- Saudi Arabia

- /

- Insurance

- /

- SASE:8210

Bupa Arabia for Cooperative Insurance Company's (TADAWUL:8210) P/E Still Appears To Be Reasonable

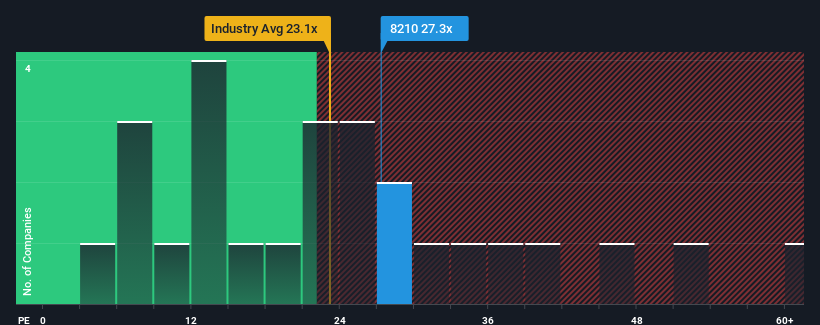

There wouldn't be many who think Bupa Arabia for Cooperative Insurance Company's (TADAWUL:8210) price-to-earnings (or "P/E") ratio of 27.3x is worth a mention when the median P/E in Saudi Arabia is similar at about 26x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Recent times haven't been advantageous for Bupa Arabia for Cooperative Insurance as its earnings have been rising slower than most other companies. It might be that many expect the uninspiring earnings performance to strengthen positively, which has kept the P/E from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

View our latest analysis for Bupa Arabia for Cooperative Insurance

How Is Bupa Arabia for Cooperative Insurance's Growth Trending?

There's an inherent assumption that a company should be matching the market for P/E ratios like Bupa Arabia for Cooperative Insurance's to be considered reasonable.

If we review the last year of earnings growth, the company posted a worthy increase of 7.2%. This was backed up an excellent period prior to see EPS up by 79% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 14% per annum as estimated by the four analysts watching the company. That's shaping up to be similar to the 16% per year growth forecast for the broader market.

With this information, we can see why Bupa Arabia for Cooperative Insurance is trading at a fairly similar P/E to the market. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Bottom Line On Bupa Arabia for Cooperative Insurance's P/E

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Bupa Arabia for Cooperative Insurance maintains its moderate P/E off the back of its forecast growth being in line with the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings won't throw up any surprises. Unless these conditions change, they will continue to support the share price at these levels.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Bupa Arabia for Cooperative Insurance, and understanding should be part of your investment process.

Of course, you might also be able to find a better stock than Bupa Arabia for Cooperative Insurance. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Bupa Arabia for Cooperative Insurance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:8210

Bupa Arabia for Cooperative Insurance

Engages in the insurance business in the Kingdom of Saudi Arabia.

Outstanding track record with excellent balance sheet and pays a dividend.

Market Insights

Community Narratives