Advertisement

- New Zealand

- /

- Food

- /

- NZSE:PGW

Shareholders Would Not Be Objecting To PGG Wrightson Limited's (NZSE:PGW) CEO Compensation And Here's Why

We have been pretty impressed with the performance at PGG Wrightson Limited (NZSE:PGW) recently and CEO Stephen Guerin deserves a mention for their role in it. The pleasing results would be something shareholders would keep in mind at the upcoming AGM on 17 October 2022. This would also be a chance for them to hear the board review the financial results, discuss future company strategy and vote on any resolutions such as executive remuneration. Here is our take on why we think CEO compensation is not extravagant.

Check out the opportunities and risks within the NZ Food industry.

Comparing PGG Wrightson Limited's CEO Compensation With The Industry

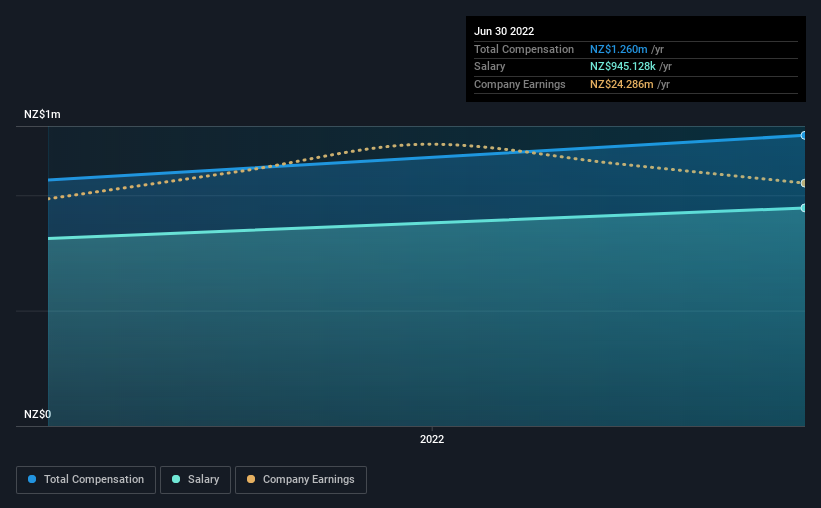

Our data indicates that PGG Wrightson Limited has a market capitalization of NZ$332m, and total annual CEO compensation was reported as NZ$1.3m for the year to June 2022. That's a notable increase of 18% on last year. In particular, the salary of NZ$945.1k, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the same industry with market capitalizations ranging between NZ$180m and NZ$720m had a median total CEO compensation of NZ$1.3m. From this we gather that Stephen Guerin is paid around the median for CEOs in the industry.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | NZ$945k | NZ$813k | 75% |

| Other | NZ$314k | NZ$253k | 25% |

| Total Compensation | NZ$1.3m | NZ$1.1m | 100% |

On an industry level, around 56% of total compensation represents salary and 44% is other remuneration. It's interesting to note that PGG Wrightson pays out a greater portion of remuneration through salary, compared to the industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

PGG Wrightson Limited's Growth

PGG Wrightson Limited's earnings per share (EPS) grew 85% per year over the last three years. In the last year, its revenue is up 12%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has PGG Wrightson Limited Been A Good Investment?

Boasting a total shareholder return of 124% over three years, PGG Wrightson Limited has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

The company's solid performance might have made most shareholders happy, possibly making CEO remuneration the least of the matters to be discussed in the AGM. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 1 warning sign for PGG Wrightson that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:PGW

PGG Wrightson

Provides goods and services for agricultural and horticultural sectors in New Zealand.

Proven track record with slight risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor