Advertisement

- Saudi Arabia

- /

- Chemicals

- /

- SASE:2330

These Analysts Just Made A Notable Downgrade To Their Advanced Petrochemical Company (TADAWUL:2330) EPS Forecasts

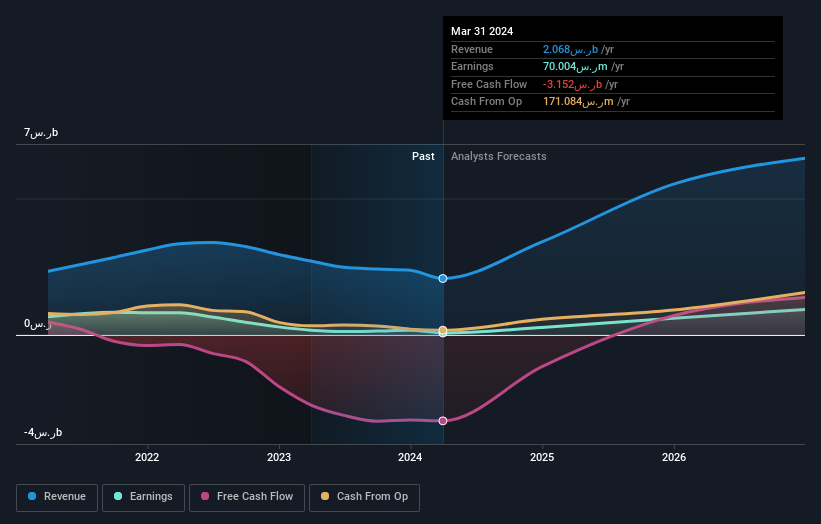

The analysts covering Advanced Petrochemical Company (TADAWUL:2330) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon.

Following the downgrade, the most recent consensus for Advanced Petrochemical from its seven analysts is for revenues of ر.س3.4b in 2024 which, if met, would be a major 65% increase on its sales over the past 12 months. Statutory earnings per share are presumed to surge 232% to ر.س0.90. Before this latest update, the analysts had been forecasting revenues of ر.س3.9b and earnings per share (EPS) of ر.س1.05 in 2024. It looks like analyst sentiment has declined substantially, with a measurable cut to revenue estimates and a considerable drop in earnings per share numbers as well.

View our latest analysis for Advanced Petrochemical

Analysts made no major changes to their price target of ر.س44.05, suggesting the downgrades are not expected to have a long-term impact on Advanced Petrochemical's valuation.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. For example, we noticed that Advanced Petrochemical's rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 95% growth to the end of 2024 on an annualised basis. That is well above its historical decline of 0.2% a year over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 5.8% annually. Not only are Advanced Petrochemical's revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Advanced Petrochemical. While analysts did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. We're also surprised to see that the price target went unchanged. Still, deteriorating business conditions (assuming accurate forecasts!) can be a leading indicator for the stock price, so we wouldn't blame investors for being more cautious on Advanced Petrochemical after the downgrade.

After a downgrade like this, it's pretty clear that previous forecasts were too optimistic. What's more, we've spotted several possible issues with Advanced Petrochemical's business, like concerns around earnings quality. For more information, you can click here to discover this and the 1 other concern we've identified.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies backed by insiders.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:2330

Advanced Petrochemical

Engages in the production and sale of propylene, polypropylene, isopropyl alcohol, polysilicon, and polysilicon downstream products in the Kingdom of Saudi Arabia and internationally.

High growth potential average dividend payer.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets