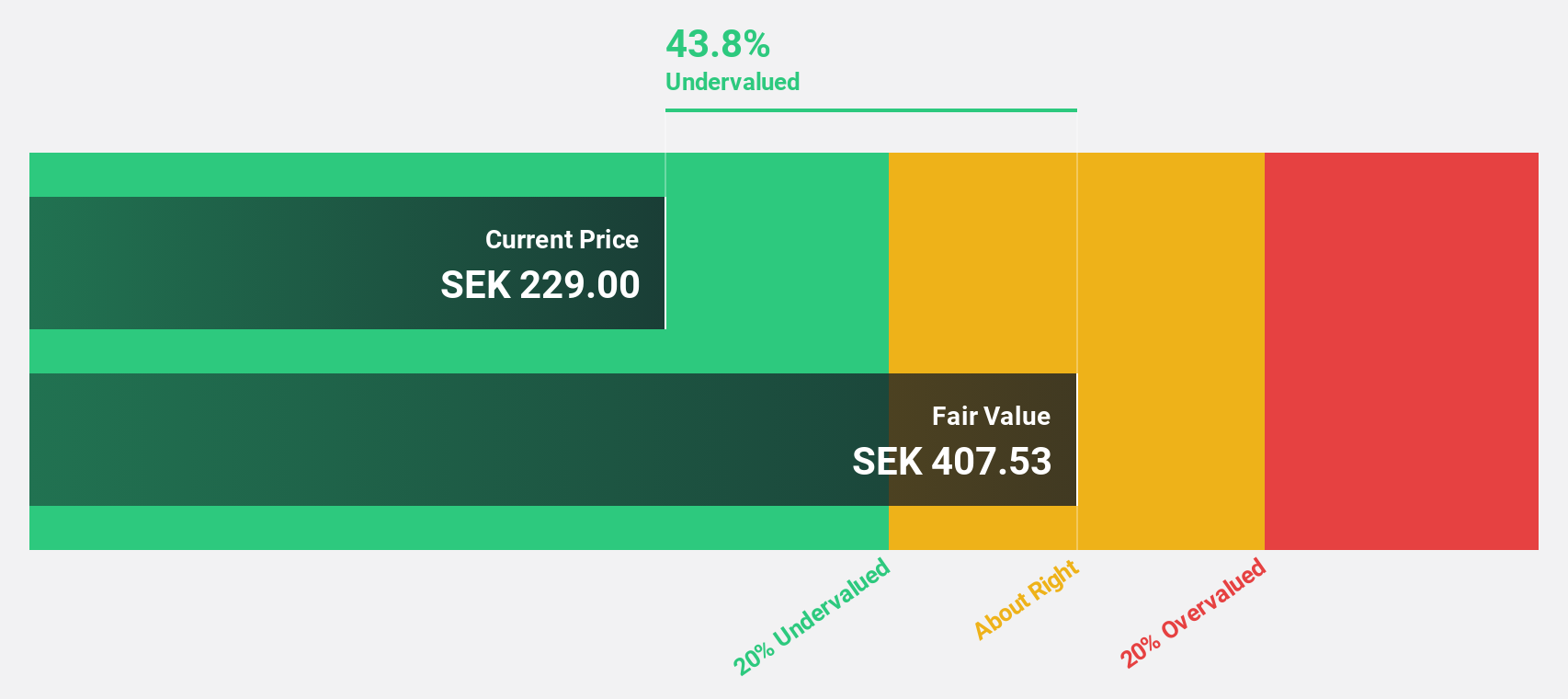

Estimated Discount To Fair Value: 45.7%

Concentric AB, trading at SEK221, is significantly undervalued with a fair value estimate of SEK406.67 based on discounted cash flow analysis. Despite recent earnings declines, the company's forecasted annual profit growth of 24.4% and revenue growth of 3.3% outpace the Swedish market averages. The proposed acquisition by A.P. Møller Holding for SEK8.6 billion could further unlock value for shareholders if regulatory approvals are met by October 16, 2024.

- Our earnings growth report unveils the potential for significant increases in Concentric's future results.

- Click here and access our complete balance sheet health report to understand the dynamics of Concentric.

Husqvarna (OM:HUSQ B)

Overview: Husqvarna AB (publ) produces and sells outdoor power products, watering products, and lawn care power equipment, with a market cap of SEK40.68 billion.

Operations: Husqvarna's revenue segments include Gardena (SEK12.59 billion), Group Common (SEK157 million), Husqvarna Construction (SEK8.14 billion), and Husqvarna Forest & Garden (SEK28.37 billion).

Estimated Discount To Fair Value: 43.5%

Husqvarna AB, trading at SEK71.28, is significantly undervalued with a fair value estimate of SEK126.14 based on discounted cash flow analysis. Despite challenging market conditions and a forecasted 5% decline in third-quarter organic sales, earnings are expected to grow 26.35% annually over the next three years, outpacing the Swedish market's growth rate of 15.1%. However, high debt levels and low forecasted return on equity (12.2%) remain concerns for investors.

- According our earnings growth report, there's an indication that Husqvarna might be ready to expand.

- Dive into the specifics of Husqvarna here with our thorough financial health report.

Seize The Opportunity

- Get an in-depth perspective on all 42 Undervalued Swedish Stocks Based On Cash Flows by using our screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:COIC

Concentric

Designs, develops, manufactures, and distributes hydraulic and engine solutions in Sweden and internationally.

Excellent balance sheet, good value and pays a dividend.