Advertisement

- Poland

- /

- Consumer Finance

- /

- WSE:KPI

The Price Is Right For Kancelaria Prawna-Inkaso WEC Spólka Akcyjna (WSE:KPI)

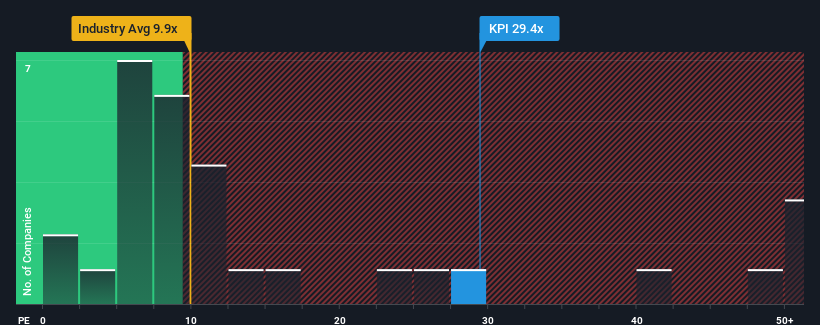

Kancelaria Prawna-Inkaso WEC Spólka Akcyjna's (WSE:KPI) price-to-earnings (or "P/E") ratio of 29.4x might make it look like a strong sell right now compared to the market in Poland, where around half of the companies have P/E ratios below 12x and even P/E's below 7x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

For instance, Kancelaria Prawna-Inkaso WEC Spólka Akcyjna's receding earnings in recent times would have to be some food for thought. One possibility is that the P/E is high because investors think the company will still do enough to outperform the broader market in the near future. If not, then existing shareholders may be quite nervous about the viability of the share price.

View our latest analysis for Kancelaria Prawna-Inkaso WEC Spólka Akcyjna

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Kancelaria Prawna-Inkaso WEC Spólka Akcyjna's to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 36%. Even so, admirably EPS has lifted 111% in aggregate from three years ago, notwithstanding the last 12 months. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Comparing that to the market, which is only predicted to deliver 16% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

With this information, we can see why Kancelaria Prawna-Inkaso WEC Spólka Akcyjna is trading at such a high P/E compared to the market. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the bourse.

The Final Word

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Kancelaria Prawna-Inkaso WEC Spólka Akcyjna revealed its three-year earnings trends are contributing to its high P/E, given they look better than current market expectations. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

You should always think about risks. Case in point, we've spotted 5 warning signs for Kancelaria Prawna-Inkaso WEC Spólka Akcyjna you should be aware of, and 3 of them shouldn't be ignored.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Kancelaria Prawna-Inkaso WEC Spólka Akcyjna might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:KPI

Kancelaria Prawna-Inkaso WEC Spólka Akcyjna

Engages in the debt collection and monitoring business in Poland.

Moderate with questionable track record.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor