- New Zealand

- /

- Capital Markets

- /

- NZSE:NZX

Should Shareholders Reconsider NZX Limited's (NZSE:NZX) CEO Compensation Package?

Key Insights

- NZX will host its Annual General Meeting on 17th of April

- CEO Mark Peterson's total compensation includes salary of NZ$600.0k

- The total compensation is similar to the average for the industry

- Over the past three years, NZX's EPS fell by 13% and over the past three years, the total loss to shareholders 34%

NZX Limited (NZSE:NZX) has not performed well recently and CEO Mark Peterson will probably need to up their game. At the upcoming AGM on 17th of April, shareholders can hear from the board including their plans for turning around performance. They will also get a chance to influence managerial decision-making through voting on resolutions such as executive remuneration, which may impact firm value in the future. The data we present below explains why we think CEO compensation is not consistent with recent performance.

See our latest analysis for NZX

How Does Total Compensation For Mark Peterson Compare With Other Companies In The Industry?

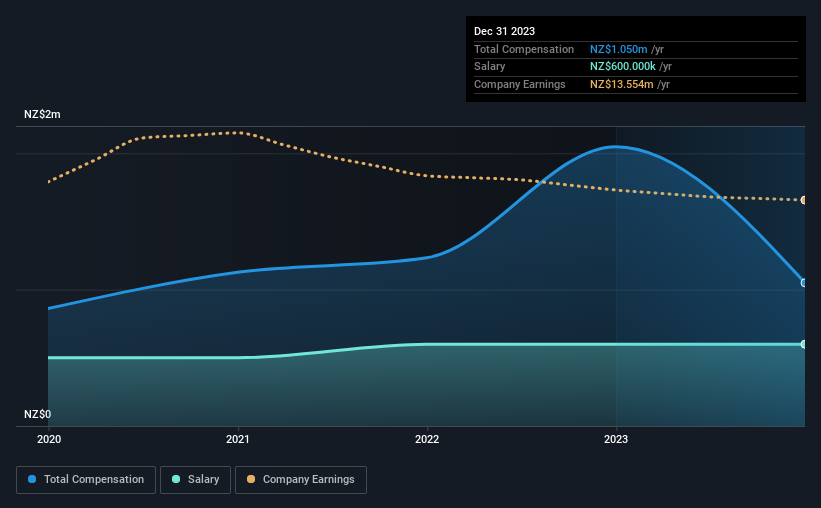

At the time of writing, our data shows that NZX Limited has a market capitalization of NZ$371m, and reported total annual CEO compensation of NZ$1.1m for the year to December 2023. We note that's a decrease of 49% compared to last year. Notably, the salary which is NZ$600.0k, represents a considerable chunk of the total compensation being paid.

On examining similar-sized companies in the New Zealand Capital Markets industry with market capitalizations between NZ$167m and NZ$668m, we discovered that the median CEO total compensation of that group was NZ$1.1m. So it looks like NZX compensates Mark Peterson in line with the median for the industry. Furthermore, Mark Peterson directly owns NZ$956k worth of shares in the company.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | NZ$600k | NZ$600k | 57% |

| Other | NZ$450k | NZ$1.4m | 43% |

| Total Compensation | NZ$1.1m | NZ$2.0m | 100% |

On an industry level, around 61% of total compensation represents salary and 39% is other remuneration. NZX is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at NZX Limited's Growth Numbers

Over the last three years, NZX Limited has shrunk its earnings per share by 13% per year. In the last year, its revenue is up 13%.

Overall this is not a very positive result for shareholders. While the revenue growth is good to see, it is outweighed by the fact that EPS are down, over three years. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has NZX Limited Been A Good Investment?

The return of -34% over three years would not have pleased NZX Limited shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Given that shareholders haven't seen any positive returns on their investment, not to mention the lack of earnings growth, this may suggest that few of them would be willing to award the CEO with a pay rise. At the upcoming AGM, they can question the management's plans and strategies to turn performance around and reassess their investment thesis in regards to the company.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 1 warning sign for NZX that investors should think about before committing capital to this stock.

Switching gears from NZX, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if NZX might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:NZX

Flawless balance sheet with proven track record.