Advertisement

- Sweden

- /

- Hospitality

- /

- OM:EVO

Evolution (OM:EVO) Margin Compression Challenges Bullish Narratives Despite FY 2025 Profit Scale

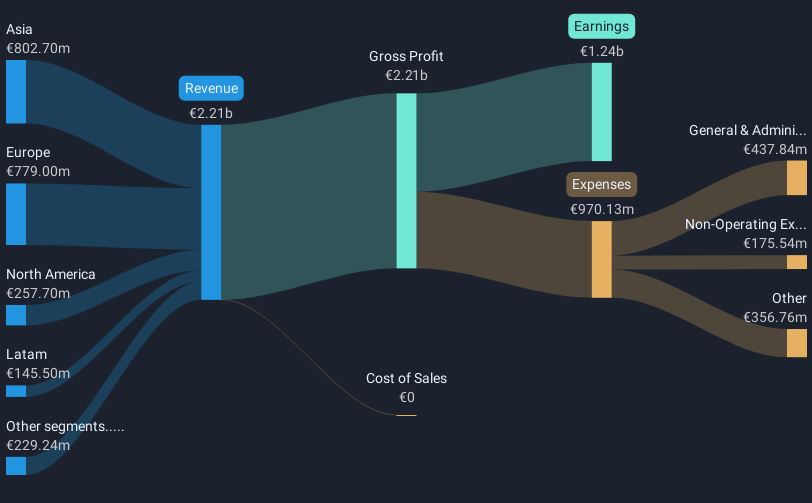

Evolution (OM:EVO) has wrapped up FY 2025 with fourth quarter revenue of €514.2 million and basic EPS of €1.54, set against a trailing twelve month EPS of €5.24 on revenue of about €2.1 billion. Over recent quarters in 2025, the company has seen revenue move between €507.1 million and €524.3 million, while quarterly EPS ranged from €1.22 to €1.54. This gives investors a clearer view of how headline growth is feeding into earnings. With a trailing net profit margin of 51.4% compared to 60.3% a year earlier, the focus this season is on how much profitability the business is keeping as it scales.

See our full analysis for Evolution.With the numbers on the table, the next step is to see how they line up against the major narratives around Evolution, highlighting where the current earnings support the story and where expectations may need a rethink.

Curious how numbers become stories that shape markets? Explore Community Narratives

51.4% margin now vs 60.3% before

- On a trailing basis, Evolution converted €2.1b of revenue into €1.1b of net income, which works out to a 51.4% net profit margin compared with 60.3% a year earlier, so a smaller share of sales is turning into profit than before.

- What stands out for the bullish view is that a 51.4% margin sits alongside trailing twelve month EPS of €5.24 and net income of €1.1b, yet the recent year is described as having negative earnings growth versus the prior five year pace of 20.8% per year, which means:

- Supporters pointing to historically strong growth now have to explain why the latest twelve month margin is lower than the earlier 60.3% level.

- The mix of high absolute profitability and weaker recent growth creates a test for any bullish claim that past growth trends still fully reflect the current earnings power.

EPS trend flattens after strong five years

- Quarterly basic EPS in 2025 moved in a relatively tight band between €1.22 and €1.54, while trailing twelve month EPS stepped down from €5.94 in late 2024 to €5.24 by Q4 2025, which aligns with the comment that earnings growth over the last year turned negative compared with 20.8% per year over five years.

- Critics focused on a bearish angle highlight that earnings growth is now forecast at about 3.5% per year, below the Swedish market forecast of 9.5%, and the recent EPS pattern gives them concrete backing because:

- The move from €5.94 to €5.24 in trailing EPS fits with the idea that growth has cooled relative to the earlier multi year trend.

- With revenue forecast at 5.7% per year and earnings at 3.5%, bears can point to a gap between top line and bottom line growth that aligns with the reported margin compression.

P/E 9.9x and 5.33% yield vs DCF fair value

- The shares trade on a P/E of 9.9x against an industry level of 17.8x and peer average of 21.6x. The current price of SEK559.60 sits well below the stated DCF fair value of SEK1,652.01 and comes with a trailing dividend yield of 5.33%.

- Supporters taking a bullish stance see this as a powerful valuation and income combo, yet the recent earnings slowdown adds an extra layer to that story because:

- The apparent 66.1% discount to the DCF fair value and the 5.33% dividend yield are being offered at a time when trailing profit margins have moved from 60.3% to 51.4%.

- That tension between a low 9.9x P/E and softer recent earnings growth is exactly what investors have to weigh when deciding how much weight to give the DCF fair value figure of SEK1,652.01.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Evolution's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Evolution now has a cooler earnings profile, with margins at 51.4% versus 60.3% before and trailing EPS moving from €5.94 to €5.24.

If that mix of softer earnings momentum and a low 9.9x P/E makes you pause, use our 239 high quality undervalued stocks to hunt for other ideas that currently look mispriced.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Evolution might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:EVO

Evolution

Develops, produces, markets, and licenses live casino and slots solutions to gaming operators in Europe, Asia, North America, Latin America, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0774.4% undervalued

217 followersusers have followed this narrative

1 commentusers have commented on this narrative

31 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.4% undervalued

55 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0716.3% undervalued

14 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3812.7% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

Recently Updated Narratives

53

537578 on Recursion Pharmaceuticals ·

Recursion Pharmaceuticals! WTH is going on?

Fair Value:US$1.9766.5% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Visa ·

Visa and the Case for Patience in Premium Businesses

Fair Value:US$2808.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EV

evadav on SSE ·

Future Prosperity Awaits with SSE's Impressive 11% Revenue Growth

Fair Value:UK£31.7613.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3956.1% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3136.9% undervalued

1351 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

37 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative

Trending Discussion

EL

Element1 on Greatland Resources ·

I can’t believe how inaccurate and out of date this site is—and people rely on it. Greatland owns tw...

0

|0

MI

Mikeymike on Auxly Cannabis Group ·

Id like to understand why they believe the profit margin is going decline so dramatically. Is it ene...

0

|0