Ifirma SA's (WSE:IFI) Stock Has Seen Strong Momentum: Does That Call For Deeper Study Of Its Financial Prospects?

Ifirma (WSE:IFI) has had a great run on the share market with its stock up by a significant 16% over the last week. We wonder if and what role the company's financials play in that price change as a company's long-term fundamentals usually dictate market outcomes. Particularly, we will be paying attention to Ifirma's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

See our latest analysis for Ifirma

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Ifirma is:

51% = zł6.8m ÷ zł13m (Based on the trailing twelve months to September 2024).

The 'return' is the profit over the last twelve months. So, this means that for every PLN1 of its shareholder's investments, the company generates a profit of PLN0.51.

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Ifirma's Earnings Growth And 51% ROE

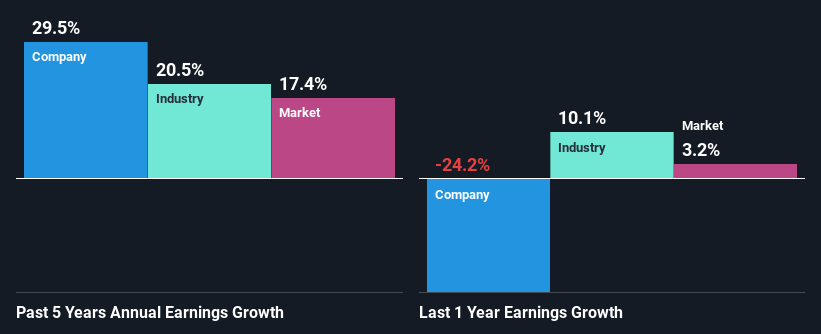

First thing first, we like that Ifirma has an impressive ROE. Second, a comparison with the average ROE reported by the industry of 18% also doesn't go unnoticed by us. So, the substantial 30% net income growth seen by Ifirma over the past five years isn't overly surprising.

Next, on comparing with the industry net income growth, we found that Ifirma's growth is quite high when compared to the industry average growth of 21% in the same period, which is great to see.

Earnings growth is a huge factor in stock valuation. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. Is Ifirma fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Ifirma Using Its Retained Earnings Effectively?

The high three-year median payout ratio of 97% (implying that it keeps only 3.0% of profits) for Ifirma suggests that the company's growth wasn't really hampered despite it returning most of the earnings to its shareholders.

Additionally, Ifirma has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 92% of its profits over the next three years. Regardless, the future ROE for Ifirma is predicted to rise to 62% despite there being not much change expected in its payout ratio.

Summary

Overall, we feel that Ifirma certainly does have some positive factors to consider. Namely, its high earnings growth, which was likely due to its high ROE. However, investors could have benefitted even more from the high ROE, had the company been reinvesting more of its earnings. As discussed earlier, the company is retaining hardly any of its profits. Up till now, we've only made a short study of the company's growth data. To gain further insights into Ifirma's past profit growth, check out this visualization of past earnings, revenue and cash flows.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:IFI

Ifirma

IFirma SA provides accounting services. The company operates a website, ifirma.pl, which offers services and tools for tax settlements and supporting business activities.

Outstanding track record with flawless balance sheet and pays a dividend.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion