Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, EQL Pharma AB (publ) (NGM:EQL) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for EQL Pharma

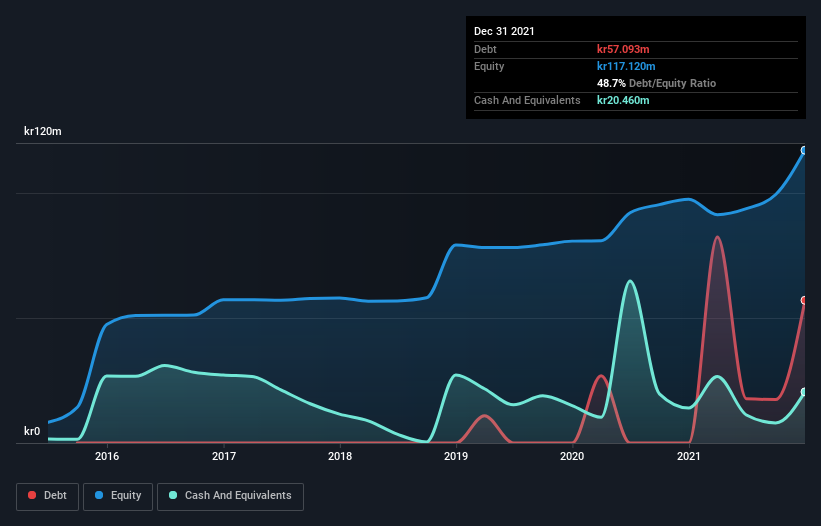

What Is EQL Pharma's Net Debt?

As you can see below, at the end of December 2021, EQL Pharma had kr57.1m of debt, up from none a year ago. Click the image for more detail. However, because it has a cash reserve of kr20.5m, its net debt is less, at about kr36.6m.

How Strong Is EQL Pharma's Balance Sheet?

According to the last reported balance sheet, EQL Pharma had liabilities of kr224.6m due within 12 months, and liabilities of kr13.4m due beyond 12 months. Offsetting these obligations, it had cash of kr20.5m as well as receivables valued at kr95.1m due within 12 months. So its liabilities total kr122.4m more than the combination of its cash and short-term receivables.

Given EQL Pharma has a market capitalization of kr828.3m, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

EQL Pharma's net debt is only 0.94 times its EBITDA. And its EBIT covers its interest expense a whopping 14.9 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. On top of that, EQL Pharma grew its EBIT by 68% over the last twelve months, and that growth will make it easier to handle its debt. There's no doubt that we learn most about debt from the balance sheet. But it is EQL Pharma's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, EQL Pharma saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Happily, EQL Pharma's impressive interest cover implies it has the upper hand on its debt. But the stark truth is that we are concerned by its conversion of EBIT to free cash flow. It's also worth noting that EQL Pharma is in the Healthcare industry, which is often considered to be quite defensive. All these things considered, it appears that EQL Pharma can comfortably handle its current debt levels. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it's worth monitoring the balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example EQL Pharma has 3 warning signs (and 1 which can't be ignored) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if EQL Pharma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:EQL

EQL Pharma

Engages in the development, marketing, and sale of generic medicines to pharmacies and hospitals in Sweden, Denmark, Norway, Finland, and the rest of Europe.

Exceptional growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.6% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|14.8% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.9% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$206.17|20.5% undervalued

AN

Based on Analyst Price Targets