Advertisement

- Poland

- /

- Capital Markets

- /

- WSE:CSR

Caspar Asset Management (WSE:CSR) Is Paying Out Less In Dividends Than Last Year

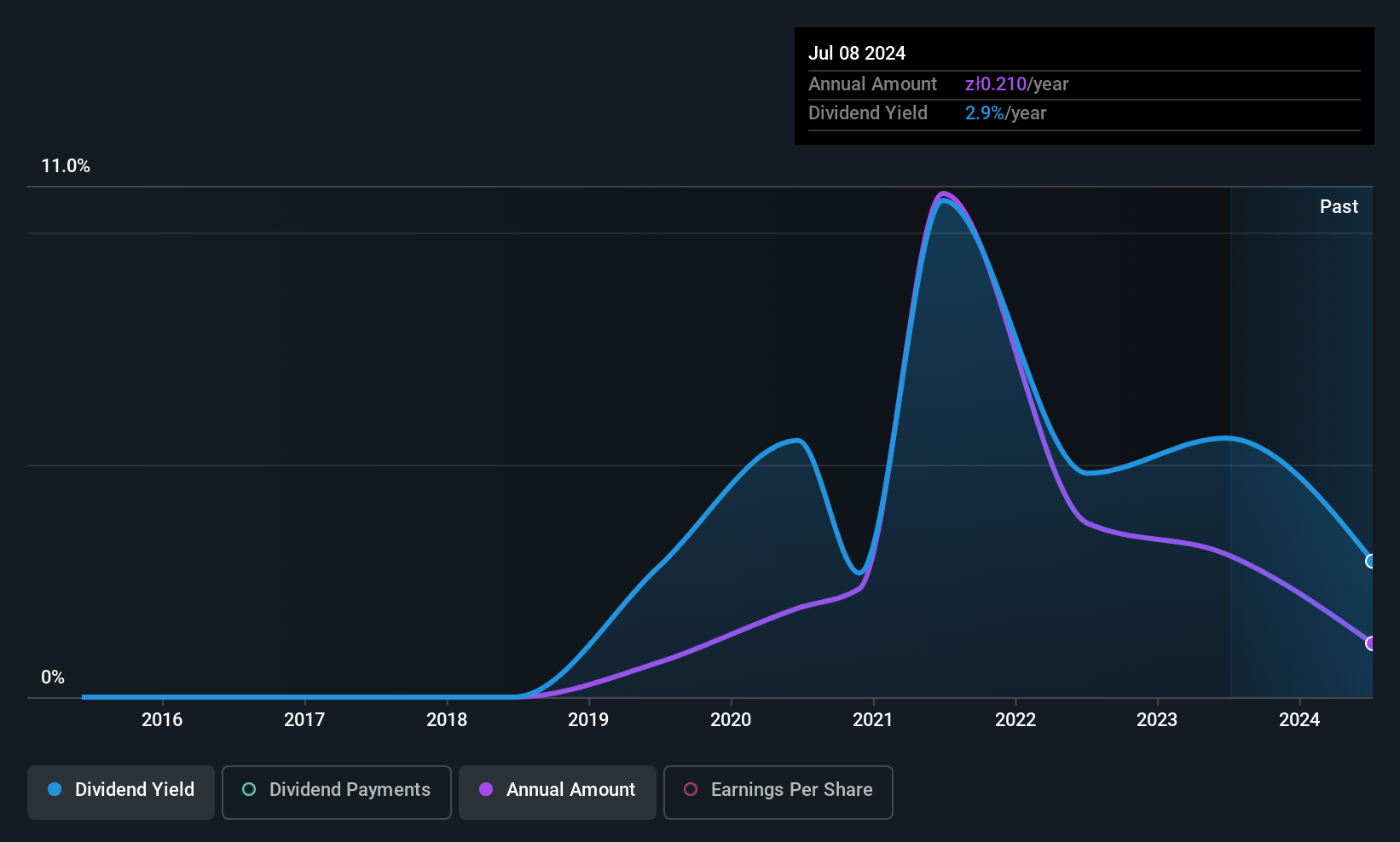

Caspar Asset Management S.A. (WSE:CSR) has announced it will be reducing its dividend payable on the 21st of July to PLN0.10, which is 52% lower than what investors received last year for the same period. This means that the annual payment is 3.5% of the current stock price, which is lower than what the rest of the industry is paying.

Caspar Asset Management's Future Dividend Projections Appear Well Covered By Earnings

If it is predictable over a long period, even low dividend yields can be attractive. Based on the last payment, Caspar Asset Management's profits didn't cover the dividend, but the company was generating enough cash instead. Generally, we think cash is more important than accounting measures of profit, so with the cash flows easily covering the dividend, we don't think there is much reason to worry.

Looking forward, EPS could fall by 13.6% if the company can't turn things around from the last few years. If the dividend continues along the path it has been on recently, we estimate the payout ratio could be 52%, which is an improvement from where it is currently.

See our latest analysis for Caspar Asset Management

Caspar Asset Management's Dividend Has Lacked Consistency

Even in its relatively short history, the company has reduced the dividend at least once. This makes us cautious about the consistency of the dividend over a full economic cycle. Since 2019, the annual payment back then was PLN0.136, compared to the most recent full-year payment of PLN0.21. This implies that the company grew its distributions at a yearly rate of about 7.5% over that duration. A reasonable rate of dividend growth is good to see, but we're wary that the dividend history is not as solid as we'd like, having been cut at least once.

The Dividend Has Limited Growth Potential

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Earnings per share has been sinking by 14% over the last five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future.

Caspar Asset Management's Dividend Doesn't Look Sustainable

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We would probably look elsewhere for an income investment.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. To that end, Caspar Asset Management has 4 warning signs (and 1 which shouldn't be ignored) we think you should know about. Is Caspar Asset Management not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:CSR

Caspar Asset Management

Provides asset management services to individual and institutional clients in the Western Europe, the United States, and Poland markets.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor