Advertisement

- Poland

- /

- Construction

- /

- WSE:MRB

Mirbud's (WSE:MRB) Sluggish Earnings Might Be Just The Beginning Of Its Problems

Mirbud S.A.'s (WSE:MRB) stock showed strength, with investors undeterred by its weak earnings report. While shareholders may be willing to overlook soft profit numbers, we believe that they should also be taking into account some other factors which may be cause for concern.

Our free stock report includes 2 warning signs investors should be aware of before investing in Mirbud. Read for free now.

Examining Cashflow Against Mirbud's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

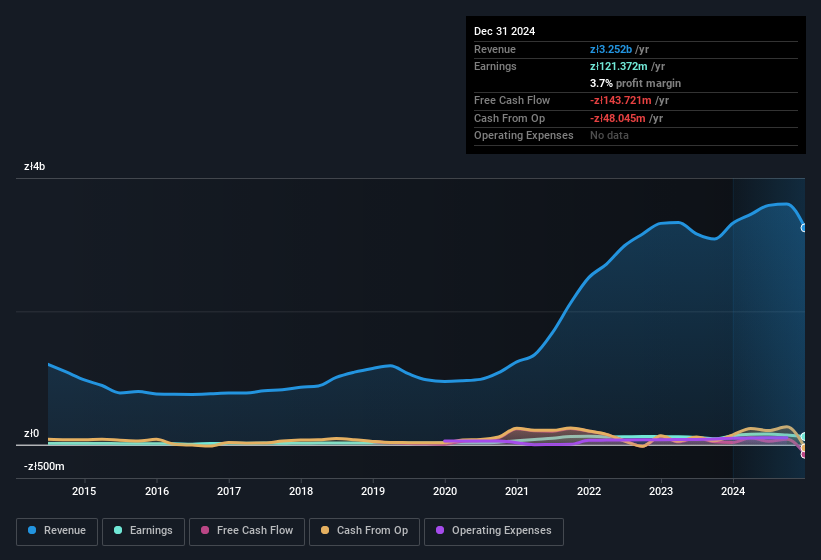

Over the twelve months to December 2024, Mirbud recorded an accrual ratio of 0.33. Therefore, we know that it's free cashflow was significantly lower than its statutory profit, raising questions about how useful that profit figure really is. In the last twelve months it actually had negative free cash flow, with an outflow of zł144m despite its profit of zł121.4m, mentioned above. We saw that FCF was zł33m a year ago though, so Mirbud has at least been able to generate positive FCF in the past. Unfortunately for shareholders, the company has also been issuing new shares, diluting their share of future earnings.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Mirbud.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. In fact, Mirbud increased the number of shares on issue by 20% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. You can see a chart of Mirbud's EPS by clicking here.

How Is Dilution Impacting Mirbud's Earnings Per Share (EPS)?

Unfortunately, Mirbud's profit is down 5.2% per year over three years. And even focusing only on the last twelve months, we see profit is down 10%. Like a sack of potatoes thrown from a delivery truck, EPS fell harder, down 25% in the same period. Therefore, the dilution is having a noteworthy influence on shareholder returns.

If Mirbud's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Our Take On Mirbud's Profit Performance

In conclusion, Mirbud has weak cashflow relative to earnings, which indicates lower quality earnings, and the dilution means that shareholders now own a smaller proportion of the company (assuming they maintained the same number of shares). For the reasons mentioned above, we think that a perfunctory glance at Mirbud's statutory profits might make it look better than it really is on an underlying level. If you'd like to know more about Mirbud as a business, it's important to be aware of any risks it's facing. For example, we've found that Mirbud has 2 warning signs (1 is a bit concerning!) that deserve your attention before going any further with your analysis.

Our examination of Mirbud has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:MRB

Mirbud

Operates as a general contractor in the construction industry in Poland.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.8% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|43.5% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|61.4% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.9% undervalued

UN

Community Contributor