Some Analysts Just Cut Their Santander Bank Polska S.A. (WSE:SPL) Estimates

Market forces rained on the parade of Santander Bank Polska S.A. (WSE:SPL) shareholders today, when the analysts downgraded their forecasts for this year. There was a fairly draconian cut to their revenue estimates, perhaps an implicit admission that previous forecasts were much too optimistic.

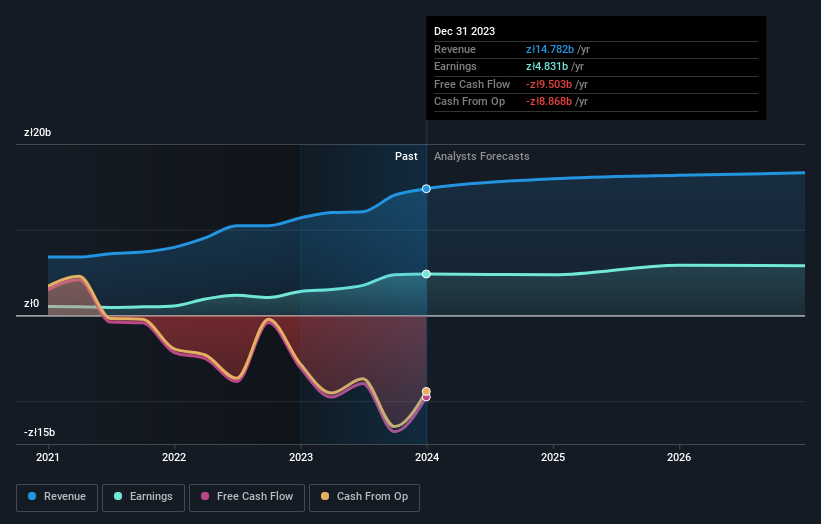

Following the downgrade, the latest consensus from Santander Bank Polska's six analysts is for revenues of zł16b in 2024, which would reflect a credible 7.8% improvement in sales compared to the last 12 months. Per-share earnings are expected to ascend 17% to zł55.39. Before this latest update, the analysts had been forecasting revenues of zł16b and earnings per share (EPS) of zł53.40 in 2024. So there seems to have been a moderate uplift in analyst sentiment with the latest consensus release, given the upgrades to both revenue and earnings per share forecasts for this year.

Check out our latest analysis for Santander Bank Polska

Although the analysts have upgraded their earnings estimates, there was no change to the consensus price target of zł530, suggesting that the forecast performance does not have a long term impact on the company's valuation.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that Santander Bank Polska's revenue growth is expected to slow, with the forecast 11% annualised growth rate until the end of 2024 being well below the historical 15% p.a. growth over the last five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 4.9% per year. So it's pretty clear that, while Santander Bank Polska's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. Fortunately, analysts also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. Often, one downgrade can set off a daisy-chain of cuts, especially if an industry is in decline. So we wouldn't be surprised if the market became a lot more cautious on Santander Bank Polska after today.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At Simply Wall St, we have a full range of analyst estimates for Santander Bank Polska going out to 2026, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:SPL

Santander Bank Polska

Provides various banking products and services for individuals, small or medium-sized enterprises, corporate clients, and public sector institutions.

Established dividend payer and good value.

Market Insights

Community Narratives