Advertisement

- China

- /

- Electrical

- /

- SHSE:688668

Uncovering Undiscovered Gems On None Exchange December 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape marked by rate cuts from the ECB and SNB, and with expectations for another Fed cut looming, small-cap stocks are feeling the pressure, evidenced by the Russell 2000's recent underperformance compared to larger indices. Despite this challenging environment, opportunities remain for discerning investors who can identify fundamentally strong companies with growth potential that may be overlooked in broader market trends.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| PSC | 17.90% | 2.07% | 13.38% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Thai Energy Storage Technology | 9.49% | -1.42% | 1.73% | ★★★★★☆ |

| National Investments Company K.S.C.P | 26.01% | 3.66% | 4.99% | ★★★★☆☆ |

| Al-Ahleia Insurance CompanyK.P | 8.09% | 10.04% | 16.85% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Jamuna Bank | 85.07% | 7.37% | -3.87% | ★★★★☆☆ |

| Al-Deera Holding Company K.P.S.C | 6.11% | 51.44% | 59.77% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

Riyadh Cement (SASE:3092)

Simply Wall St Value Rating: ★★★★★★

Overview: Riyadh Cement Company engages in the production and sale of cement across several Middle Eastern countries, including Saudi Arabia, Bahrain, Jordan, Kuwait, Qatar, and Oman, with a market capitalization of SAR4.06 billion.

Operations: Riyadh Cement generates revenue primarily from cement manufacturing, amounting to SAR727.03 million. The company's financial performance can be assessed through its net profit margin trends over recent periods, reflecting its profitability efficiency.

Riyadh Cement stands out with impressive earnings growth of 37% over the past year, surpassing the Basic Materials industry's 12.1%. The company reported a net income of SAR 94.58 million for Q3 2024, a significant jump from SAR 18.71 million in the previous year, reflecting its robust performance. Trading at a price-to-earnings ratio of 14.9x, it offers good value compared to the SA market's average of 23.7x. Riyadh Cement is debt-free and has been added to both the S&P Global BMI Index and S&P Pan Arab Composite, underscoring its growing industry presence and potential for future growth despite forecasts suggesting an earnings decline by an average of 6.9% annually over three years.

- Click here and access our complete health analysis report to understand the dynamics of Riyadh Cement.

Assess Riyadh Cement's past performance with our detailed historical performance reports.

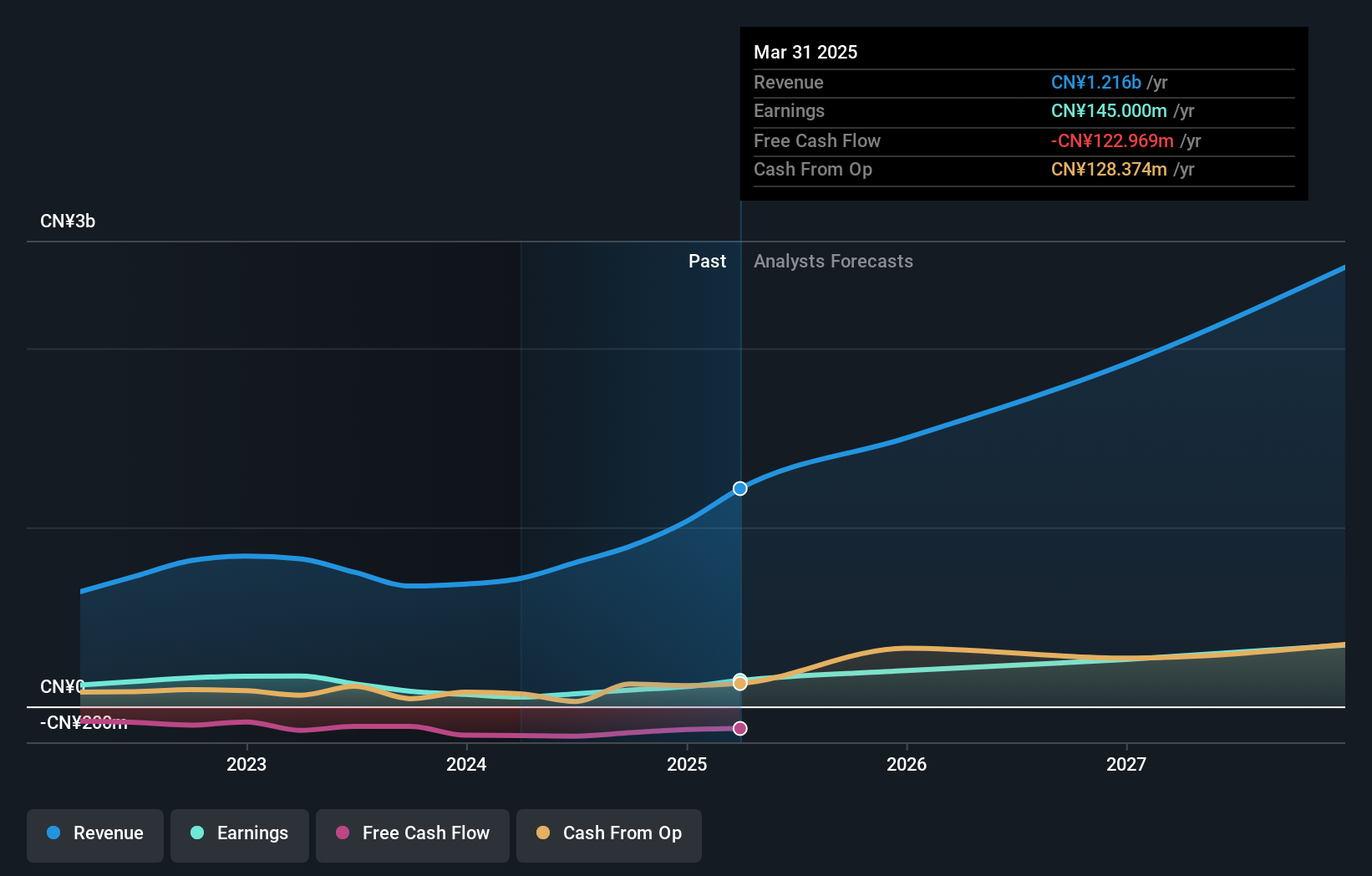

Dongguan Dingtong Precision Metal (SHSE:688668)

Simply Wall St Value Rating: ★★★★★★

Overview: Dongguan Dingtong Precision Metal Co., Ltd. operates in the precision metal industry and has a market capitalization of CN¥5.34 billion.

Operations: Dingtong Precision Metal generates revenue primarily through its precision metal products. The company's net profit margin is a key financial metric, reflecting its profitability efficiency.

Dongguan Dingtong Precision Metal has been making waves with a notable 8% earnings growth over the past year, outpacing the electrical industry’s modest 1.1% rise. The company is debt-free, which suggests financial stability and no concerns about interest payments. Over the last nine months, sales jumped to CNY 703 million from CNY 491 million, while net income rose to CNY 78 million from CNY 53 million previously. Earnings per share climbed to CNY 0.57 from CNY 0.39 a year ago, indicating robust performance despite recent share price volatility in the market.

- Take a closer look at Dongguan Dingtong Precision Metal's potential here in our health report.

Understand Dongguan Dingtong Precision Metal's track record by examining our Past report.

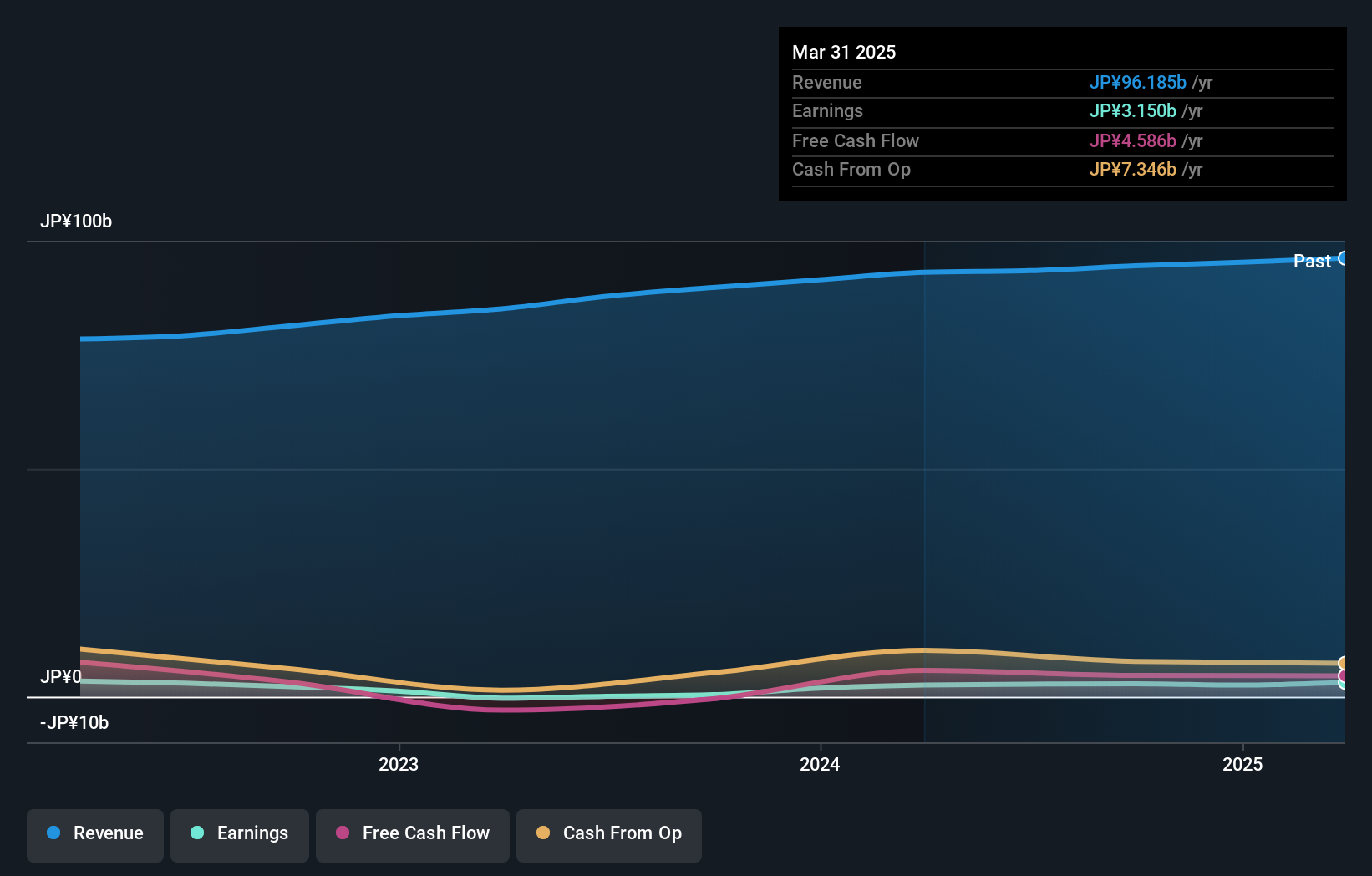

Mos Food Services (TSE:8153)

Simply Wall St Value Rating: ★★★★★☆

Overview: Mos Food Services, Inc. operates the MOS BURGER hamburger franchise and other restaurant businesses both in Japan and internationally, with a market cap of ¥117.86 billion.

Operations: Mos Food Services generates revenue primarily through its MOS BURGER franchise and other restaurant operations across Japan and internationally. The company's market cap stands at ¥117.86 billion, reflecting its significant presence in the food service industry.

Mos Food Services has been making waves with a remarkable earnings growth of 567% over the past year, significantly outpacing the Hospitality industry's 24.5%. Despite a slight uptick in its debt to equity ratio from 5.2% to 5.5% over five years, it holds more cash than total debt, suggesting financial stability is not an issue. The company also enjoys high-quality earnings and maintains positive free cash flow, indicating robust operational efficiency. Looking ahead, earnings are projected to grow by about 5% annually, hinting at continued potential for steady expansion in its niche market segment.

Make It Happen

- Explore the 4621 names from our Undiscovered Gems With Strong Fundamentals screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688668

Dongguan Dingtong Precision Metal

Dongguan Dingtong Precision Metal Co., Ltd.

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor