Advertisement

- New Zealand

- /

- Software

- /

- NZSE:GTK

Gentrack Group (NZSE:GTK): Evaluating Valuation After Strong 2025 Earnings and Strategic Platform Wins

Simply Wall St

Reviewed by Simply Wall St

Gentrack Group (NZSE:GTK) has just reported a strong set of full-year earnings, highlighting a jump in both revenue and net income for 2025. This was accompanied by positive updates on its international platform strategy.

See our latest analysis for Gentrack Group.

Following the earnings announcement and new client wins for its g2 platform, Gentrack Group’s share price has leapt 39% in the past week, reflecting renewed optimism after a period of tepid returns. Its one-year total shareholder return remains down 23%. Over the longer term, momentum is still apparent thanks to a substantial 324% total shareholder return over the past three years. This turnaround has caught many eyes even amid a dip earlier this year.

If Gentrack's revival has sparked your curiosity, this could be the perfect moment to broaden your view and discover fast growing stocks with high insider ownership

But after such a sharp rebound and strong earnings, the question remains: is Gentrack Group’s rapid growth already reflected in its share price, or could investors still be looking at an attractive entry point?

Price-to-Earnings of 53.6x: Is it justified?

Gentrack Group is currently trading at a price-to-earnings (PE) ratio of 53.6x, which is well above both its peer average of 16.6x and the global software industry average of 27.1x. This lofty multiple places the stock in significantly more expensive territory relative to similar companies.

The PE ratio compares a company’s current share price to its per-share earnings, serving as a way to gauge how much investors are willing to pay today for a dollar of future earnings. For technology and software firms like Gentrack Group, investors often accept higher PE ratios if they believe in sustained strong earnings growth or groundbreaking products in development.

Gentrack’s current high multiple suggests that the market has already priced in much of the company’s recent earnings growth. The company not only comfortably surpasses both the New Zealand market and its industry in annual profit growth forecasts, but it has also delivered extraordinary triple-digit profit growth rates in the past year. However, at these valuation levels, the bar for future performance remains high and price corrections could occur if growth slows.

Compared to its New Zealand software peers and the global software industry, Gentrack’s valuation stands out as notably expensive. The absence of data for a “fair” ratio leaves the current pricing exposed to shifts in investor sentiment or unmet financial expectations.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 53.6x (OVERVALUED)

However, ongoing high expectations and any slip in annual profit or revenue growth could quickly cool current investor enthusiasm for Gentrack Group.

Find out about the key risks to this Gentrack Group narrative.

Another View: What Does the SWS DCF Model Say?

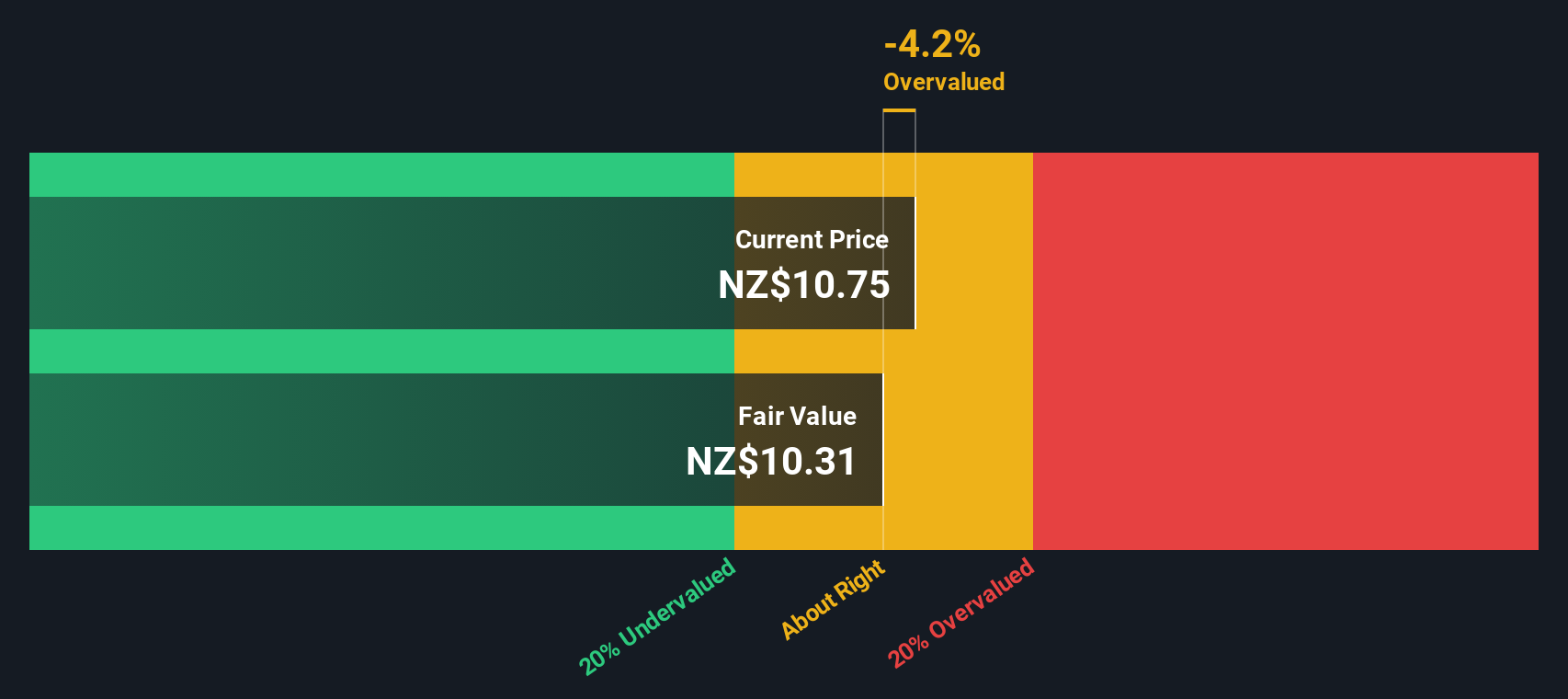

Looking at our DCF model, Gentrack Group appears to be trading just slightly above our calculated fair value of NZ$10.31, with shares at NZ$10.39. This suggests that despite premium multiples, the current price may not be dramatically overvalued from a cash flow perspective. Does this alternative outlook indicate limited risk, or will the market still demand stronger growth?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Gentrack Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 928 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Gentrack Group Narrative

If you see the story differently or want to dive into your own analysis, you can build a personal view in just a few minutes. Do it your way

A great starting point for your Gentrack Group research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors always keep an eye out for the next big opportunity and never settle for just one great story. Step up your game by checking out these hand-picked stock ideas tailor-made for today's market:

- Kickstart your hunt for the next breakout company with these 3579 penny stocks with strong financials, which combine rapid growth with robust financial health.

- Tap into unstoppable trends by zeroing in on these 30 healthcare AI stocks, driving medical innovation and redefining the future of patient care.

- Capitalize on steady income streams by reviewing these 15 dividend stocks with yields > 3%, featuring attractive yields above 3% and a track record of rewarding shareholders.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NZSE:GTK

Gentrack Group

Engages in the development, integration, and support of enterprise billing and customer management software solutions for the energy and water utility, and airport industries.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

JO

JohnJ on Worldline ·

No miracle in sight

Fair Value:€7.0178.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

79 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative