Advertisement

Bank Polska Kasa Opieki (WSE:PEO) Is Paying Out Less In Dividends Than Last Year

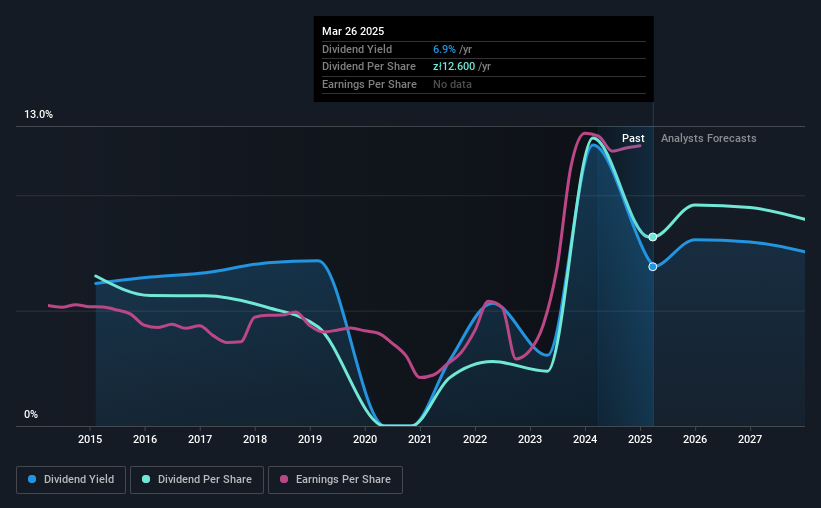

Bank Polska Kasa Opieki S.A. (WSE:PEO) is reducing its dividend from last year's comparable payment to PLN12.60 on the 23rd of May. However, the dividend yield of 6.9% is still a decent boost to shareholder returns.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Bank Polska Kasa Opieki's stock price has increased by 31% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

Bank Polska Kasa Opieki's Dividend Forecasted To Be Well Covered By Earnings

If the payments aren't sustainable, a high yield for a few years won't matter that much.

Bank Polska Kasa Opieki has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. Based on Bank Polska Kasa Opieki's last earnings report, the payout ratio is at a decent 52%, meaning that the company is able to pay out its dividend with a bit of room to spare.

EPS is set to fall by 10.2% over the next 3 years. However, as estimated by analysts, the future payout ratio could be 62% over the same time period, which we think the company can easily maintain.

View our latest analysis for Bank Polska Kasa Opieki

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The annual payment during the last 10 years was PLN10.00 in 2015, and the most recent fiscal year payment was PLN12.60. This works out to be a compound annual growth rate (CAGR) of approximately 2.3% a year over that time. It's encouraging to see some dividend growth, but the dividend has been cut at least once, and the size of the cut would eliminate most of the growth anyway, which makes this less attractive as an income investment.

The Dividend Looks Likely To Grow

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Bank Polska Kasa Opieki has impressed us by growing EPS at 24% per year over the past five years. The company's earnings per share has grown rapidly in recent years, and it has a good balance between reinvesting and paying dividends to shareholders, so we think that Bank Polska Kasa Opieki could prove to be a strong dividend payer.

We Really Like Bank Polska Kasa Opieki's Dividend

Overall, we think that Bank Polska Kasa Opieki could be a great option for a dividend investment, although we would have preferred if the dividend wasn't cut this year. The cut will allow the company to continue paying out the dividend without putting the balance sheet under pressure, which means that it could remain sustainable for longer. All of these factors considered, we think this has solid potential as a dividend stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Case in point: We've spotted 2 warning signs for Bank Polska Kasa Opieki (of which 1 is a bit concerning!) you should know about. Is Bank Polska Kasa Opieki not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Bank Polska Kasa Opieki might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:PEO

Bank Polska Kasa Opieki

A commercial bank, provides banking products and services to retail and corporate clients in Poland.

Undervalued with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor