Advertisement

- Qatar

- /

- Industrials

- /

- DSM:IQCD

Industries Qatar Q.P.S.C. (DSM:IQCD) On An Uptrend: Could Fundamentals Be Driving The Stock?

Industries Qatar Q.P.S.C's (DSM:IQCD) stock is up by 1.2% over the past week. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to investigate if the company's decent financials had a hand to play in the recent price move. In this article, we decided to focus on Industries Qatar Q.P.S.C's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for Industries Qatar Q.P.S.C

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Industries Qatar Q.P.S.C is:

13% = ر.ق5.0b ÷ ر.ق38b (Based on the trailing twelve months to June 2024).

The 'return' is the income the business earned over the last year. That means that for every QAR1 worth of shareholders' equity, the company generated QAR0.13 in profit.

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Industries Qatar Q.P.S.C's Earnings Growth And 13% ROE

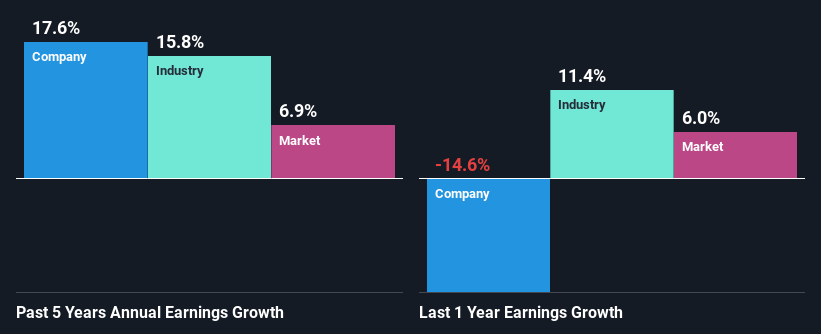

As you can see, Industries Qatar Q.P.S.C's ROE looks pretty weak. Still, the company's ROE is higher than the average industry ROE of 7.9% so that's certainly interesting. Especially considering that Industries Qatar Q.P.S.C has seen a decent 18% net income growth seen over the past five years. Bear in mind, the company does have a low ROE. It is just that the industry ROE is lower. Therefore, the growth in earnings could also be the result of other factors. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

Next, on comparing Industries Qatar Q.P.S.C's net income growth with the industry, we found that the company's reported growth is similar to the industry average growth rate of 16% over the last few years.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. If you're wondering about Industries Qatar Q.P.S.C's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Industries Qatar Q.P.S.C Using Its Retained Earnings Effectively?

The high three-year median payout ratio of 75% (or a retention ratio of 25%) for Industries Qatar Q.P.S.C suggests that the company's growth wasn't really hampered despite it returning most of its income to its shareholders.

Besides, Industries Qatar Q.P.S.C has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders. Looking at the current analyst consensus data, we can see that the company's future payout ratio is expected to rise to 93% over the next three years. However, the company's ROE is not expected to change by much despite the higher expected payout ratio.

Conclusion

On the whole, we do feel that Industries Qatar Q.P.S.C has some positive attributes. Especially the substantial growth in earnings backed by a decent ROE. Despite the company reinvesting only a small portion of its profits, it still has managed to grow its earnings so that is appreciable. With that said, the latest industry analyst forecasts reveal that the company's earnings growth is expected to slow down. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DSM:IQCD

Industries Qatar Q.P.S.C

Through its subsidiaries, operates in the petrochemical, fertilizer, and steel businesses in Qatar.

Flawless balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor