Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Bactiguard Holding AB (publ) (STO:BACTI B) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Bactiguard Holding

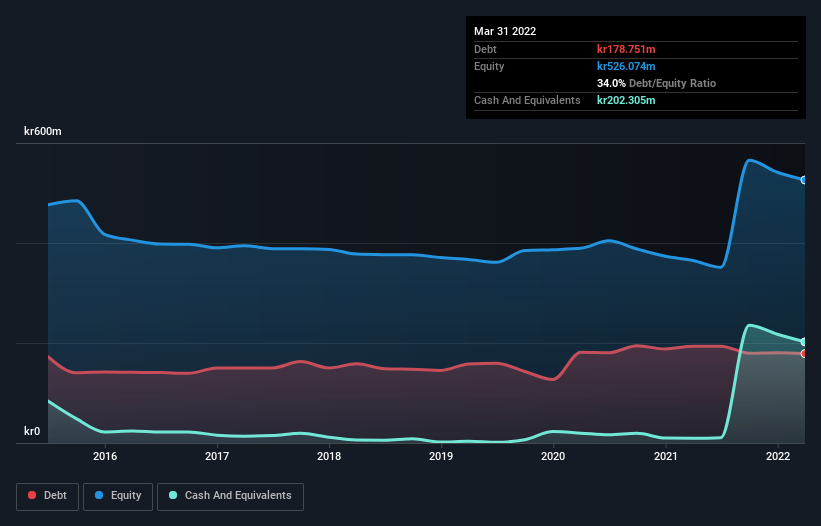

How Much Debt Does Bactiguard Holding Carry?

As you can see below, Bactiguard Holding had kr178.8m of debt at March 2022, down from kr193.6m a year prior. However, it does have kr202.3m in cash offsetting this, leading to net cash of kr23.6m.

How Strong Is Bactiguard Holding's Balance Sheet?

The latest balance sheet data shows that Bactiguard Holding had liabilities of kr75.0m due within a year, and liabilities of kr239.7m falling due after that. Offsetting this, it had kr202.3m in cash and kr78.3m in receivables that were due within 12 months. So its liabilities total kr34.1m more than the combination of its cash and short-term receivables.

This state of affairs indicates that Bactiguard Holding's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the kr3.57b company is short on cash, but still worth keeping an eye on the balance sheet. While it does have liabilities worth noting, Bactiguard Holding also has more cash than debt, so we're pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Bactiguard Holding will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Bactiguard Holding wasn't profitable at an EBIT level, but managed to grow its revenue by 11%, to kr189m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is Bactiguard Holding?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Bactiguard Holding lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through kr8.3m of cash and made a loss of kr65m. With only kr23.6m on the balance sheet, it would appear that its going to need to raise capital again soon. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 3 warning signs for Bactiguard Holding (1 is potentially serious) you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Bactiguard Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:BACTI B

Bactiguard Holding

A medTech company, provides infection prevention technology and solutions in orthopedics, cardiology, neurology, urology, and vascular access areas in the United States, Sweden, Malaysia, India, Bangladesh, Indonesia, the Kingdom of Saudi Arabia, and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor