Advertisement

- Poland

- /

- Interactive Media and Services

- /

- WSE:ICG

We Think Ice Code Games (WSE:ICG) Can Easily Afford To Drive Business Growth

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

Given this risk, we thought we'd take a look at whether Ice Code Games (WSE:ICG) shareholders should be worried about its cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for Ice Code Games

How Long Is Ice Code Games' Cash Runway?

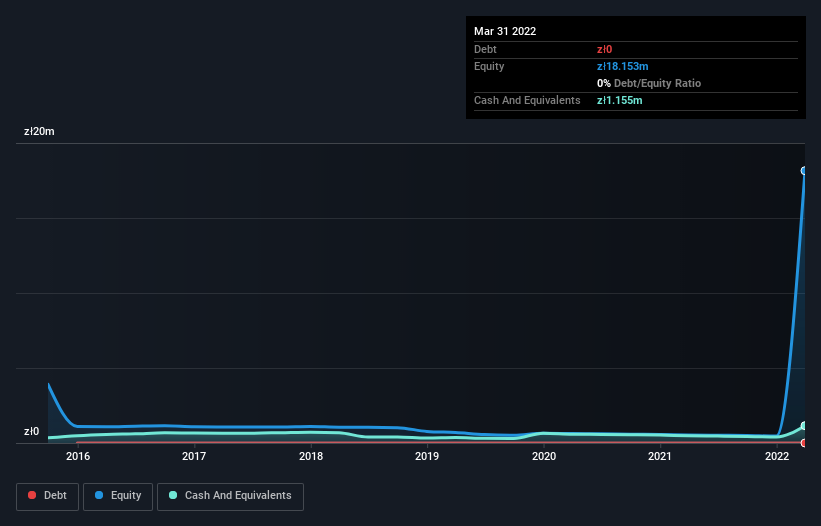

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. In March 2022, Ice Code Games had zł1.2m in cash, and was debt-free. Importantly, its cash burn was zł8.5k over the trailing twelve months. That means it had a cash runway of very many years as of March 2022. While this is only one measure of its cash burn situation, it certainly gives us the impression that holders have nothing to worry about. You can see how its cash balance has changed over time in the image below.

How Is Ice Code Games' Cash Burn Changing Over Time?

In our view, Ice Code Games doesn't yet produce significant amounts of operating revenue, since it reported just zł276k in the last twelve months. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. The good news, from a balance sheet perspective, is that it actually reduced its cash burn by 92% in the last twelve months. While that hardly points to growth potential, it does at least suggest the company is trying to survive. Ice Code Games makes us a little nervous due to its lack of substantial operating revenue. We prefer most of the stocks on this list of stocks that analysts expect to grow.

How Easily Can Ice Code Games Raise Cash?

While we're comforted by the recent reduction evident from our analysis of Ice Code Games' cash burn, it is still worth considering how easily the company could raise more funds, if it wanted to accelerate spending to drive growth. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of zł127m, Ice Code Games' zł8.5k in cash burn equates to about 0.007% of its market value. So it could almost certainly just borrow a little to fund another year's growth, or else easily raise the cash by issuing a few shares.

Is Ice Code Games' Cash Burn A Worry?

As you can probably tell by now, we're not too worried about Ice Code Games' cash burn. For example, we think its cash burn reduction suggests that the company is on a good path. But it's fair to say that its cash burn relative to its market cap was also very reassuring. Looking at all the measures in this article, together, we're not worried about its rate of cash burn, which seems to be under control. Separately, we looked at different risks affecting the company and spotted 5 warning signs for Ice Code Games (of which 4 are significant!) you should know about.

Of course Ice Code Games may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:ICG

Medium-low risk with weak fundamentals.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor