Advertisement

In a week marked by tariff uncertainties and softer-than-expected U.S. job growth, global markets have shown mixed performances, with the S&P 500 Index experiencing a slight decline and European indices defying trade concerns to post gains. Amid these fluctuations, small-cap stocks are drawing attention as potential opportunities for investors seeking growth in an environment where broader market sentiment remains cautious. In this context, identifying undiscovered gems requires a keen eye for companies that can navigate economic challenges while capitalizing on niche market positions or innovative strategies.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Darya-Varia Laboratoria | NA | 1.44% | -11.65% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Boursa Kuwait Securities Company K.P.S.C | NA | 14.28% | 2.26% | ★★★★★★ |

| Interactive Digital Technologies | 1.30% | 6.10% | 4.63% | ★★★★★☆ |

| Berger Paints Bangladesh | 3.72% | 10.32% | 7.30% | ★★★★★☆ |

| Eclatorq Technology | 37.47% | 8.43% | 18.41% | ★★★★★☆ |

| National Investments Company K.S.C.P | 26.01% | 3.66% | 4.99% | ★★★★☆☆ |

| Al-Deera Holding Company K.P.S.C | 6.11% | 51.44% | 59.77% | ★★★★☆☆ |

| Central Cooperative Bank AD | 4.88% | 37.94% | 537.05% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

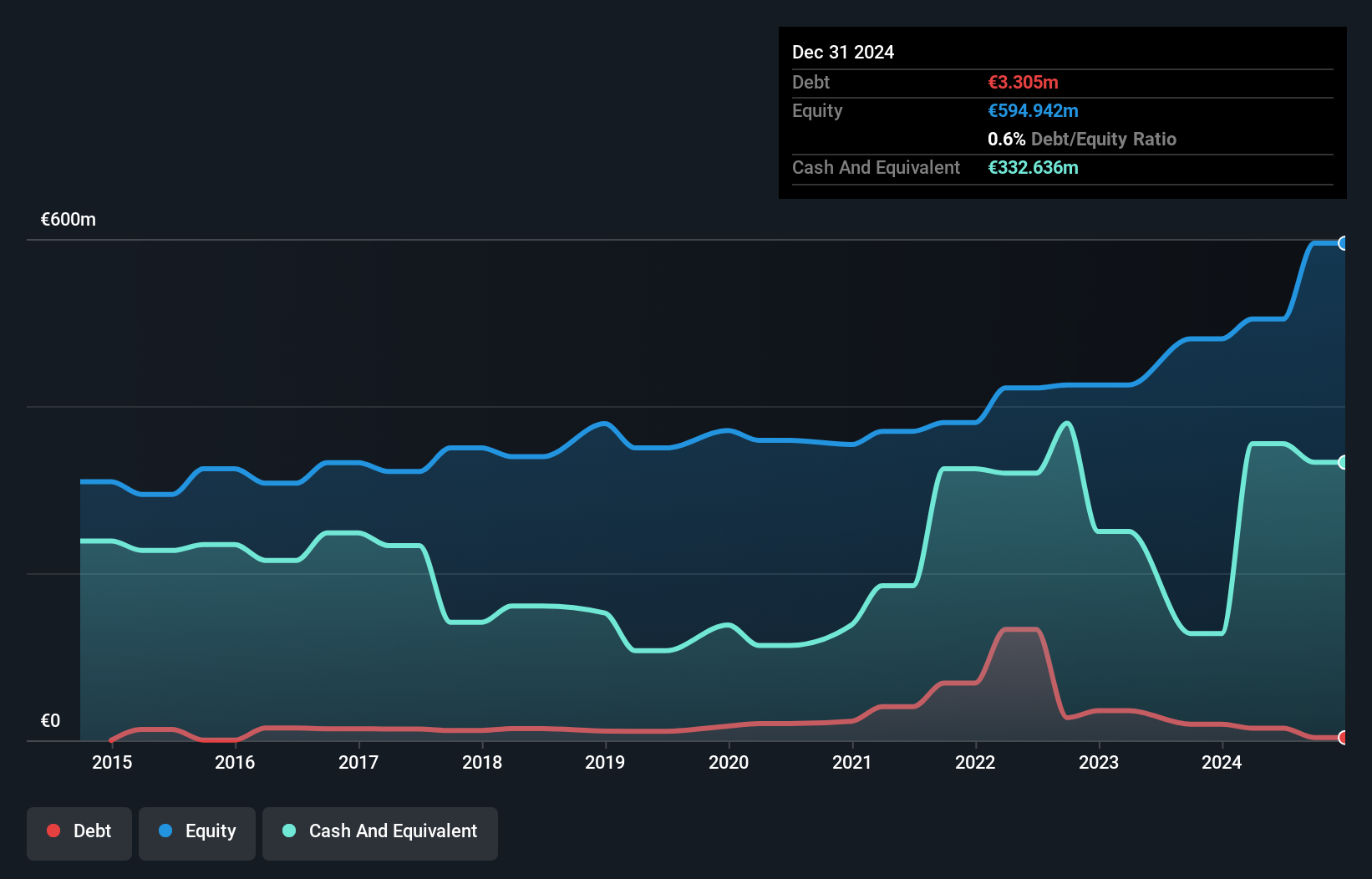

Électricite de Strasbourg Société Anonyme (ENXTPA:ELEC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Électricite de Strasbourg Société Anonyme is involved in supplying electricity and natural gas to individuals, businesses, and local authorities in France, with a market capitalization of approximately €906.93 million.

Operations: Électricite de Strasbourg Société Anonyme generates revenue primarily from the production and distribution of electricity and gas, amounting to €1.24 billion, followed by its role as an electricity distributor with €302.94 million in revenue. The company reports a net profit margin that reflects its financial efficiency in managing costs relative to its total revenues.

Électricite de Strasbourg, a relatively small player in the electric utilities sector, has demonstrated impressive financial health. The company’s earnings surged by 97% over the past year, significantly outpacing the industry average of -6%. Trading at 91.5% below its estimated fair value suggests potential undervaluation. With more cash than total debt and a reduced debt-to-equity ratio from 3.1 to 2.9 over five years, financial stability seems robust. The firm is anticipated to report its Q4 2024 results soon, which could provide further insights into its growth trajectory and market positioning within the industry context.

- Dive into the specifics of Électricite de Strasbourg Société Anonyme here with our thorough health report.

Learn about Électricite de Strasbourg Société Anonyme's historical performance.

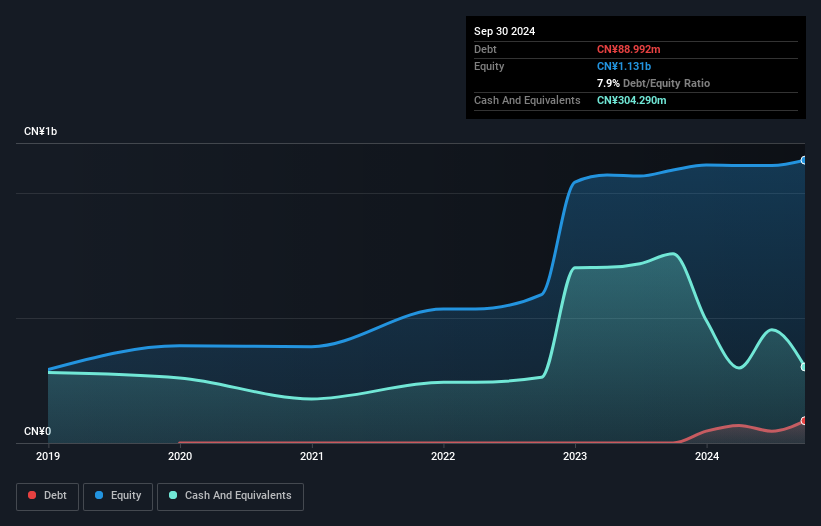

Zhejiang Weigang Technology (SZSE:001256)

Simply Wall St Value Rating: ★★★★★☆

Overview: Zhejiang Weigang Technology Co., Ltd. specializes in providing label printing and converting machines in China, with a market cap of CN¥2.66 billion.

Operations: Weigang Technology generates revenue primarily from the sale of label printing and converting machines. The company's market capitalization is approximately CN¥2.66 billion, reflecting its financial standing in the industry.

Zhejiang Weigang Technology, a small player in the machinery sector, has shown promising earnings growth of 16.5% over the past year, outpacing the industry average of -0.06%. This company boasts high-quality earnings and a price-to-earnings ratio of 27.3x, which is attractive compared to the broader CN market's 36.4x. However, its debt-to-equity ratio has increased to 7.9% over five years, though it maintains more cash than total debt. Recently, they completed a share buyback of 750,000 shares for CNY10 million and plan to use surplus funds for additional projects discussed at their shareholder meeting on February 14th.

- Click to explore a detailed breakdown of our findings in Zhejiang Weigang Technology's health report.

Understand Zhejiang Weigang Technology's track record by examining our Past report.

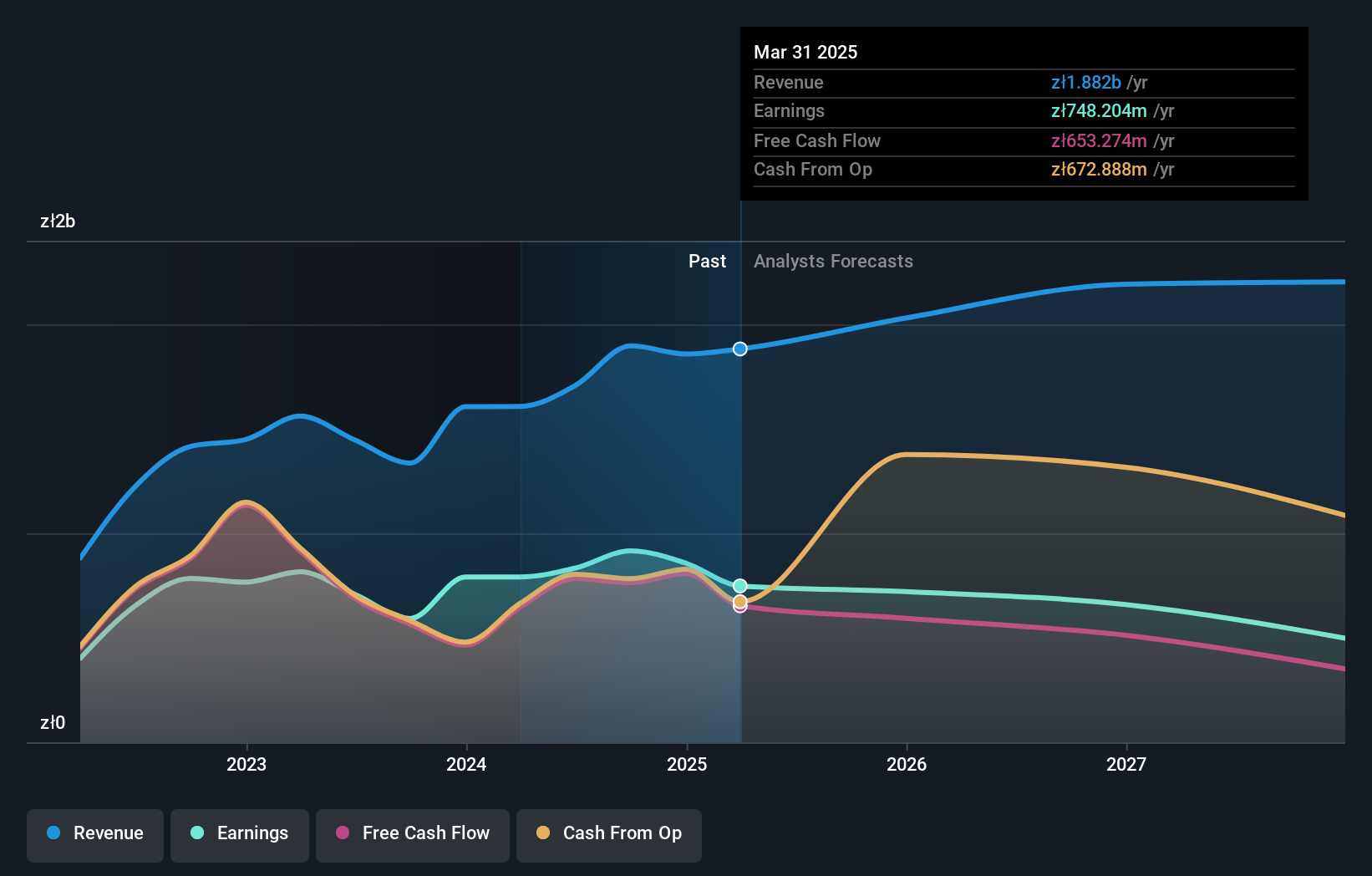

XTB (WSE:XTB)

Simply Wall St Value Rating: ★★★★☆☆

Overview: XTB S.A. is a brokerage firm offering ETF, currency derivatives, commodities, indices, stocks, and bonds services across Central and Eastern Europe, Western Europe, Latin America, and the Middle East with a market cap of PLN7.74 billion.

Operations: XTB generates revenue primarily from brokerage services in ETF, currency derivatives, commodities, indices, stocks, and bonds. The company operates across various regions including Central and Eastern Europe, Western Europe, Latin America, and the Middle East.

XTB, a financial player with a market cap on the smaller side, has demonstrated impressive earnings growth of 8.6% over the past year, surpassing its industry peers. Despite an increase in its debt to equity ratio from 4.8% to 8.1% over five years, it remains financially robust with more cash than total debt and high-quality earnings. Trading at 37.5% below fair value estimates suggests potential undervaluation opportunities for investors looking for hidden gems in capital markets. However, future prospects seem mixed as earnings are projected to decline by an average of 16.8% annually over the next three years while revenue is expected to grow by a modest rate of 5%.

- Delve into the full analysis health report here for a deeper understanding of XTB.

Examine XTB's past performance report to understand how it has performed in the past.

Turning Ideas Into Actions

- Dive into all 4701 of the Undiscovered Gems With Strong Fundamentals we have identified here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Weigang Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:001256

Zhejiang Weigang Technology

Provides label printing machines and converting machines in China.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor