Advertisement

- Saudi Arabia

- /

- Food and Staples Retail

- /

- SASE:4001

Capital Allocation Trends At Abdullah Al-Othaim Markets (TADAWUL:4001) Aren't Ideal

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Having said that, from a first glance at Abdullah Al-Othaim Markets (TADAWUL:4001) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Abdullah Al-Othaim Markets:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.13 = ر.س450m ÷ (ر.س6.0b - ر.س2.4b) (Based on the trailing twelve months to December 2023).

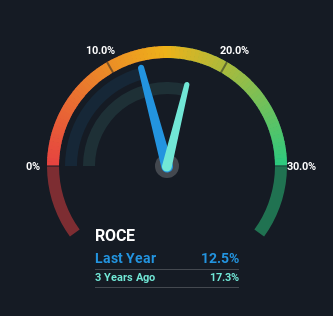

So, Abdullah Al-Othaim Markets has an ROCE of 13%. That's a pretty standard return and it's in line with the industry average of 13%.

View our latest analysis for Abdullah Al-Othaim Markets

Above you can see how the current ROCE for Abdullah Al-Othaim Markets compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for Abdullah Al-Othaim Markets .

What The Trend Of ROCE Can Tell Us

When we looked at the ROCE trend at Abdullah Al-Othaim Markets, we didn't gain much confidence. Over the last five years, returns on capital have decreased to 13% from 18% five years ago. Meanwhile, the business is utilizing more capital but this hasn't moved the needle much in terms of sales in the past 12 months, so this could reflect longer term investments. It's worth keeping an eye on the company's earnings from here on to see if these investments do end up contributing to the bottom line.

On a separate but related note, it's important to know that Abdullah Al-Othaim Markets has a current liabilities to total assets ratio of 41%, which we'd consider pretty high. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

The Bottom Line On Abdullah Al-Othaim Markets' ROCE

Bringing it all together, while we're somewhat encouraged by Abdullah Al-Othaim Markets' reinvestment in its own business, we're aware that returns are shrinking. Investors must think there's better things to come because the stock has knocked it out of the park, delivering a 104% gain to shareholders who have held over the last five years. But if the trajectory of these underlying trends continue, we think the likelihood of it being a multi-bagger from here isn't high.

One final note, you should learn about the 3 warning signs we've spotted with Abdullah Al-Othaim Markets (including 1 which shouldn't be ignored) .

While Abdullah Al-Othaim Markets may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:4001

Abdullah Al-Othaim Markets

Engages in the wholesale and retail trade of food supplies and other products in the Kingdom of Saudi Arabia and Arab Republic of Egypt.

Very undervalued with outstanding track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor