Advertisement

- Sweden

- /

- Industrials

- /

- OM:LIFCO B

Does Lifco’s (OM:LIFCO B) Strong Q3 and Acquisitions Reinforce Its Long-Term Growth Outlook?

Simply Wall St

Reviewed by Sasha Jovanovic

- Lifco AB reported strong third-quarter 2025 results, with sales rising to SEK 6,842 million and net income increasing to SEK 892 million compared to the previous year.

- Management highlighted Lifco’s continued low net debt to EBITDA ratio of 1.3x and emphasized an ongoing commitment to acquisitions across Europe to support future development.

- We’ll assess how Lifco’s solid financial position and ongoing acquisition activity could influence its previously established growth outlook.

Outshine the giants: these 27 early-stage AI stocks could fund your retirement.

Lifco Investment Narrative Recap

To own Lifco, an investor should be comfortable with a model that pairs steady operational growth with disciplined, acquisition-driven expansion, even as margin pressures appear in some segments. The latest quarterly results reinforce Lifco’s strong financial footing and ongoing commitment to acquisitions, but do not materially impact the most immediate catalyst, the pace and sustainability of revenue growth in core areas, nor do they significantly address the biggest near-term risk, which is margin compression from lower-margin System Solutions trends.

The company’s recent report of increased third-quarter sales and net income, alongside continued acquisition activity, stands out as particularly relevant. While revenue continues to grow, segment mix and margin quality remain critical themes for investors to watch, as these have direct consequences on both short-term performance and the duration of earnings momentum.

By contrast, investors should remain mindful of how further growth in lower-margin segments could affect overall profitability if not carefully balanced by acquisitions that enhance...

Read the full narrative on Lifco (it's free!)

Lifco's outlook projects SEK34.7 billion in revenue and SEK4.4 billion in earnings by 2028. This is based on an annual revenue growth rate of 8.4% and a SEK1.0 billion increase in earnings from the current level of SEK3.4 billion.

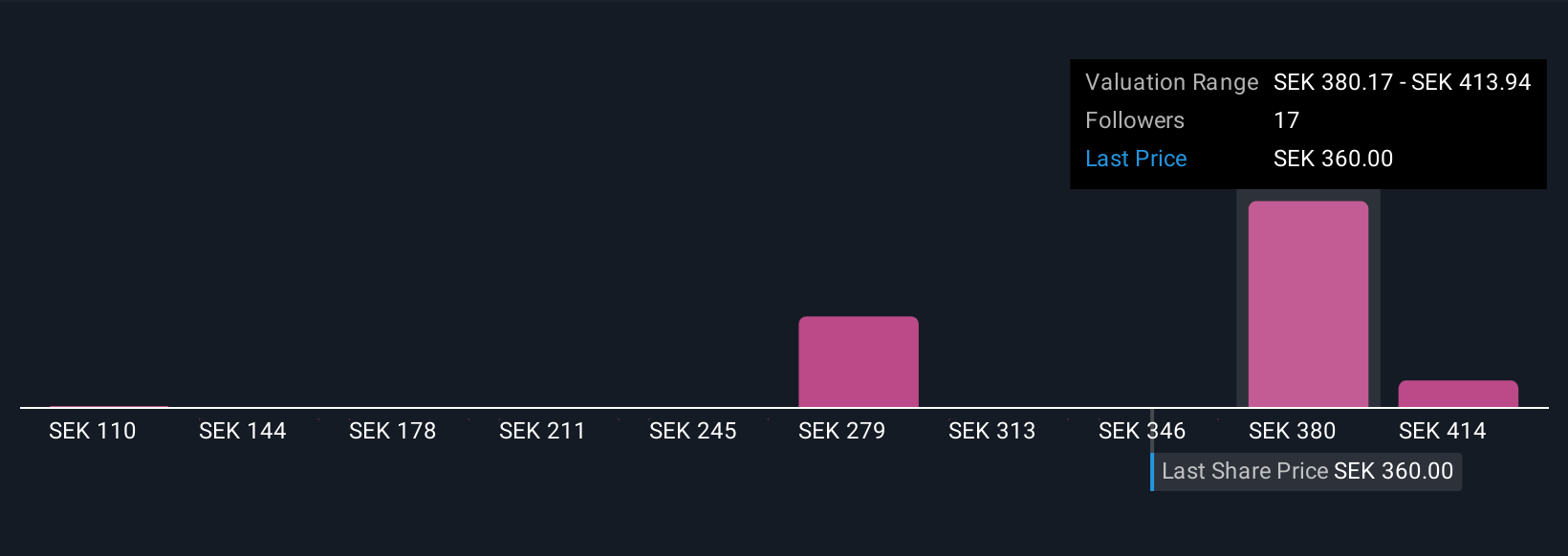

Uncover how Lifco's forecasts yield a SEK383.67 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Seven individual fair value estimates from the Simply Wall St Community range widely, from SEK110 to SEK447.71 per share. While many plural views exist, margin pressure within System Solutions may ultimately constrain Lifco’s financial upside, highlighting the importance of multiple perspectives on likely outcomes.

Explore 7 other fair value estimates on Lifco - why the stock might be worth less than half the current price!

Build Your Own Lifco Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Lifco research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Lifco research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lifco's overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Rare earth metals are the new gold rush. Find out which 37 stocks are leading the charge.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:LIFCO B

Lifco

Engages in the dental, demolition and tools, and systems solutions businesses in Sweden, Norway, Germany, rest of Europe, the United Kingdom, Asia, Australia, Italy, North America, and internationally.

Acceptable track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor