Advertisement

What You Should Know About Plasma System S.A.'s (WSE:PSM) Financial Strength

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Plasma System S.A. (WSE:PSM) is a small-cap stock with a market capitalization of zł1.9m. While investors primarily focus on the growth potential and competitive landscape of the small-cap companies, they end up ignoring a key aspect, which could be the biggest threat to its existence: its financial health. Why is it important? Given that PSM is not presently profitable, it’s crucial to understand the current state of its operations and pathway to profitability. We'll look at some basic checks that can form a snapshot the company’s financial strength. However, this is not a comprehensive overview, so I’d encourage you to dig deeper yourself into PSM here.

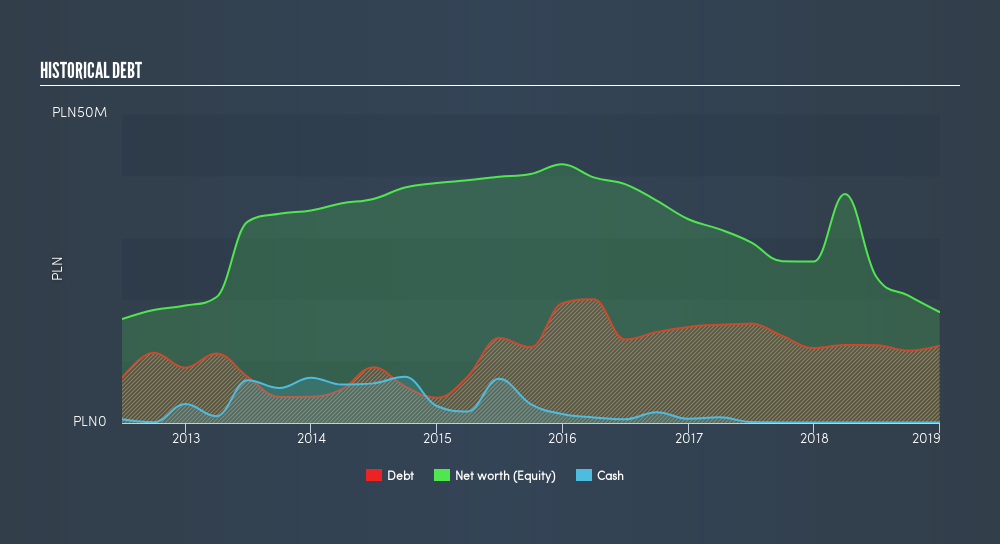

PSM’s Debt (And Cash Flows)

PSM has sustained its debt level by about zł13m over the last 12 months which accounts for long term debt. At this stable level of debt, PSM currently has zł68k remaining in cash and short-term investments to keep the business going. We note it produced negative cash flow over the last twelve months. For this article’s sake, I won’t be looking at this today, but you can take a look at some of PSM’s operating efficiency ratios such as ROA here.

Does PSM’s liquid assets cover its short-term commitments?

With current liabilities at zł18m, it seems that the business may not have an easy time meeting these commitments with a current assets level of zł3.8m, leading to a current ratio of 0.21x. The current ratio is calculated by dividing current assets by current liabilities.

Is PSM’s debt level acceptable?

PSM is a relatively highly levered company with a debt-to-equity of 70%. This is somewhat unusual for small-caps companies, since lenders are often hesitant to provide attractive interest rates to less-established businesses. However, since PSM is presently unprofitable, sustainability of its current state of operations becomes a concern. Running high debt, while not yet making money, can be risky in unexpected downturns as liquidity may dry up, making it hard to operate.

Next Steps:

Although PSM’s debt level is towards the higher end of the spectrum, its cash flow coverage seems adequate to meet debt obligations which means its debt is being efficiently utilised. But, its lack of liquidity raises questions over current asset management practices for the small-cap. This is only a rough assessment of financial health, and I'm sure PSM has company-specific issues impacting its capital structure decisions. You should continue to research Plasma System to get a better picture of the stock by looking at:

- Historical Performance: What has PSM's returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About WSE:PSM

Plasma System

Plasma System S.A., a technological company, provides services in the area of surface engineering in Poland and internationally.

Slightly overvalued with weak fundamentals.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor