- Saudi Arabia

- /

- Basic Materials

- /

- SASE:3060

Can Yanbu Cement Company's (TADAWUL:3060) Weak Financials Pull The Plug On The Stock's Current Momentum On Its Share Price?

Most readers would already be aware that Yanbu Cement's (TADAWUL:3060) stock increased significantly by 32% over the past three months. However, in this article, we decided to focus on its weak fundamentals, as long-term financial performance of a business is what ultimatley dictates market outcomes. In this article, we decided to focus on Yanbu Cement's ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

View our latest analysis for Yanbu Cement

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Yanbu Cement is:

9.4% = ر.س295m ÷ ر.س3.2b (Based on the trailing twelve months to September 2020).

The 'return' is the yearly profit. Another way to think of that is that for every SAR1 worth of equity, the company was able to earn SAR0.09 in profit.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Yanbu Cement's Earnings Growth And 9.4% ROE

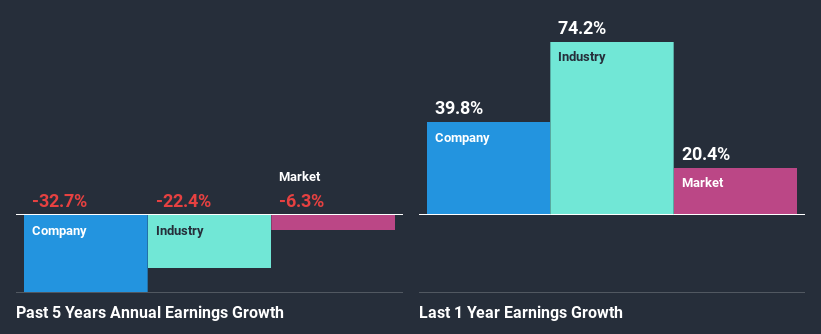

It is quite clear that Yanbu Cement's ROE is rather low. Further, we noted that the company's ROE is similar to the industry average of 9.1%. Given the circumstances, the significant decline in net income by 33% seen by Yanbu Cement over the last five years is not surprising.

As a next step, we compared Yanbu Cement's performance with the industry and found thatYanbu Cement's performance is depressing even when compared with the industry, which has shrunk its earnings at a rate of 22% in the same period, which is a slower than the company.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Yanbu Cement is trading on a high P/E or a low P/E, relative to its industry.

Is Yanbu Cement Using Its Retained Earnings Effectively?

Yanbu Cement's high three-year median payout ratio of 127% suggests that the company is depleting its resources to keep up its dividend payments, and this shows in its shrinking earnings. Its usually very hard to sustain dividend payments that are higher than reported profits. You can see the 2 risks we have identified for Yanbu Cement by visiting our risks dashboard for free on our platform here.

Additionally, Yanbu Cement has paid dividends over a period of eight years, which means that the company's management is rather focused on keeping up its dividend payments, regardless of the shrinking earnings. Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 87% over the next three years. Regardless, the ROE is not expected to change much for the company despite the lower expected payout ratio.

Conclusion

On the whole, Yanbu Cement's performance is quite a big let-down. Particularly, its ROE is a huge disappointment, not to mention its lack of proper reinvestment into the business. As a result its earnings growth has also been quite disappointing. With that said, we studied the latest analyst forecasts and found that while the company has shrunk its earnings in the past, analysts expect its earnings to grow in the future. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

If you decide to trade Yanbu Cement, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SASE:3060

Yanbu Cement

Engages in manufacturing, producing, and trading of cement and related products in the Kingdom of Saudi Arabia and internationally.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Community Narratives