Advertisement

- Poland

- /

- Real Estate

- /

- WSE:LKD

Lokum Deweloper S.A.'s (WSE:LKD) Stock On An Uptrend: Could Fundamentals Be Driving The Momentum?

Lokum Deweloper (WSE:LKD) has had a great run on the share market with its stock up by a significant 29% over the last three months. We wonder if and what role the company's financials play in that price change as a company's long-term fundamentals usually dictate market outcomes. Particularly, we will be paying attention to Lokum Deweloper's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

Check out our latest analysis for Lokum Deweloper

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Lokum Deweloper is:

17% = zł77m ÷ zł441m (Based on the trailing twelve months to March 2023).

The 'return' is the profit over the last twelve months. Another way to think of that is that for every PLN1 worth of equity, the company was able to earn PLN0.17 in profit.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Lokum Deweloper's Earnings Growth And 17% ROE

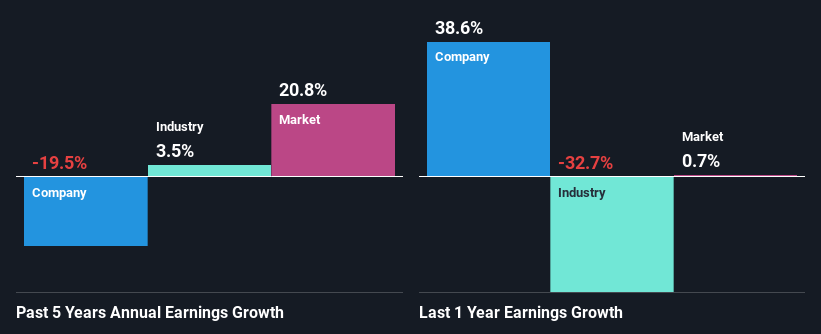

At first glance, Lokum Deweloper seems to have a decent ROE. Especially when compared to the industry average of 12% the company's ROE looks pretty impressive. For this reason, Lokum Deweloper's five year net income decline of 19% raises the question as to why the high ROE didn't translate into earnings growth. Based on this, we feel that there might be other reasons which haven't been discussed so far in this article that could be hampering the company's growth. These include low earnings retention or poor allocation of capital.

However, when we compared Lokum Deweloper's growth with the industry we found that while the company's earnings have been shrinking, the industry has seen an earnings growth of 3.5% in the same period. This is quite worrisome.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Lokum Deweloper is trading on a high P/E or a low P/E, relative to its industry.

Is Lokum Deweloper Using Its Retained Earnings Effectively?

Lokum Deweloper's declining earnings is not surprising given how the company is spending most of its profits in paying dividends, judging by its three-year median payout ratio of 53% (or a retention ratio of 47%). With only a little being reinvested into the business, earnings growth would obviously be low or non-existent. You can see the 2 risks we have identified for Lokum Deweloper by visiting our risks dashboard for free on our platform here.

Moreover, Lokum Deweloper has been paying dividends for seven years, which is a considerable amount of time, suggesting that management must have perceived that the shareholders prefer consistent dividends even though earnings have been shrinking. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to rise to 91% over the next three years. Therefore, the expected rise in the payout ratio explains why the company's ROE is expected to decline to 7.3% over the same period.

Conclusion

Overall, we feel that Lokum Deweloper certainly does have some positive factors to consider. Although, we are disappointed to see a lack of growth in earnings even in spite of a high ROE. Bear in mind, the company reinvests a small portion of its profits, which means that investors aren't reaping the benefits of the high rate of return. Additionally, the latest industry analyst forecasts show that the company is expected to continue to see a similar decline in its earnings in the future as well. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:LKD

Lokum Deweloper

Develops and sells residential and commercial properties in Poland.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor