- Sweden

- /

- Professional Services

- /

- OM:WISE

Does Wise Group AB (publ)'s (STO:WISE) Recent Track Record Look Strong?

When Wise Group AB (publ) (STO:WISE) released its most recent earnings update (31 December 2018), I compared it against two factor: its historical earnings track record, and the performance of its industry peers on average. Being able to interpret how well Wise Group has done so far requires weighing its performance against a benchmark, rather than looking at a standalone number at a point in time. In this article, I've summarized the key takeaways on how I see WISE has performed.

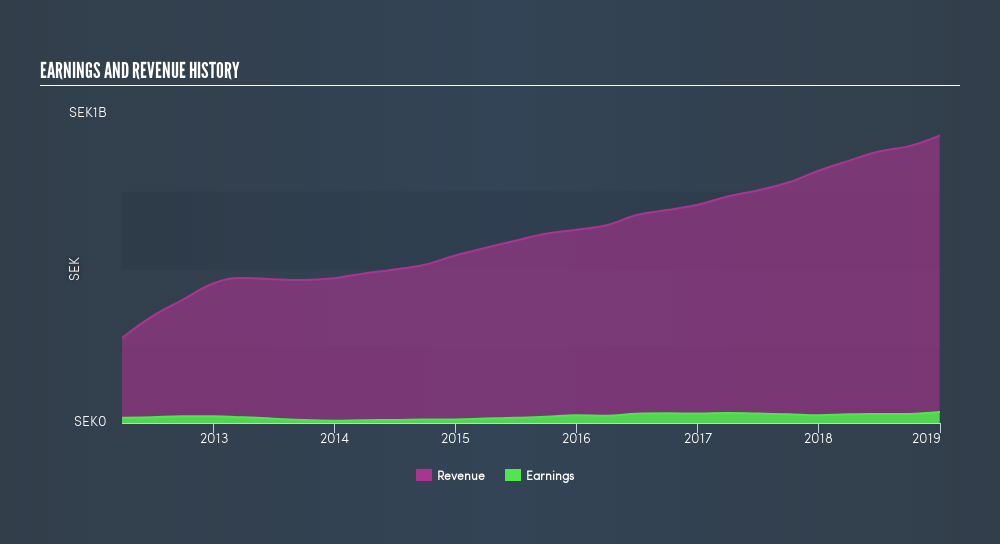

View our latest analysis for Wise Group

How Well Did WISE Perform?

WISE's trailing twelve-month earnings (from 31 December 2018) of kr35m has jumped 41% compared to the previous year.

Furthermore, this one-year growth rate has exceeded its 5-year annual growth average of 23%, indicating the rate at which WISE is growing has accelerated. What's enabled this growth? Let's take a look at if it is only due to an industry uplift, or if Wise Group has experienced some company-specific growth.

In terms of returns from investment, Wise Group has invested its equity funds well leading to a 27% return on equity (ROE), above the sensible minimum of 20%. Furthermore, its return on assets (ROA) of 10% exceeds the SE Professional Services industry of 7.2%, indicating Wise Group has used its assets more efficiently. And finally, its return on capital (ROC), which also accounts for Wise Group’s debt level, has increased over the past 3 years from 27% to 30%.

What does this mean?

Though Wise Group's past data is helpful, it is only one aspect of my investment thesis. Companies that have performed well in the past, such as Wise Group gives investors conviction. However, the next step would be to assess whether the future looks as optimistic. I recommend you continue to research Wise Group to get a better picture of the stock by looking at:

- Future Outlook: What are well-informed industry analysts predicting for WISE’s future growth? Take a look at our free research report of analyst consensus for WISE’s outlook.

- Financial Health: Are WISE’s operations financially sustainable? Balance sheets can be hard to analyze, which is why we’ve done it for you. Check out our financial health checks here.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 31 December 2018. This may not be consistent with full year annual report figures.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About OM:WISE

Wise Group

Engages in the provision of recruitment and consultancy services in Sweden, Finland, and Denmark.

Flawless balance sheet and slightly overvalued.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion