- Saudi Arabia

- /

- Real Estate

- /

- SASE:4324

Banan Real Estate Co.'s (TADAWUL:9519) Popularity With Investors Is Under Threat From Overpricing

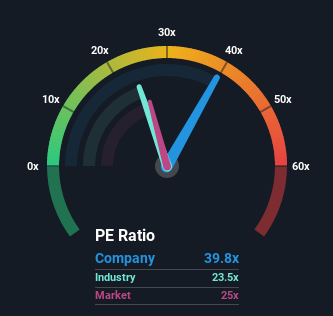

Banan Real Estate Co.'s (TADAWUL:9519) price-to-earnings (or "P/E") ratio of 39.8x might make it look like a strong sell right now compared to the market in Saudi Arabia, where around half of the companies have P/E ratios below 24x and even P/E's below 17x are quite common. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Banan Real Estate certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for Banan Real Estate

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Banan Real Estate's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 71% gain to the company's bottom line. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 99% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

In contrast to the company, the rest of the market is expected to grow by 14% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

In light of this, it's alarming that Banan Real Estate's P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

The Bottom Line On Banan Real Estate's P/E

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Banan Real Estate currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the high P/E lower. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for Banan Real Estate with six simple checks on some of these key factors.

If you're unsure about the strength of Banan Real Estate's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Banan Real Estate might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:4324

Banan Real Estate

Owns and leases residential and non-residential properties in Saudi Arabia.

Solid track record with adequate balance sheet.

Market Insights

Community Narratives