Advertisement

- Sweden

- /

- Personal Products

- /

- OM:HUMBLE

3 Growth Companies With High Insider Ownership Expecting Up To 66% Earnings Growth

Simply Wall St

Reviewed by Simply Wall St

In a week marked by heightened economic activity and cautious earnings reports, global markets saw mixed performances, with major indices like the Nasdaq Composite and S&P MidCap 400 reaching new highs before retreating. Amid this backdrop of fluctuating market conditions, growth companies with high insider ownership can offer unique opportunities for investors seeking to align with firms where management has significant skin in the game.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 21.1% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Laopu Gold (SEHK:6181) | 36.4% | 33% |

| Alkami Technology (NasdaqGS:ALKT) | 11.2% | 98.6% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

We'll examine a selection from our screener results.

Esker (ENXTPA:ALESK)

Simply Wall St Growth Rating: ★★★★☆☆

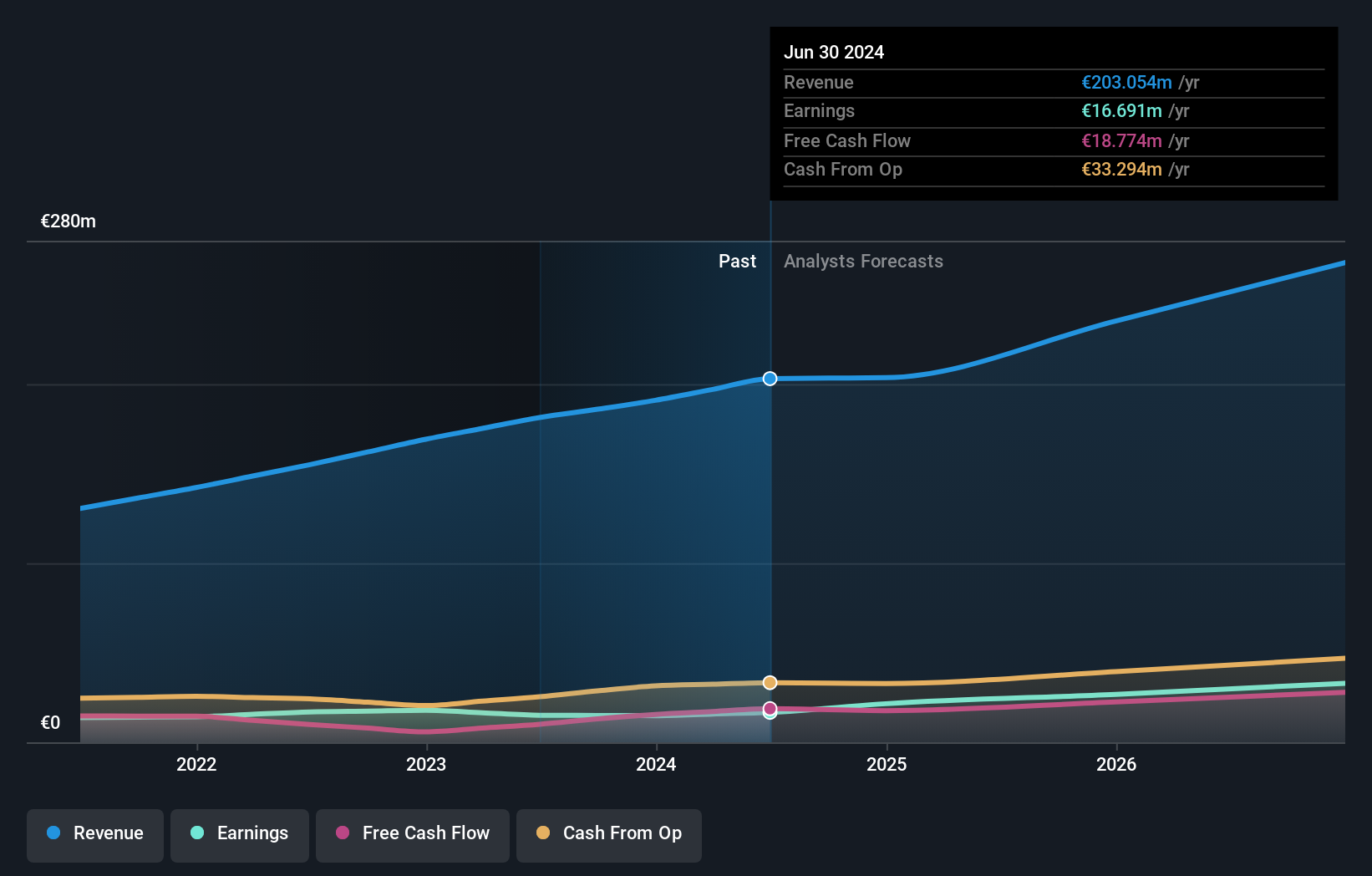

Overview: Esker SA operates a cloud platform designed for finance and customer service professionals both in France and internationally, with a market cap of approximately €1.54 billion.

Operations: The company's revenue is primarily derived from its Software & Programming segment, totaling €203.05 million.

Insider Ownership: 11.1%

Earnings Growth Forecast: 26.7% p.a.

Esker has demonstrated strong growth potential with a 17% increase in third-quarter sales revenue, reaching €51 million. The company's earnings are forecast to grow at 26.7% annually, outpacing the French market's average of 12.3%. Despite slower revenue growth projections at 11.8%, Esker's insider ownership remains significant, evidenced by recent acquisition interest from General Atlantic and Bridgepoint Group for €1.58 billion, highlighting confidence in its strategic direction and future prospects.

- Get an in-depth perspective on Esker's performance by reading our analyst estimates report here.

- Our valuation report unveils the possibility Esker's shares may be trading at a premium.

Humble Group (OM:HUMBLE)

Simply Wall St Growth Rating: ★★★★☆☆

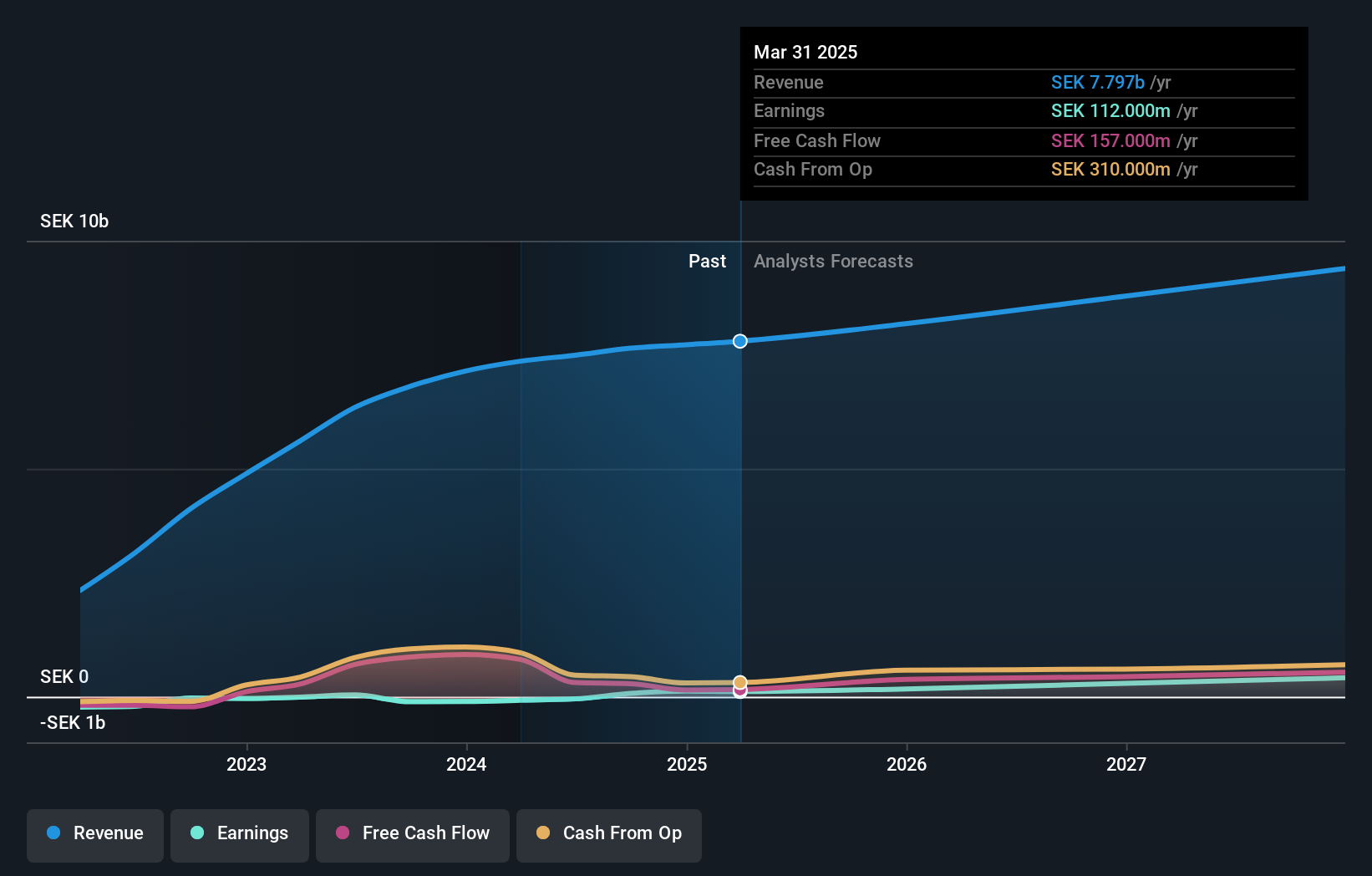

Overview: Humble Group AB (publ) refines, develops, and distributes fast-moving consumer products in Sweden and internationally, with a market cap of SEK5.40 billion.

Operations: The company's revenue is derived from four main segments: Future Snacking (SEK959 million), Sustainable Care (SEK2.34 billion), Quality Nutrition (SEK1.58 billion), and Nordic Distribution (SEK2.74 billion).

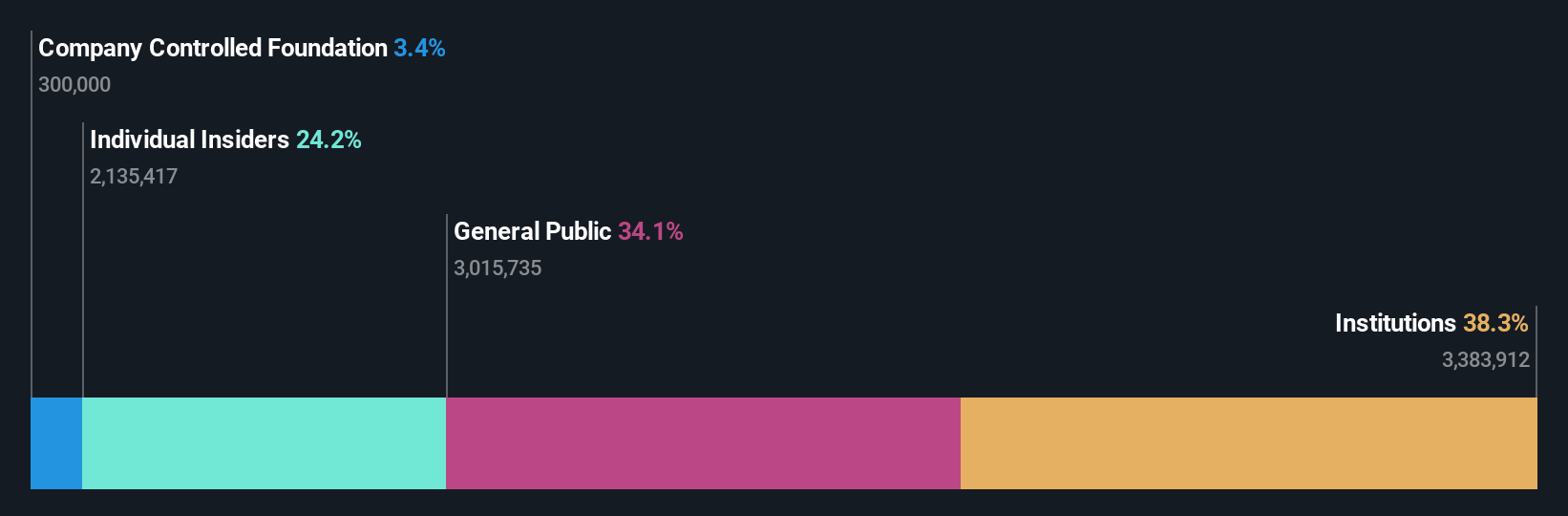

Insider Ownership: 15.8%

Earnings Growth Forecast: 66.7% p.a.

Humble Group's recent performance highlights its growth trajectory, reporting a net income of SEK 27 million in Q3 2024 compared to a loss last year. With earnings forecasted to grow at 66.7% annually, significantly outpacing the Swedish market, the company shows strong growth potential. Insider confidence is evident with substantial insider buying over the past three months. Despite trading below estimated fair value and slower revenue growth projections, Humble's strategic direction appears promising with its inclusion in the OMX Nordic All-Share Index.

- Click here to discover the nuances of Humble Group with our detailed analytical future growth report.

- According our valuation report, there's an indication that Humble Group's share price might be on the expensive side.

Enplas (TSE:6961)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Enplas Corporation is a company that manufactures and sells semiconductor, automobile parts, optical communication devices, and life science products both in Japan and internationally, with a market cap of ¥52.44 billion.

Operations: The company's revenue segments include semiconductor products at ¥10.45 billion, automobile parts at ¥8.32 billion, optical communication devices at ¥5.67 billion, and life science related products at ¥3.21 billion.

Insider Ownership: 24.2%

Earnings Growth Forecast: 24.5% p.a.

Enplas demonstrates strong growth potential with earnings projected to grow 24.47% annually, surpassing the Japanese market's average. Despite a volatile share price recently, it trades at 56.6% below its estimated fair value, suggesting potential undervaluation. Revenue growth is expected at 9.8%, outpacing the broader market but not reaching high-growth benchmarks. Recent insider trading activity is limited, providing no substantial insights into insider sentiment over the past three months.

- Delve into the full analysis future growth report here for a deeper understanding of Enplas.

- Our valuation report unveils the possibility Enplas' shares may be trading at a discount.

Summing It All Up

- Reveal the 1538 hidden gems among our Fast Growing Companies With High Insider Ownership screener with a single click here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Humble Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:HUMBLE

Humble Group

Develops, refines, and distributes fast-moving consumer products in Sweden and internationally.

Reasonable growth potential and fair value.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.6% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.5% undervalued

AG

Community Contributor