Advertisement

- New Zealand

- /

- Renewable Energy

- /

- NZSE:NWF

NZ Windfarms Limited's (NZSE:NWF) On An Uptrend But Financial Prospects Look Pretty Weak: Is The Stock Overpriced?

NZ Windfarms (NZSE:NWF) has had a great run on the share market with its stock up by a significant 40% over the last three months. However, in this article, we decided to focus on its weak fundamentals, as long-term financial performance of a business is what ultimatley dictates market outcomes. Specifically, we decided to study NZ Windfarms' ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

Check out our latest analysis for NZ Windfarms

How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for NZ Windfarms is:

4.2% = NZ$1.7m ÷ NZ$41m (Based on the trailing twelve months to June 2020).

The 'return' refers to a company's earnings over the last year. Another way to think of that is that for every NZ$1 worth of equity, the company was able to earn NZ$0.04 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of NZ Windfarms' Earnings Growth And 4.2% ROE

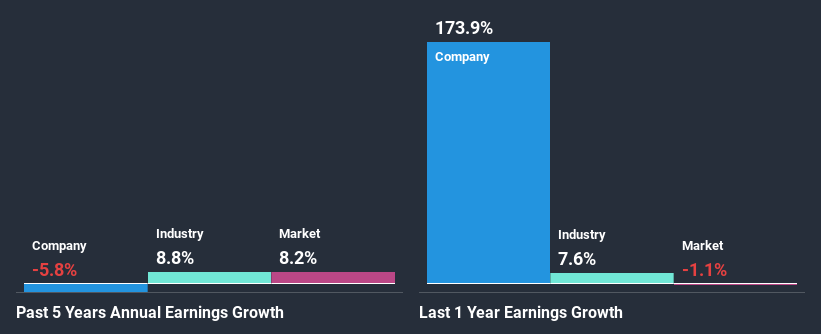

It is hard to argue that NZ Windfarms' ROE is much good in and of itself. However, the fact that it is higher than the industry average of 3.5% makes us a bit more interested. Or may be not, given NZ Windfarms' five year net income decline of 5.8% in the past five years. Remember, the company's ROE is quite low to begin with, just that it is higher than the industry average. So that's what might be causing earnings growth to shrink.

However, when we compared NZ Windfarms' growth with the industry we found that while the company's earnings have been shrinking, the industry has seen an earnings growth of 8.8% in the same period. This is quite worrisome.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is NZ Windfarms fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is NZ Windfarms Using Its Retained Earnings Effectively?

NZ Windfarms' very high three-year median payout ratio of 244% over the last three years suggests that the company is paying its shareholders more than what it is earning and this explains the company's shrinking earnings. Paying a dividend higher than reported profits is not a sustainable move. You can see the 3 risks we have identified for NZ Windfarms by visiting our risks dashboard for free on our platform here.

Moreover, NZ Windfarms has been paying dividends for three years, which is a considerable amount of time, suggesting that management must have perceived that the shareholders prefer consistent dividends even though earnings have been shrinking.

Summary

In total, we would have a hard think before deciding on any investment action concerning NZ Windfarms. Its earnings growth particularly is not much to talk about even though it does have a pretty respectable ROE. The lack of growth can be blamed on its poor earnings retention. As discussed earlier, the company is retaining hardly any of its profits. So far, we've only made a quick discussion around the company's earnings growth. So it may be worth checking this free detailed graph of NZ Windfarms' past earnings, as well as revenue and cash flows to get a deeper insight into the company's performance.

If you’re looking to trade NZ Windfarms, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if NZ Windfarms might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NZSE:NWF

NZ Windfarms

Generates and sells renewable electricity to the national grid in New Zealand.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor