- Sweden

- /

- Construction

- /

- OM:NCC B

Is It Smart To Buy NCC AB (publ) (STO:NCC B) Before It Goes Ex-Dividend?

It looks like NCC AB (publ) (STO:NCC B) is about to go ex-dividend in the next three days. The ex-dividend date generally occurs two days before the record date, which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade can take two business days or more to settle. Therefore, if you purchase NCC's shares on or after the 8th of May, you won't be eligible to receive the dividend, when it is paid on the 14th of May.

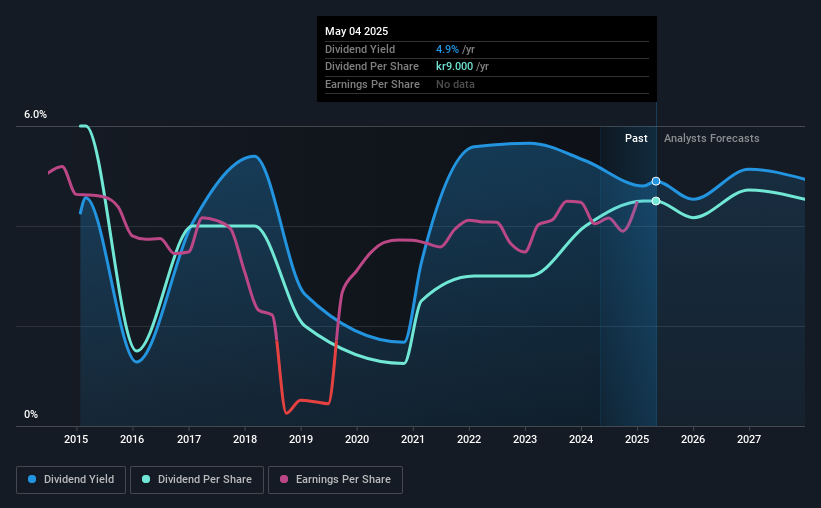

The company's upcoming dividend is kr06.50 a share, following on from the last 12 months, when the company distributed a total of kr9.00 per share to shareholders. Looking at the last 12 months of distributions, NCC has a trailing yield of approximately 4.9% on its current stock price of kr0183.80. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to check whether the dividend payments are covered, and if earnings are growing.

We've discovered 1 warning sign about NCC. View them for free.Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. NCC paid out 56% of its earnings to investors last year, a normal payout level for most businesses. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. The good news is it paid out just 20% of its free cash flow in the last year.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Check out our latest analysis for NCC

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings fall far enough, the company could be forced to cut its dividend. For this reason, we're glad to see NCC's earnings per share have risen 15% per annum over the last five years. NCC has an average payout ratio which suggests a balance between growing earnings and rewarding shareholders. Given the quick rate of earnings per share growth and current level of payout, there may be a chance of further dividend increases in the future.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. NCC's dividend payments per share have declined at 2.8% per year on average over the past 10 years, which is uninspiring. NCC is a rare case where dividends have been decreasing at the same time as earnings per share have been improving. It's unusual to see, and could point to unstable conditions in the core business, or more rarely an intensified focus on reinvesting profits.

The Bottom Line

Should investors buy NCC for the upcoming dividend? NCC's growing earnings per share and conservative payout ratios make for a decent combination. We also like that it paid out a lower percentage of its cash flow. NCC looks solid on this analysis overall, and we'd definitely consider investigating it more closely.

In light of that, while NCC has an appealing dividend, it's worth knowing the risks involved with this stock. Case in point: We've spotted 1 warning sign for NCC you should be aware of.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

If you're looking to trade NCC, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if NCC might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:NCC B

NCC

Operates as a construction company in Sweden, Norway, Denmark, and Finland.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Community Narratives