Advertisement

Earnings Miss: Balco Group AB Missed EPS By 96% And Analysts Are Revising Their Forecasts

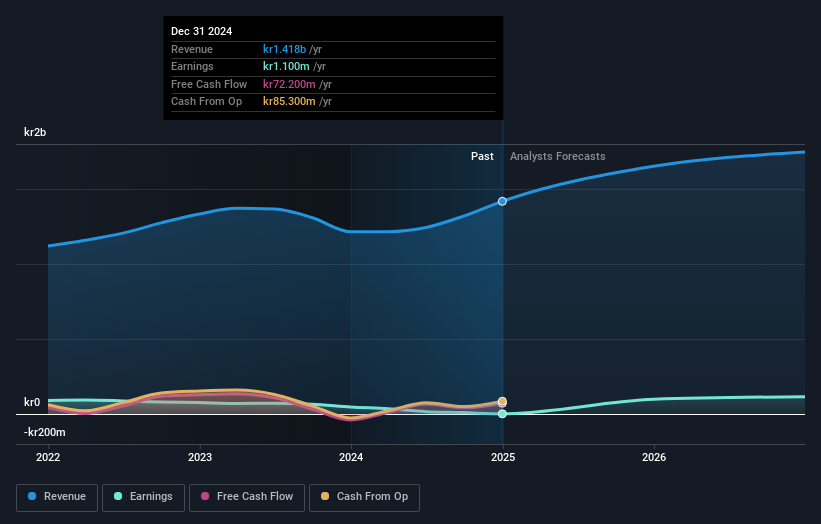

Balco Group AB (STO:BALCO) just released its latest yearly report and things are not looking great. Results showed a clear earnings miss, with kr1.4b revenue coming in 4.3% lower than what the analystexpected. Statutory earnings per share (EPS) of kr0.05 missed the mark badly, arriving some 96% below what was expected. The analyst typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analyst latest (statutory) post-earnings forecasts for next year.

See our latest analysis for Balco Group

After the latest results, the solitary analyst covering Balco Group are now predicting revenues of kr1.65b in 2025. If met, this would reflect a notable 16% improvement in revenue compared to the last 12 months. Per-share earnings are expected to soar 8,774% to kr4.24. Yet prior to the latest earnings, the analyst had been anticipated revenues of kr1.69b and earnings per share (EPS) of kr4.44 in 2025. It's pretty clear that pessimism has reared its head after the latest results, leading to a weaker revenue outlook and a minor downgrade to earnings per share estimates.

The average price target climbed 5.5% to kr58.00despite the reduced earnings forecasts, suggesting that this earnings impact could be a positive for the stock, once it passes.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Balco Group's past performance and to peers in the same industry. The analyst is definitely expecting Balco Group's growth to accelerate, with the forecast 16% annualised growth to the end of 2025 ranking favourably alongside historical growth of 2.2% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 5.8% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analyst also expect Balco Group to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analyst reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Balco Group. They also downgraded Balco Group's revenue estimates, but industry data suggests that it is expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analyst clearly feeling that the intrinsic value of the business is improving.

With that in mind, we wouldn't be too quick to come to a conclusion on Balco Group. Long-term earnings power is much more important than next year's profits. We have analyst estimates for Balco Group going out as far as 2026, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 2 warning signs for Balco Group that you should be aware of.

Valuation is complex, but we're here to simplify it.

Discover if Balco Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:BALCO

Balco Group

Engages in developing, manufacturing, selling, and installing balcony systems for tenant-owner associations, private landlords, municipal housing, architects, builders, and shipping companies.

Reasonable growth potential and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor