Advertisement

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Enter Air Sp. z o.o. (WSE:ENT) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Enter Air Sp. z o.o

What Is Enter Air Sp. z o.o's Debt?

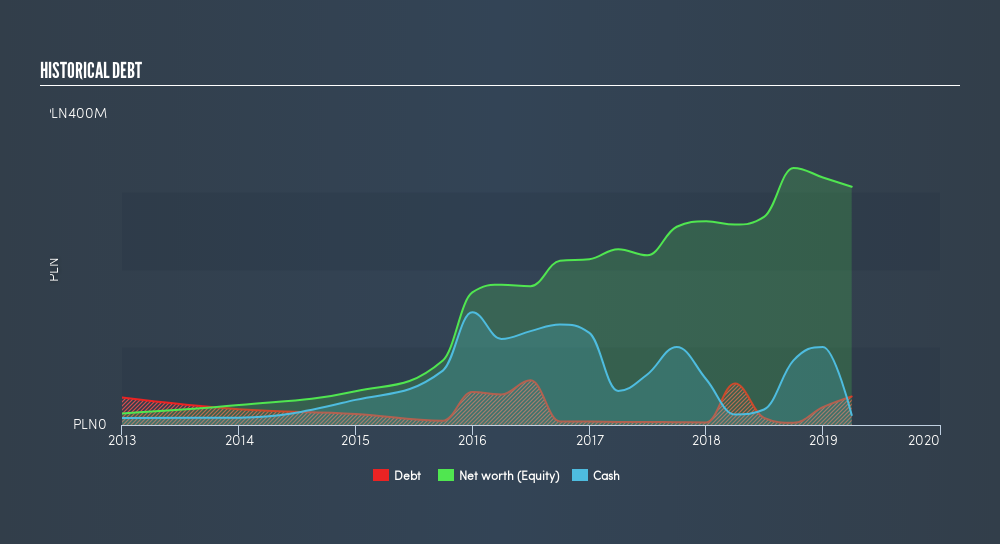

As you can see below, at the end of March 2019, Enter Air Sp. z o.o had zł729.6m of debt, up from zł400.7m a year ago. Click the image for more detail. Net debt is about the same, since the it doesn't have much cash.

A Look At Enter Air Sp. z o.o's Liabilities

According to the last reported balance sheet, Enter Air Sp. z o.o had liabilities of zł361.9m due within 12 months, and liabilities of zł1.11b due beyond 12 months. On the other hand, it had cash of zł12.7m and zł113.6m worth of receivables due within a year. So it has liabilities totalling zł1.35b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the zł603.5m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt At the end of the day, Enter Air Sp. z o.o would probably need a major re-capitalization if its creditors were to demand repayment. Either way, since Enter Air Sp. z o.o does have more debt than cash, it's worth keeping an eye on its balance sheet.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Enter Air Sp. z o.o's debt is only 3.27 times its EBITDA, and its EBIT cover its interest expense 5.31 times over. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Notably, Enter Air Sp. z o.o's EBIT launched higher than Elon Musk, gaining a whopping 189% on last year. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Enter Air Sp. z o.o will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Enter Air Sp. z o.o produced sturdy free cash flow equating to 71% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

We feel some trepidation about Enter Air Sp. z o.o's difficulty level of total liabilities, but we've got positives to focus on, too. To wit both its EBIT growth rate and conversion of EBIT to free cash flow were encouraging signs. Looking at all the angles mentioned above, it does seem to us that Enter Air Sp. z o.o is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Enter Air Sp. z o.o's earnings per share history for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About WSE:ENT

Good value with proven track record.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor