Advertisement

- Russia

- /

- Metals and Mining

- /

- MISX:BLNG

We're Not So Sure You Should Rely on Belon's (MCX:BLNG) Statutory Earnings

Broadly speaking, profitable businesses are less risky than unprofitable ones. That said, the current statutory profit is not always a good guide to a company's underlying profitability. This article will consider whether Belon's (MCX:BLNG) statutory profits are a good guide to its underlying earnings.

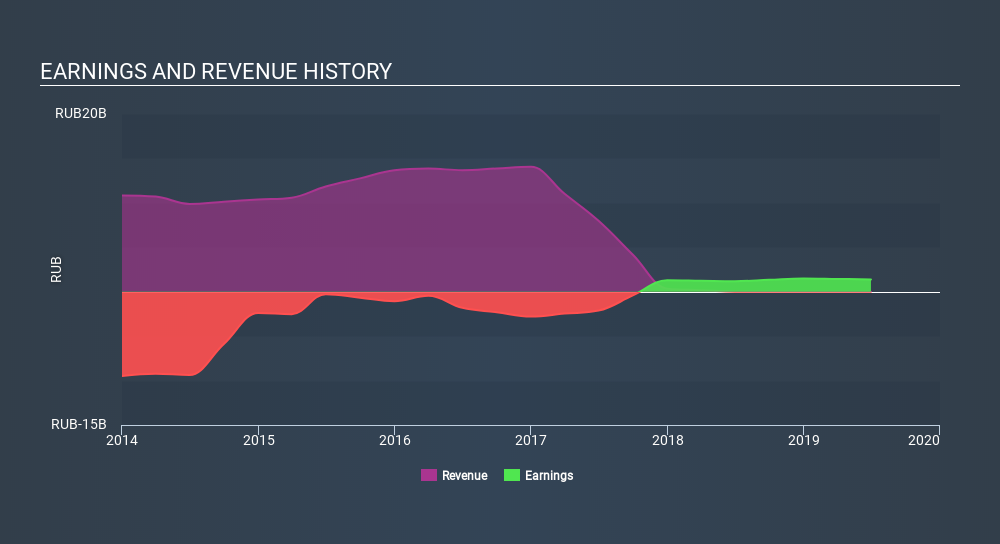

While Belon was able to generate revenue of ₽5.57m in the last twelve months, we think its profit result of ₽1.38b was more important. Even though revenue is down over the last three years, you can see in the chart below that the company has moved from loss-making to profitable.

View our latest analysis for Belon

Of course, it is only sensible to look beyond the statutory profits and question how well those numbers represent the sustainable earnings power of the business. Therefore, we think it's worth taking a closer look at Belon's cashflow, as well as examining the impact that unusual items have had on its reported profit. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Belon.

Zooming In On Belon's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. This ratio tells us how much of a company's profit is not backed by free cashflow.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

Over the twelve months to June 2019, Belon recorded an accrual ratio of 0.30. We can therefore deduce that its free cash flow fell well short of covering its statutory profit, suggesting we might want to think twice before putting a lot of weight on the latter. Even though it reported a profit of ₽1.38b, a look at free cash flow indicates it actually burnt through ₽123m in the last year. Coming off the back of negative free cash flow last year, we imagine some shareholders might wonder if its cash burn of ₽123m, this year, indicates high risk. However, that's not all there is to consider. The accrual ratio is reflecting the impact of unusual items on statutory profit, at least in part.

How Do Unusual Items Influence Profit?

Given the accrual ratio, it's not overly surprising that Belon's profit was boosted by unusual items worth ₽4.8m in the last twelve months. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. And, after all, that's exactly what the accounting terminology implies. Belon had a rather significant contribution from unusual items relative to its profit to June 2019. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On Belon's Profit Performance

Belon had a weak accrual ratio, but its profit did receive a boost from unusual items. For the reasons mentioned above, we think that a perfunctory glance at Belon's statutory profits might make it look better than it really is on an underlying level. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. Every company has risks, and we've spotted 4 warning signs for Belon (of which 2 are a bit unpleasant!) you should know about.

Our examination of Belon has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About MISX:BLNG

Belon

Belon Joint Stock Company extracts, processes, and produces coal and related products in Russia.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor