Advertisement

- Serbia

- /

- Metals and Mining

- /

- BELEX:IMPL

There Are Reasons To Feel Uneasy About IMPOL SEVAL Valjaonica Aluminijuma a.d's (BELEX:IMPL) Returns On Capital

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Having said that, from a first glance at IMPOL SEVAL Valjaonica Aluminijuma a.d (BELEX:IMPL) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for IMPOL SEVAL Valjaonica Aluminijuma a.d, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.13 = дин1.2b ÷ (дин17b - дин7.3b) (Based on the trailing twelve months to December 2021).

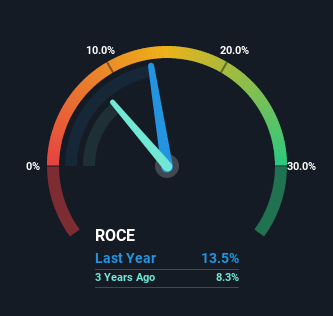

Therefore, IMPOL SEVAL Valjaonica Aluminijuma a.d has an ROCE of 13%. That's a relatively normal return on capital, and it's around the 15% generated by the Metals and Mining industry.

View our latest analysis for IMPOL SEVAL Valjaonica Aluminijuma a.d

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of IMPOL SEVAL Valjaonica Aluminijuma a.d, check out these free graphs here.

What The Trend Of ROCE Can Tell Us

When we looked at the ROCE trend at IMPOL SEVAL Valjaonica Aluminijuma a.d, we didn't gain much confidence. Around five years ago the returns on capital were 19%, but since then they've fallen to 13%. Although, given both revenue and the amount of assets employed in the business have increased, it could suggest the company is investing in growth, and the extra capital has led to a short-term reduction in ROCE. If these investments prove successful, this can bode very well for long term stock performance.

While on the subject, we noticed that the ratio of current liabilities to total assets has risen to 44%, which has impacted the ROCE. If current liabilities hadn't increased as much as they did, the ROCE could actually be even lower. And with current liabilities at these levels, suppliers or short-term creditors are effectively funding a large part of the business, which can introduce some risks.

The Bottom Line

While returns have fallen for IMPOL SEVAL Valjaonica Aluminijuma a.d in recent times, we're encouraged to see that sales are growing and that the business is reinvesting in its operations. In light of this, the stock has only gained 36% over the last five years. Therefore we'd recommend looking further into this stock to confirm if it has the makings of a good investment.

One more thing: We've identified 3 warning signs with IMPOL SEVAL Valjaonica Aluminijuma a.d (at least 1 which makes us a bit uncomfortable) , and understanding them would certainly be useful.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BELEX:IMPL

IMPOL SEVAL Valjaonica Aluminijuma a.d

Manufactures and sells aluminum products worldwide.

Low risk with weak fundamentals.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor